Hello my dears,

Today we're going to show everyone who thinks of shoes when they think of Chucks what the precious Chucks are.

After the great success of our company presentation from France by Riber $ALRIB (+5,28 %) . we took another look around the semiconductor industry in France.

Just like Riber, we have found another niche champion.

Today we would like to introduce you to an indispensable blade supplier.

How much potential do you see here? And do you share Juan's opinion that we even have a long-term tenbagger candidate here?

With SEMCO we present you a newcomer to the stock market.

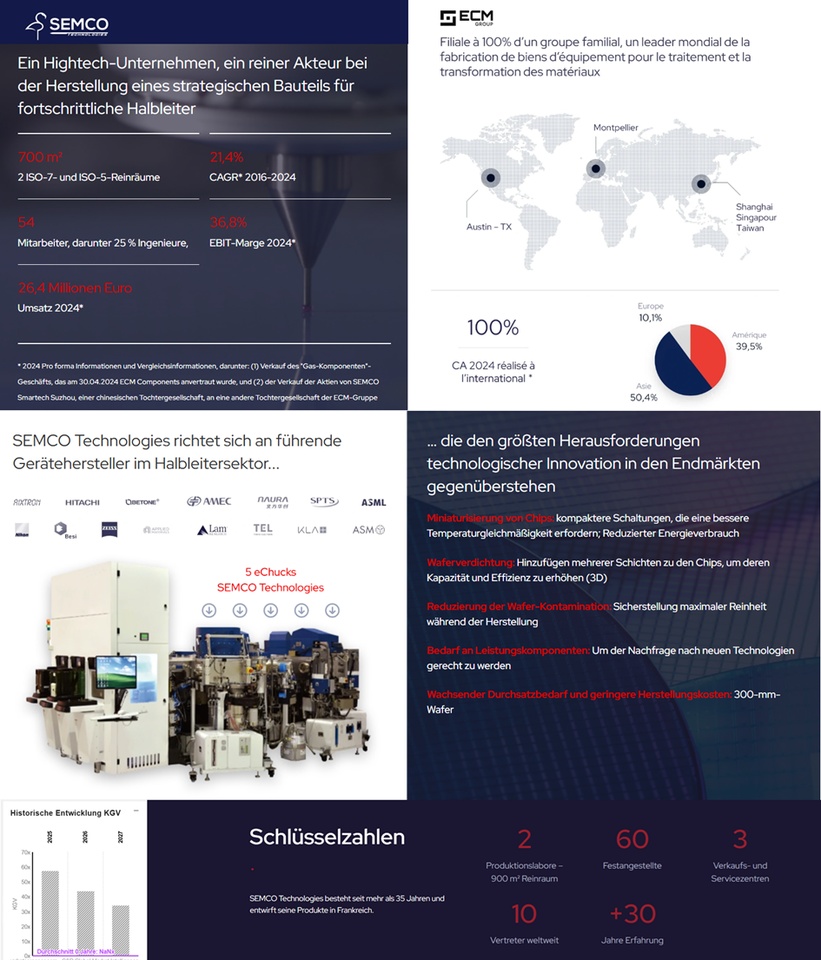

SEMCO Technologies specializes in the development and manufacture of electrostatic chucks for the production of semiconductor components.

Net sales are distributed geographically as follows: France (16.3 %), Europe (9.1 %), Asia (41.9 %) and America (32.7 %).

Number of employees: 54

Semco Technologies has announced that it has passed several important milestones in the implementation of its growth strategy. In particular, the specialist in the development and manufacture of strategic components for semiconductor production has announced the opening of a subsidiary in China to strengthen its commercial and industrial presence in one of its strategic markets.

In addition, the company has continued to automate its production site in Montpellier in order to increase its industrial capacity and meet the growing demand for semiconductors.

Finally, Semco Technologies has appointed Clément Dupuy as Technical Director to manage the innovation and co-development of eChucks with customers and prospects. An eChuck is an electrostatic chuck. It is a high-precision component used in factories for the production of electronic chips.

© MarketScreener.com - 2026

(14,01,2026)

01 - What is a chuck?

The chuck is the carrier on which the wafer (silicon wafer) is placed for processing

02 - What is its purpose?

The chuck is the only component in contact with the wafer to ensure stability, purity and thermal control during the semiconductor manufacturing process

03 - What is the added value of Semco's chucks?

SEMCO produces next generation eChucks or electrostatic chucks to improve the quality and yield of the final product

04 - Who do you produce eChucks for?

SEMCO markets its eChucks to the world's leading manufacturers of next-generation semiconductor production equipment

AIXTRON, HITACHI, BETONE, AMEC, NAURA, SPTS, ASML, NIKON, Besi, ZEISS, Applied Materials, Lam Resarch, Tokio Electron, KLA, ASM Intern.

SEMCO's moat is based on:

1) Specialization in "Next-Gen eChucks"

SEMCO focuses on new generations of ESCswhich:

- better temperature control

- higher purity

- less particle formation

- higher yield stability.

This is a real differentiating factor.

2) Very small but extremely demanding niche

The ESC market is tinybut technologically extremely demanding. Only a few companies can even produce it.

→ High barriers to entry.

📌 Conclusion for investors

Direct competitors: Kyocera, Technetics, Plansee.

Moat: Yes - SEMCO has a technological niche moatwhich is based on material know-how, OEM qualification, purity, temperature control and process integration. based.

Market structure: Oligopoly with extremely high barriers to entry → very attractive for small specialists like SEMCO.

Why SEMCO can outperform (tenbagger logic)

(1) Tiny market + high barriers to entry

→ Few competitors, hardly any new players.

(2) OEM lock-in

→ Once qualified = years of sales.

(3) Technological advantage

→ "Next-Gen eChucks" are a real differentiator.

(4) Structural growth in the semiconductor market

→ ESC demand is growing faster than the overall market.

(5) SEMCO is small - the big players are sluggish

→ Asymmetrical competitive situation.

(6) Margin potential extremely high

→ ESCs are high-value components.

(7) Net cash balance + scaling

→ Financial data shows: SEMCO is growing cleanly and becoming more profitable every year.

⭐ Juan's conclusion: Why SEMCO can outperform

SEMCO sits in a mini niche with mega barriersdelivers next-gen technology, is OEM qualified, is growing double-digit growth, has net cashand the competition is big, slow and not focused.

This is exactly the kind of asymmetric setupfrom which tenbaggers emerge.

SEMCO_HYR2025_25092025_FR_vf.pdf

Juan's conclusion (short & sweet):

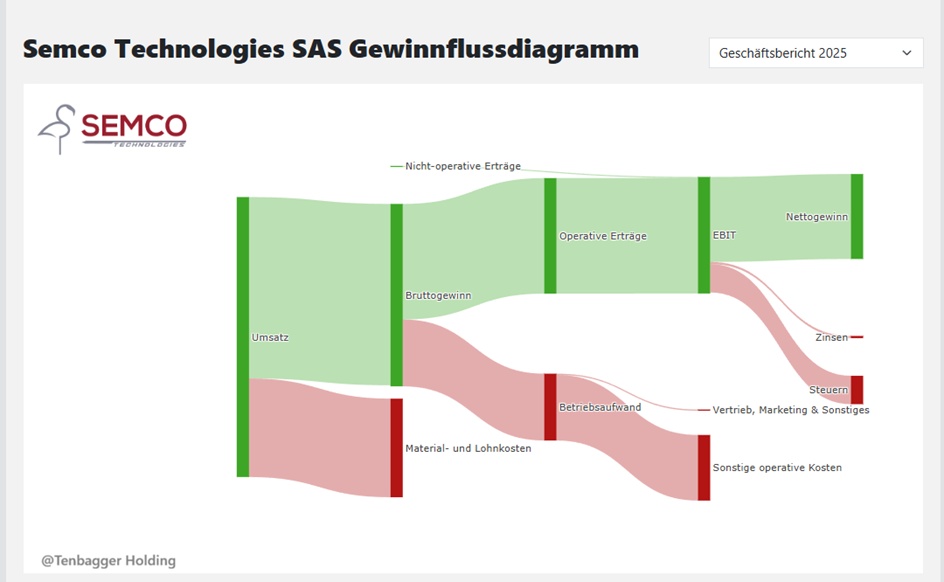

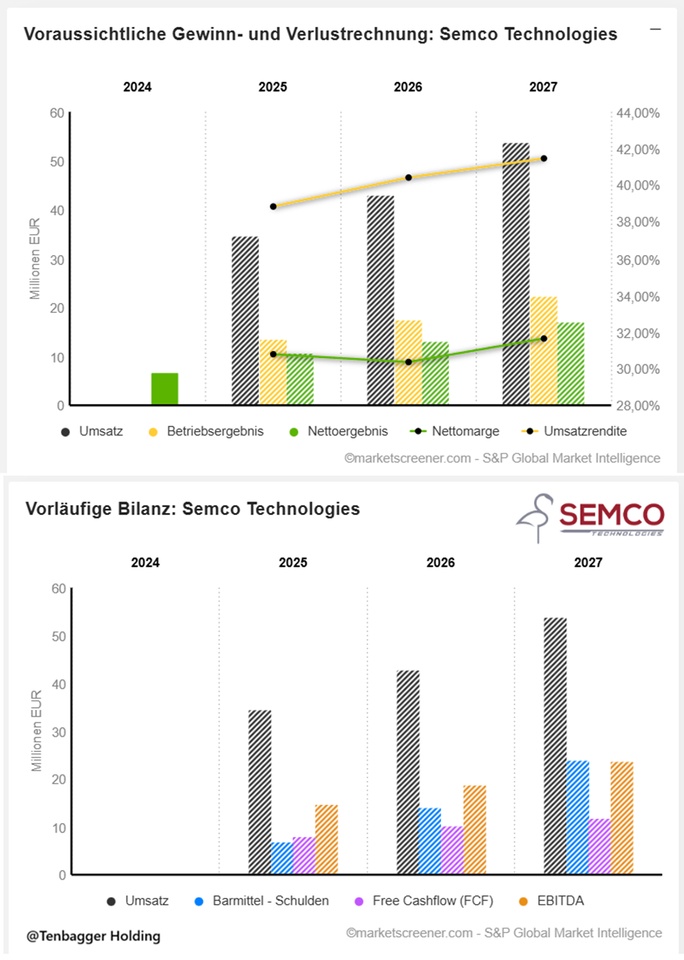

Semco delivers a strong growth triangle: sales are growing at double-digit rates every year, EBIT and FCF are growing cleanly and margins remain impressively stable at a high-tech level. Net debt has turned deeply negative - in other words, the company is really solid financially. EPS jumps dynamically upwards again after the split effect. Overall: small company, but the key figures look like something out of a textbook for scalable, profitable growth.

Market value 569.8

Number of shares (in thousands) 10,267

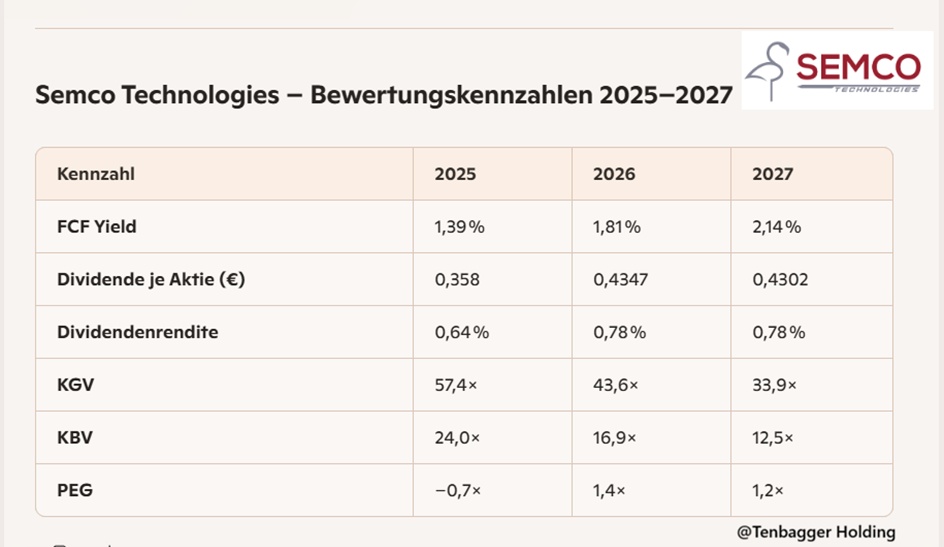

Juan analysis (key valuation figures 2025-2027)

Semco looks like a classic high-growth stock that is only just entering its valuation normalization phase. The FCF yield is rising cleanly every year - still low, but clearly heading in the right direction. The dividend is growing moderately, but remains rather symbolic.

The P/E ratio is falling from "sporty" to "healthy growth", while the P/B ratio and PEG show that the market is increasingly pricing in scaling, but is no longer exaggerating. PEG 2027 at 1.2 is almost a quality signal: growth and valuation are coming into balance.

In short: Semco is getting cheaper every year without growth slowing down. Exactly the kind of valuation trend that is really fun in the long term.

⭐ Juan's hoodie conclusion

"Semco is scaling like a high-tech mini-champion: growth strong, margins rising, cash flow getting stronger and valuation falling every year. Exactly the kind of structural setup that creates long-term tenbaggers."

Performance

1 week +13.38 %

1 month +18.21 %

6 month + 134.18 %

03,06,2026, 17:35:10 -

Euronext Growth Paris (EUR)

55.50 EUR

$FR0014010H01 (+4,25 %) (@Get_Rich_or_Die_Tryin ,great margins)