Hello my dears,

Today I would like to discuss one of the strongest Japanese stocks with you once again. That's why Juan has picked out the current financial and valuation ratios for you.

After good figures but a somewhat disappointing outlook, which in my opinion could also improve with peace in Iran.

And could therefore also provide a surprise. In the long term, we are in a growth segment in which Fujikura is continuing to expand.

I also see the current share price losses as being due to a weak Japanese market.

At a glance:

- Record profit of 157.2 billion yen

- Outlook for 2027 well below analysts' expectations

- Provision for US tariffs a burden

- Dividend raised to 40 percent

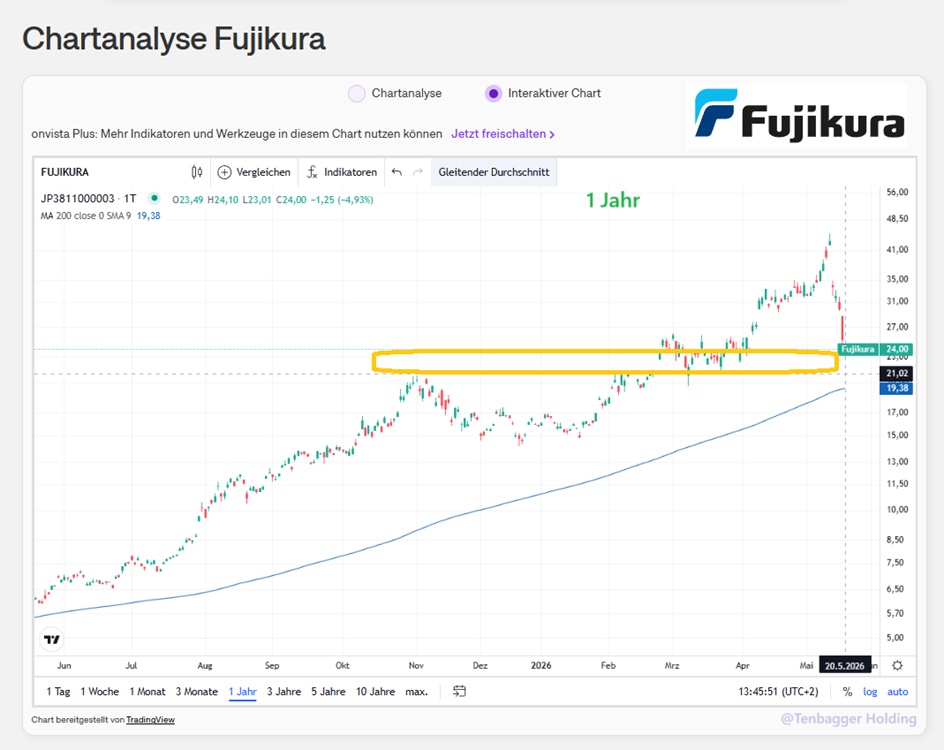

Record profits, and yet the share price plummets by 20 percent. What is currently happening at Fujikura illustrates a classic stock market phenomenon: it is not looking back that determines the share price, but looking forward.

Outlook falls well short of expectations

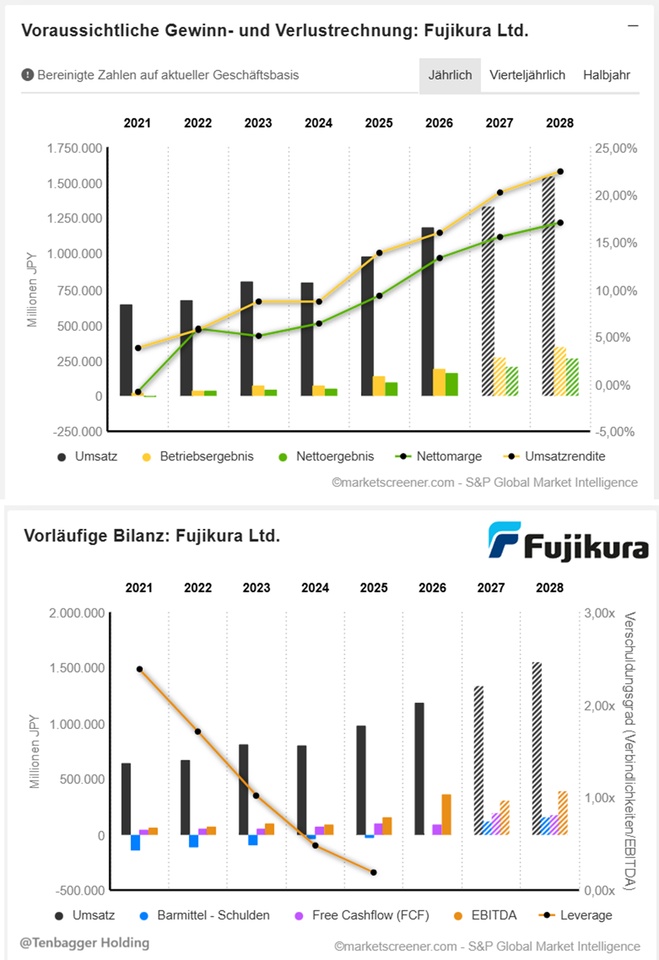

Fujikura reported a net profit of 157.2 billion yen for the financial year to March 2026 - an increase of 73% compared to the previous year. Sounds strong. The problem lies in the next step.

For the current financial year to March 2027, the company expects a net profit of 156 billion yen - a marginal drop compared to the record year. Analysts had around 207.7 billion yen on the cards. The gap is around 25 percent. No wonder investors are reacting nervously.

To make matters worse, Fujikura had to make a provision of 12.8 billion yen for US tariffs on fiber optic imports from a subsidiary in China. The company intends to contest the customs decision and the damage has been priced in for the time being.

Strong core business, but rising costs

The operating picture is actually robust. Last year, sales rose by around 21 percent to 1.182 trillion yen, while the operating result climbed 39 percent to 188.7 billion yen. Growth was driven by the telecommunications, automotive and energy systems segments.

For the new financial year, Fujikura is expecting sales of 1.243 trillion yen - i.e. further growth. However, rising raw material costs and geopolitical risks are putting pressure on the profit margin. The management explicitly mentioned a possible conflict in the Middle East and a potential blockade of the Strait of Hormuz as scenarios that have been factored in.

Dividend high, investments underway

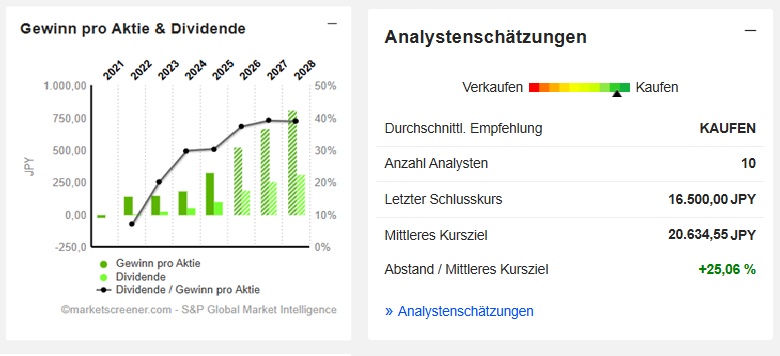

To bolster shareholder confidence, Fujikura is raising the payout ratio from 30% to 40%. A final dividend of 130 yen per share has been proposed for the past financial year - before the 1:6 stock split completed in the spring. For the new year, the company is planning 38 yen per share on an adjusted basis.

Strategic investments are running in parallel. The new US subsidiary Fujikura Cable Systems LLC is to be founded in Delaware in June 2026. The plant in Sakura will receive up to 40 billion yen to expand the production of fiber optic cables for AI data centers - commissioning is planned by the end of 2030. Fujikura has also developed a technology for precise three-dimensional nanostructuring together with MIT, which is intended for optical communication and AI applications.

Thursday's fall in the share price is less a reflection of the past than of uncertainty about the pace of recovery. Whether the conservative guidance contains buffers or reflects the actual expectations will become clearer with the half-year figures in the fall at the latest.

Fujikura Aktie: Guidance 25 Prozent unter Analystenschätzung - Finanztrends

Dear all, would you play the hero and get in now?

Or wait for a further correction to €21?

Or perhaps wait for an improvement in sentiment in the end?

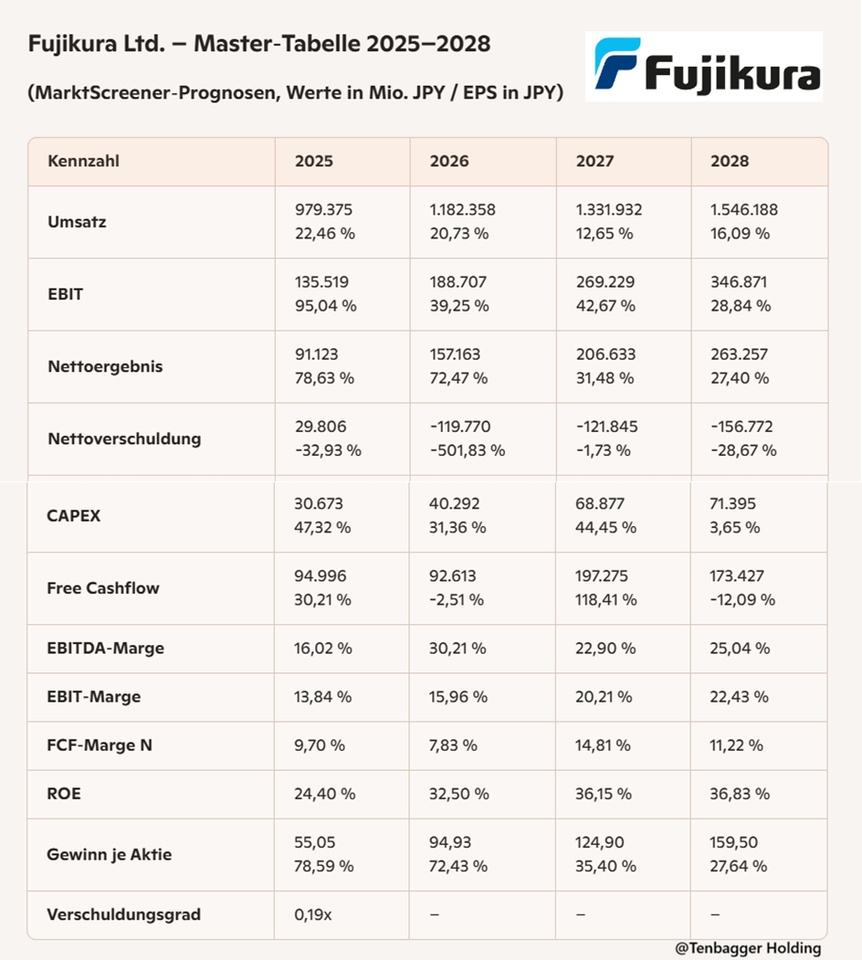

Juan-Investment-Summary - Fujikura (2025-2028)

(compact, investor-focused, without marketing bullshit)

1) Growth & scaling

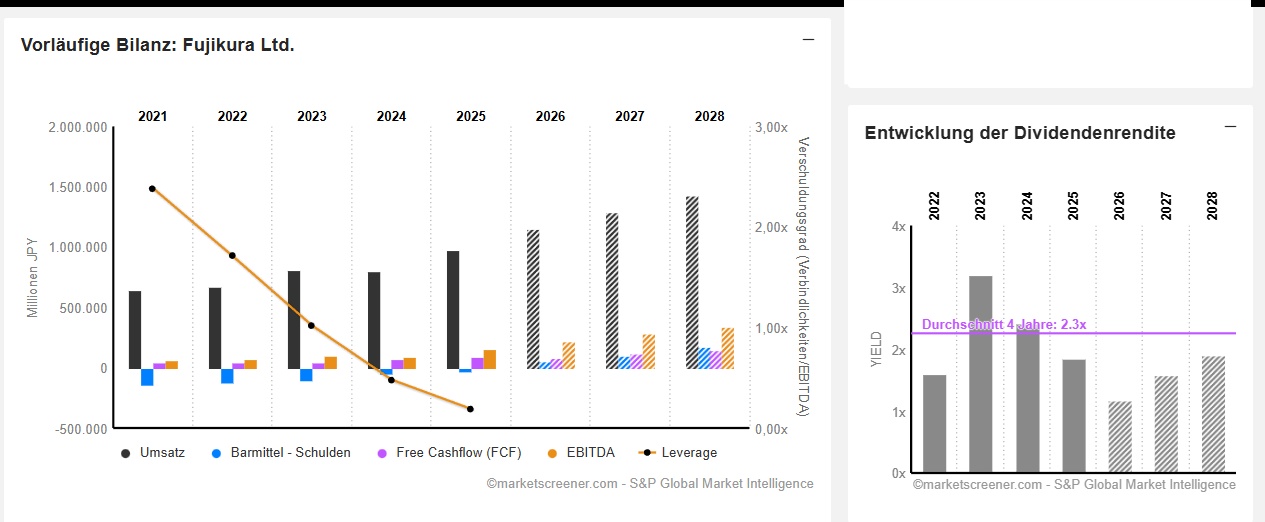

- Sales increase from JPY 979 bn → JPY 1,546 bn (2025-2028).

- Solid double-digit annual growth → Clear scaling path.

- EBIT grows disproportionately → Operating levers are working.

2) Profitability

- EBIT margin increases from 13,8 % → 22,4 %.

- EBITDA margin 2028 at 25 % → Top tier for Industrials.

- FCF margin volatile, but 2027 peak (14,8 %) shows cash power.

3) Balance sheet & capital structure

- Net debt turns deep into net cash in 2026 net cash.

- 2028: JPY -156 billion → Extremely solid balance sheet.

- Leverage ratio practically irrelevant → Financial risk minimal.

4) Yields & quality

- ROE increases to 36-37 % → High-quality compounder level.

- EPS grows from 55 → 160 JPY (2025-2028).

- Growth + margins + balance sheet = Quality profile clearly confirmed.

- 5) Juan conclusion

Fujikura is a structurally growing high quality industrial stock with massive margin expansion, net cash balance sheet and strong EPS compounding. The combination of scale, balance sheet strength and increasing profitability is rare and attractive.

Market value 7,773,320

Number of shares (in thousands) 1,655,659

Date of publication 14,05,2026

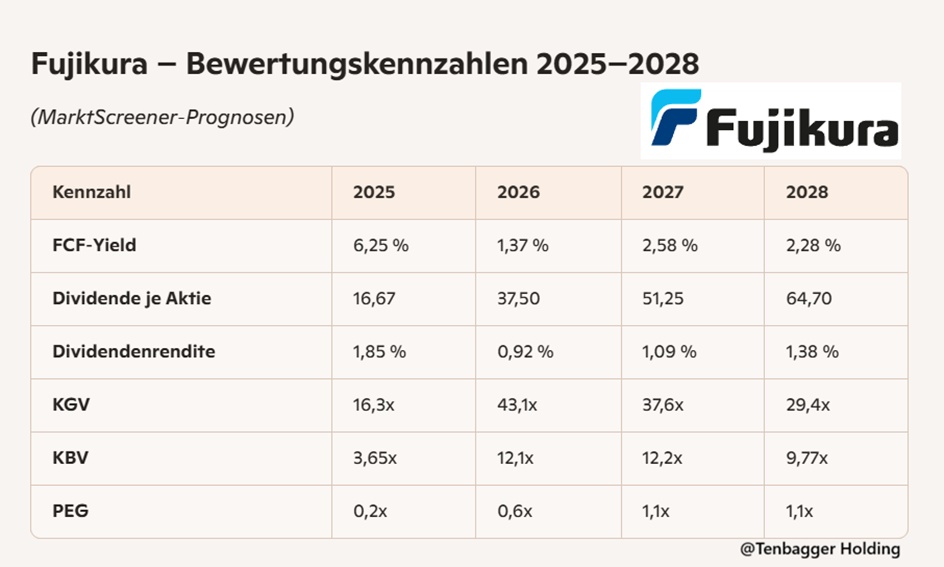

Juan conclusion (valuation)

Fujikura is traded as a high quality growth play: high multiples but supported by real EPS and margin compounding. The share is not cheapbut fundamentally well-founded expensive. For investors who are looking for quality + growth, this is a coherent valuation story.

20,05,2026

today, 13:52:01 -

Tradegate BSX (EUR)

24.10 EUR

-1.15 EUR-4.56 %

Ladies and gentlemen, would €21 be a good entry level for you?