Hello my dears,

Over the Whitsun holidays, Juan has a visit from Avi from Israel.

And of course, how could it be otherwise, this visit was about companies with potential from Israel.

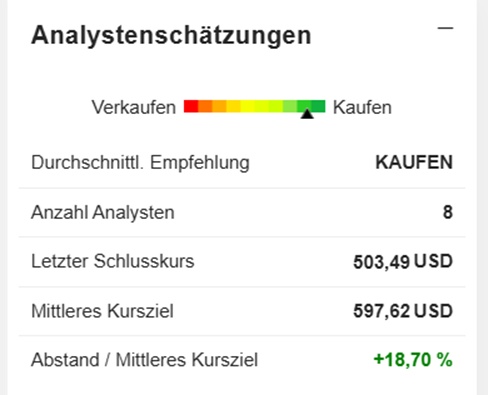

Even if the analysts still see room for improvement here. Based on the valuation, Juan would recommend the watch for now. But apart from that, there is a lot of enthusiasm about the company that Avi brought us from Israel.

Your many comments on $NVMI (-3.44%) would be much appreciated by Avi and Juan. After all, they spent their time working on this presentation for you in the beautiful weather.

22.05.2026, 22:00:00 -

Nasdaq (USD)

503.49 USD

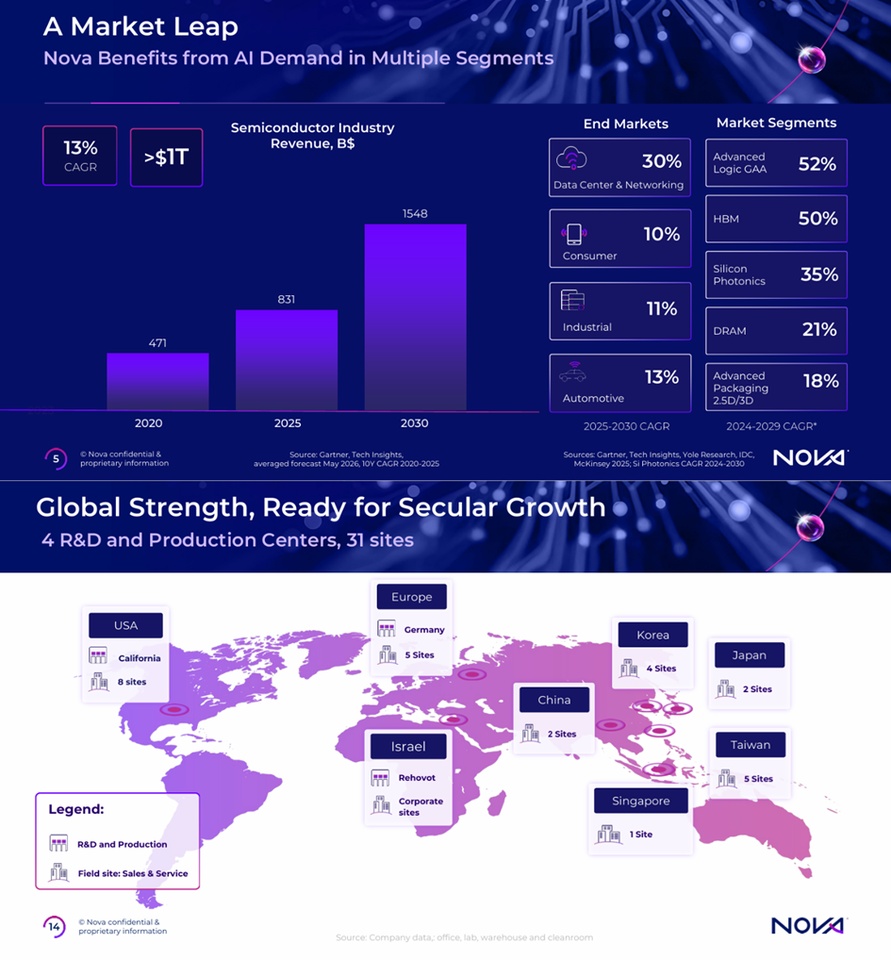

Nova Ltdformerly Nova Measuring Instruments Ltd, is an Israel-based company that provides metrology solutions for the semiconductor industry. The company offers in-line optical and X-ray stand-alone metrology systems as well as integrated optical metrology systems that are directly connected to wafer fabrication process equipment. The company's metrology systems measure various layer thickness and composition properties as well as critical dimension (CD) variables during various front-end and back-end-of-line steps in semiconductor wafer manufacturing. The product portfolio includes a range of in-situ, integrated and stand-alone measurement platforms suitable for dimensional, coating and material measurements for process control in various semiconductor manufacturing process steps. Products include NovaScan 2040, NovaScan 3090Next, Nova i500, Nova T500, Nova T600 and Nova V2600 TSV metrology system.

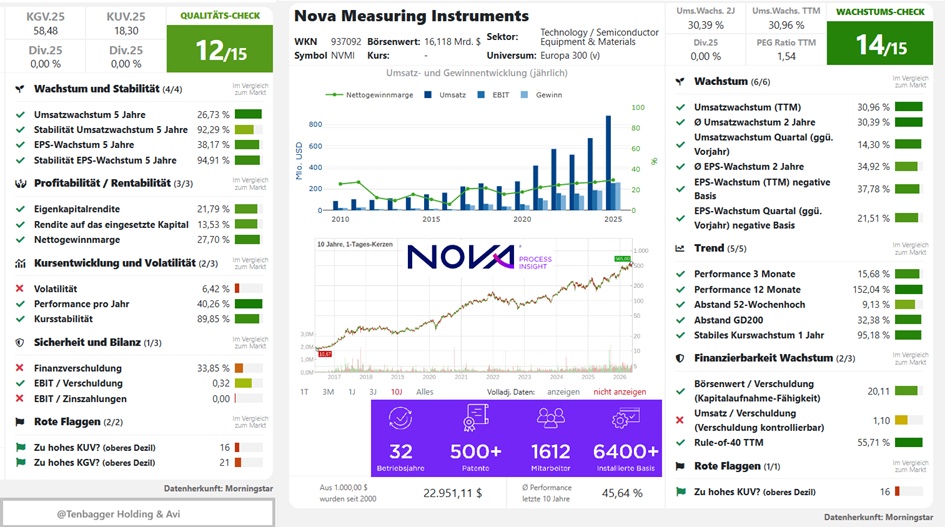

Number of employees: 1,612

nova-investor-presenation-q12026.pdf

Nova reports record financial results for the first quarter of 2026

May 14, 2026

|

Rehovot, Israel

Geographical distribution of sales

2025 (USD)

China 291 million

Taiwan, ROC 255 million

Korea 141 million

Other 114 million

U.S.A. 79.25 million

Short Juan summary

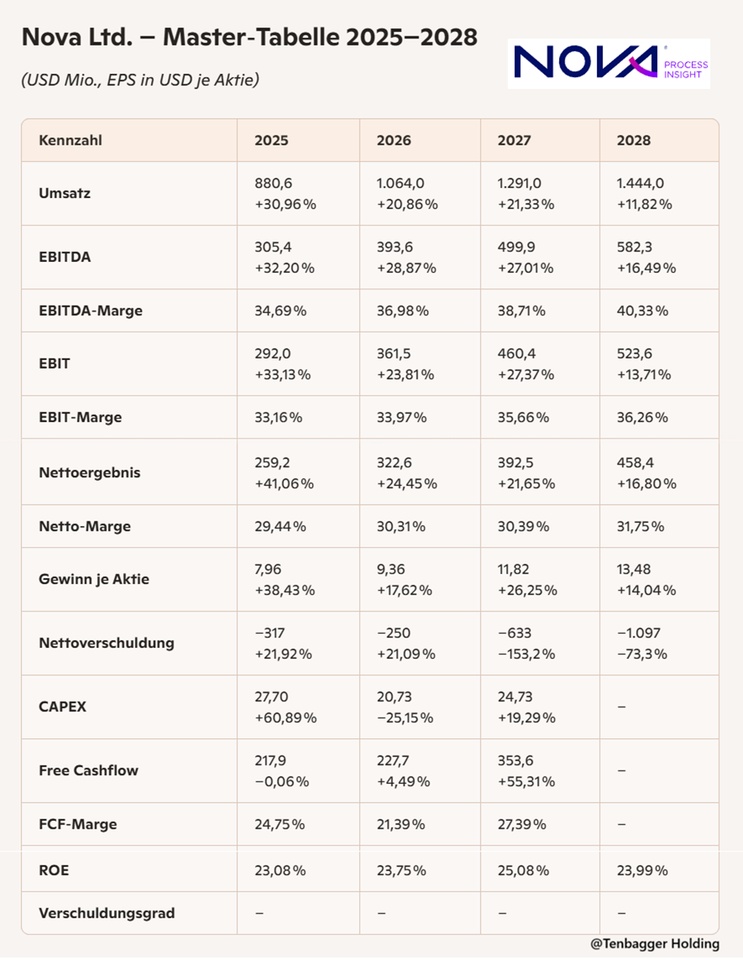

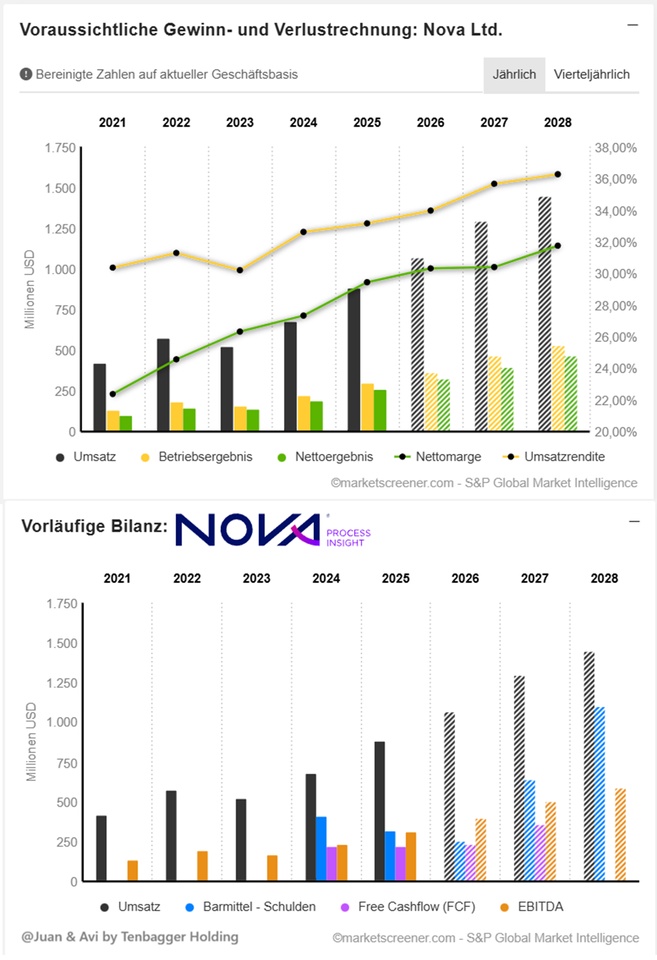

Nova is delivering a strong, clean growth profile: sales, EBITDA and EBIT are growing at double-digit rates every year, with margins climbing steadily towards 40%. Net profit and EPS are following suit, which clearly confirms profitability. Net debt turns deeply negative, FCF remains solid and gains significant momentum from 2027 onwards. For Juan, this is a classic quality compounder setup: high scalability, strong cash conversion, robust balance sheet - a structurally growing semiconductor enabler with clear visibility.

Market value 16,002

Number of shares (in thousands) 31,783

Date of publication 12.02.2026

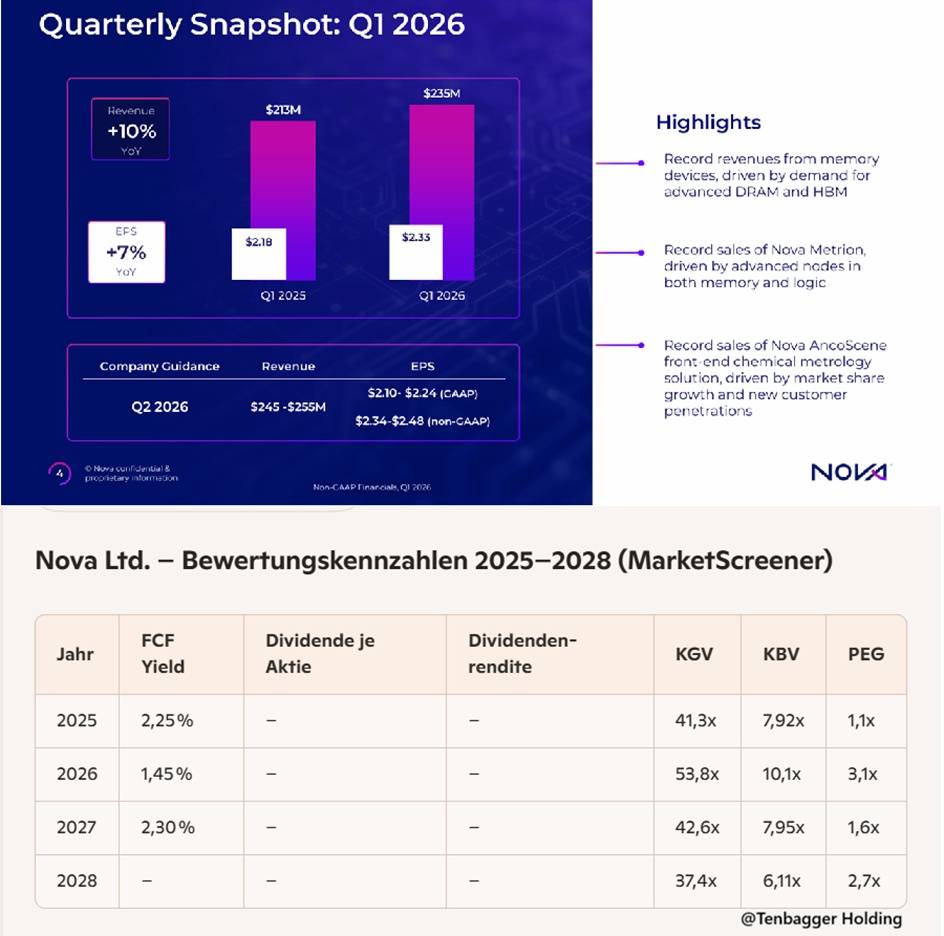

🔹 Juan conclusion on the valuation ratios (Nova Ltd.)

(Basis: MarketScreener data 2025-2028 )

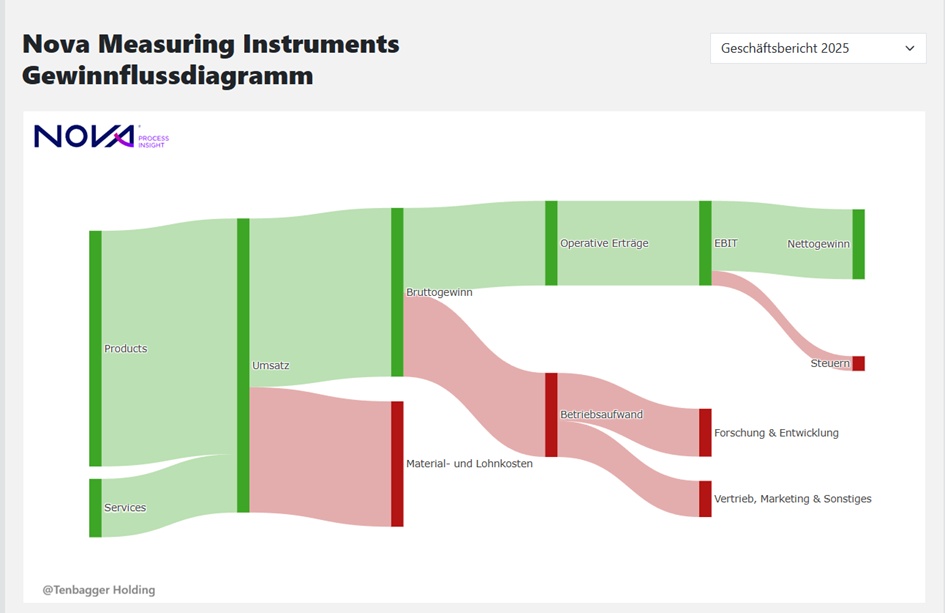

Nova delivers a clear high-growth profile - but at a price that now looks really ambitious. The P/E ratio rises to 41-54x in 2025-2026while the PEG 2026 at 3.1x clearly signals that earnings growth no longer fully justifies the valuation. At the same time, the FCF yield falls to just 1.45-2.3% in 2025-2027which is extremely low for a mature semiconductor supplier.

Positive: From 2027, the valuation eases slightly (P/E ratio 42.6x → 37.4x) and the PEG normalizes again. There are still no dividends - Nova remains a pure growth play.

In a nutshell: Strong structural growth, but the stock is currently "Quality at a High Price". Attractive for long-term investors, but rather "expensively priced in" in the short term.

Performance

1 week -1.00 %

1 month -2.30 %

6 months +78.21 %

1 year +167.93 %

3 years +363.43 %

5 years +459.47 %

7 years +1,761.73 %

25,05,2026

today, 14:37:50 -

Lang & Schwarz (EUR)

434.10 EUR