Hello folks,

Today we're traveling to Scandinavia again. I'm surprised that we haven't already been introduced to today's company from Denmark by the Nordic Grand Master. (@Raketentoni )

That's why I'm all the more looking forward to our Mr. Prompt's assessment.

My dears, but of course I am also looking forward to many comments from you.

So let's start right away with the introduction of

$NETC (+1.76%)

Netcompany Group right away.

Netcompany Group A/S specializes in the provision of IT services in the field of electronic commerce. Net sales break down by activity as follows:

- Maintenance and technical support (51.9%);

- Development, implementation and management of IT solutions and services (47.6%);

- Sale of licenses (0.5%).

Net sales by market are split between the public sector (64.8%) and the private sector (35.2%).

The geographical breakdown of net sales is as follows: Denmark (52.6%), Belgium (12.1%), Greece (10.5%), United Kingdom (10%), Norway (5.3%), Luxembourg (2.8%), Netherlands (2%) and other (4.7%).

Number of employees: 7,942

Solution overview

1) Public sector & administration

- Business environment (self-service, case management, portals)

- EU institutions

- Enabling Europe to move faster | Netcompany

- Financial authorities / public financial affairs

- Social & Interior (social services)

- Taxation (Tax)

- Netcompany chosen to overhaul Danish tax administration | Netcompany

- Immigration

- Justice (Justice)

- Labor Market (Inspection & Supervision)

- Housing & Development

- Healthcare

- Education

- Legacy transformation (modernization of old IT systems)

- Netcompany to digitalise the city of Oslo | Netcompany

2) Security, defense & resilience

- Defense & Resilience (Multi-Domain Awareness, Response)

- Making defence ready for the cloud: a pathway to digital transformation for NATO | Netcompany

3) Infrastructure & mobility

- Airports

- Public Transportation (Ticketing, Road Pricing, Signaling)

- Go-Ahead and Netcompany join forces for more predictable train operations in Norway | Netcompany

- Logistics (real-time data platforms)

4) Energy, climate & sustainability

- Energy & utilities

- Climate & sustainability (data- & AI-based solutions)

5) Economy & private sector

- Banking (core banking, AI-supported)

- Manufacturing

- Retail & wholesale

- Property Management

- Service companies (cloud-based platforms)

- Telecommunications & Media

- Life & Pension

- Unions & Unemployment Insurance Funds

6) Cross-cutting technologies

- Data & integration portals

- Real-time data platforms

- AI-supported modernization

- Cloud-based utility platforms

- Self-service systems

- Case management solutions

🎯 Brief summary for you as an investor

Netcompany covers almost all critical digitization areas in Europe with a focus on:

- Government digitization (very stable, long-term contracts)

- Regulated industries (banking, energy, healthcare)

- Infrastructure & mobility (high barriers to entry)

- AI and data platforms (future growth drivers)

The portfolio is extremely broadbut at the same time highly specialized in digital platforms with reusability - a clear advantage for margins and scalability.

Netcompany - Product overview

1) ERMIS

Europe's leading customs solution. A modern, fully digital platform for customs clearance, transit processes and legally compliant customs processes. → Focus: public authorities, customs administrations, international logistics.

2) SOLONSTEUER (SOLON TAX)

Digital revenue and tax management for the public sector. An end-to-end solution for tax collection, payment management, compliance and modernization of government revenue systems. → Focus: tax authorities, ministries, national tax administrations.

3) PERSEUS

Future-oriented platform for pension and security administration. Digitizes pension processes, benefit allocation, case management and governance workflows. → Focus: pension funds, social security funds, state pension authorities.

4) LUMENUS

Next-gen risk analytics for the modern public sector. A data-driven platform for risk detection, analysis, prevention and decision support. → Focus: public authorities, security organizations, regulators.

5) DX4B

Modern banking platform for dynamic requirements. Supports digital banking processes, customer interactions, compliance, product management and modern financial architectures. → Focus: banks, financial service providers, fintech modernization.

🎯 Brief summary for you as an investor

Netcompany offers no generic IT productsbut highly focused, modular platform products for regulated, government and security-critical areas:

- extremely high barriers to entry

- Long-term contracts

- high reusability → increasing margins

- clear specialization in public sector & regulated industries

The product portfolio is strategically strong, scalable and resilient to economic cycles.

Netcompany - Future platforms

1) PULS

A real-time data enginethat connects all the moving parts of a company. It collects, links and orchestrates data across systems, enabling faster decisions, automation and growth. → Future relevance: real-time data, interoperability, AI readiness.

2) AMPLIO

A platform for orchestration of process automation and case management. It digitizes complex procedures, workflows and authority processes - scalable, modular, highly reusable. → Relevance to the future: Automation, efficiency, public sector digitalization.

3) AMI

A platform that companies, governments and citizens via intelligent, dynamic services. It enables secure interactions, self-service, identity management and seamless digital journeys. → Future relevance: Citizen services, digital ecosystems, secure interactions.

4) EASLEY

An AI platformthat increases productivity and empowers organizations, independent and resilient in the age of AI. It integrates AI models, automates knowledge work and supports data-driven decisions. → Future relevance: AI enablement, automation, knowledge work 2.0.

🎯 Brief summary for you as an investor

These four platforms are Netcompany's future stack - they address exactly the areas that are growing structurally in Europe:

- Real-time data & interoperability (PULS)

- Automation & process digitization (AMPLIO)

- Digital citizen and business services (AMI)

- AI productivity & modernization (EASLEY)

They are modular, scalable, reusable and have extremely high barriers to entry - a clear strategic advantage.

New contracts:

HM Revenue & Customs

- Netcompany has been selected by HMRC to implement and operate the next phase of its Trader Support Service (TSS). With a strong track record in digital trade and customs systems, the new digital TSS solution will be built on Netcompany's market-proven ERMIS customs product, which powers the Trader Support Service portal used by traders. In addition, Netcompany's AMPLIO platform will be integrated with ERMIS to provide case handling capabilities that will enable customer support staff to handle more complex trader queries.

COSMOTE

- Netcompany was awarded a project to implement Omilia OCP, a unified conversational AI platform that provides natural, human-like interactions, voice and chat automation across IVR, phone, messaging, web and mobile devices, and improved customer engagement for COSMOTE's contact center.

OBOS Bank

- OBOS Bank has selected Netcompany Banking Services to supply and maintain its new core banking system. The agreement highlights Netcompany Banking Services' approach based on open architecture, flexible integrations and a high degree of automation, and includes the development of a new, modern credit solution for the Norwegian market to strengthen the bank's competitiveness.

Danmarks Domstole

- Netcompany has been selected by the Danish jurisdiction to lead the comprehensive modernization of the core components and administration portal of the national digital land registry system (Tinglysningssystem). This important project will eliminate dependencies on outdated technology, ensure compliance with national security standards and create a more robust, secure and easier to maintain platform for future development.#

Forca

- Netcompany, Festina Finance and Forca have agreed to build the pensions solution of the future with OpenAdvisor, which will enable pensions advisers to provide better and more comprehensive advice to all members. The implementation of OpenAdvisor is part of the complete pension solution that will be provided to Forca and Forca's clients.

Piraeus

- Netcompany was selected for the further development of the Profits Core Banking System to support Piraeus Bank's branch activities, including upgrade to the latest Profits version, additional core banking modules, new payment services (SWIFT), regulatory reporting enhancements.

New contracts continue

STRYRELSON FOR IT OG LEARNING

- Netcompany has been selected as a provider under STIL's TUK framework agreement, which covers the development and maintenance of a portfolio of critical education and grants management systems. The contract includes responsibility for systems that support institutional grant payments, as well as the development of Denmark's new national examination platform, and many other solutions that support the public education sector in Denmark.

HEDNO

- Netcompany was selected to develop a fully modern, digital, secure consumer portal to transform citizen engagement with HEDNO. It covers 14 customer service use cases and over 150 variations, MyAccount status and notifications, chatbot and assistance support, appointment booking and video calls with agents, and integrations with over 15 external systems (government APIs, LLMs and more).

COSMOTE

- Netcompany secured a 3-year extension covering further development, maintenance and operational support across the Cosmote Payments ecosystem. This includes the core banking system, Payzy Wallet backend, customer onboarding, AML & fraud systems, card issuing and acquiring services, data analytics services, hosting and infrastructure support.

NATIONAL BANK OF GREECE

- NBG has engaged Netcompany in several strategic areas, including the creation and support of NBG's AI framework, the further development of small business loans and card issuance, the creation of Customer 360° within MyNBG, the implementation of new digital banking functionalities and SAP development services.

IKOMM

- Netcompany has signed a contract with Ikomm and the municipality of Nesodden to deliver a next generation of AI-powered case management. The system, based on our Easley AI platform, will be integrated into existing municipal systems to automate processes and improve decision-making. This strategic win paves the way for a scalable model for the future of digital public services and positions our platform for wider application in the public sector.

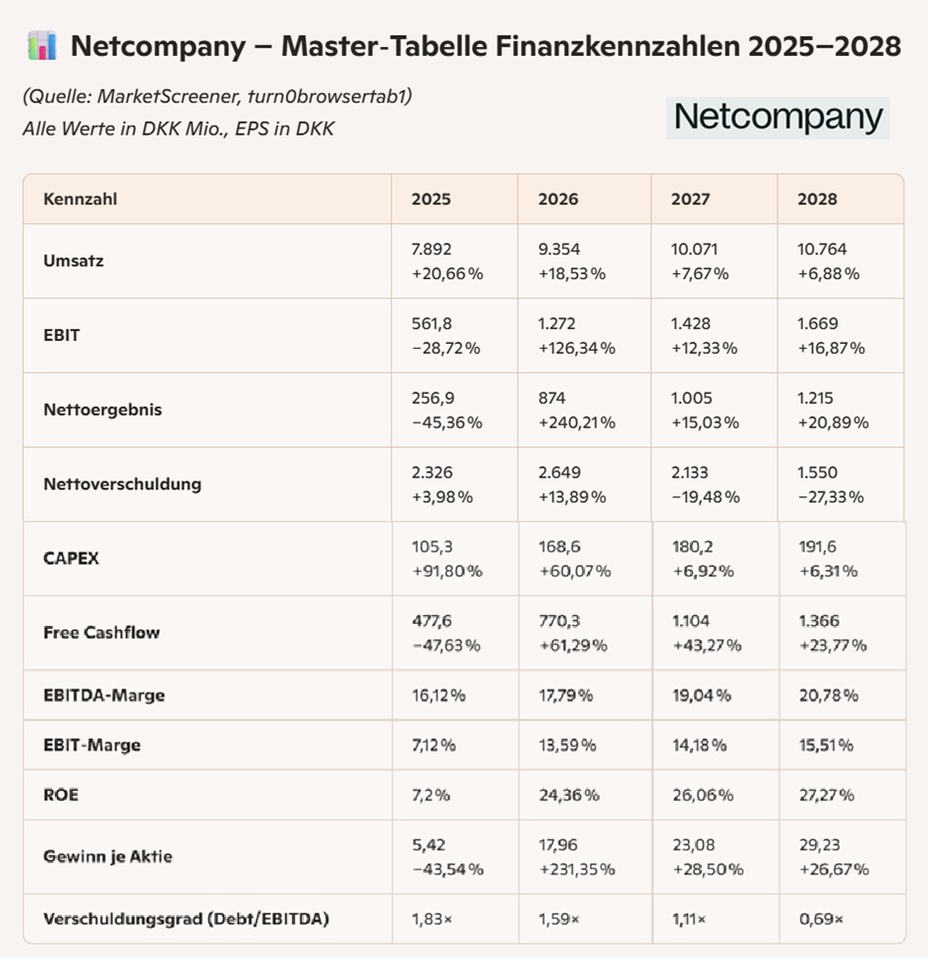

📌 Investment summary on Netcompany (2025-2028)

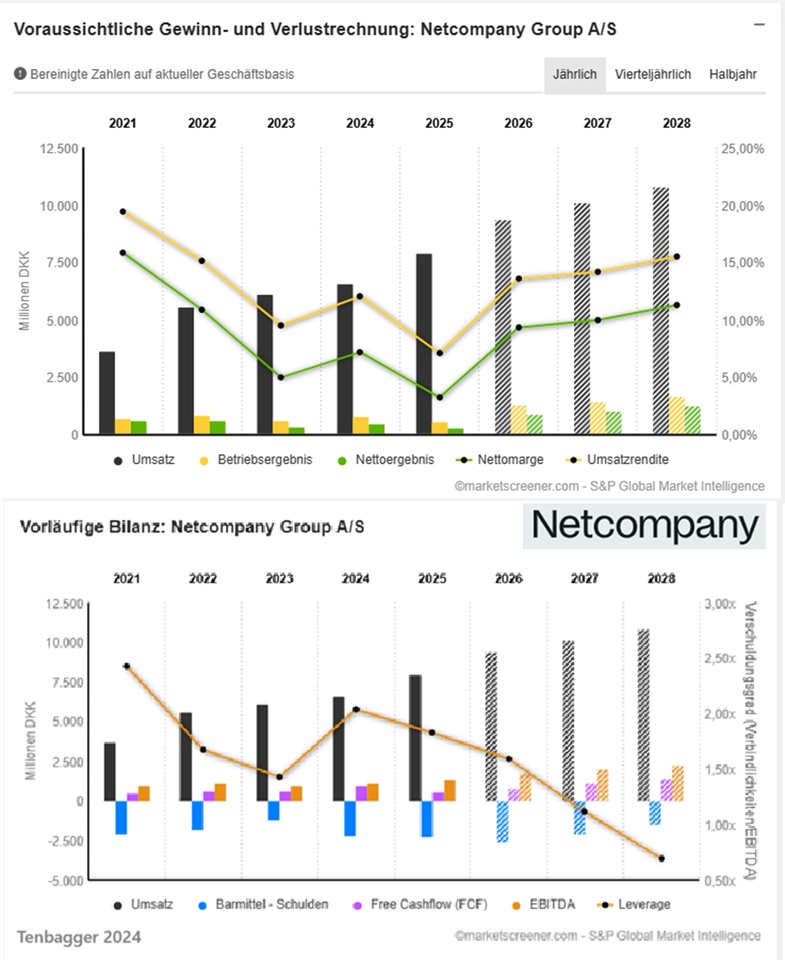

1) Growth - strong but not overheated

- Revenue growth 7.9 billion → DKK 10.8 billion until 2028.

- Growth remains double-digit growth 2025-2026, thereafter robust single-digit rates thereafter.

- That is healthy, predictable growthtypical of a public sector digitizer.

Valuation:

Solid structural growth, no high growth, but very stable.

2) Profitability - clear upward trend reversal

- EBIT margin increases 7,1 % → 15,5 %.

- EBITDA margin increases 16,1 % → 20,8 %.

- This is a massive margin expansionthat shows: → Scaling is working → Projects are becoming more profitable → Platform business is taking hold

Evaluation:

Quality feature - Netcompany becomes more efficient and has higher margins.

3) Free cash flow - growing strongly

- FCF increases 477 million → DKK 1,366 million.

- FCF growth > +180 % over the period.

- This is crucial because FCF = → Debt reduction → Dividend potential → M&A capability → Resilience

Valuation:

FCF machine - very positive for shareholders.

4) Balance sheet - greatly improved stability

- Net debt falls 2,649 million → DKK 1,550 million.

- Leverage ratio (debt/EBITDA) falls 1,83× → 0,69×.

Valuation:

Financially extremely solid - risk decreases, flexibility increases.

5) Return on capital employed - ROE increases significantly

- ROE increases 7,2 % → 27,3 %.

- This is a quality signalthat shows: → Capital is used efficiently → Scaling works → Profitability increases sustainably

Assessment:

High quality profile.

6) EPS - strong value creation for shareholders

- EPS increases 5.42 → 29.23 DKK.

- That is a fivefold increase in four years.

- Drivers: Margins, scaling, FCF, lower interest rates.

Valuation:

Very shareholder friendly - real value appreciation.

🎯 Overall conclusion for you as an investor

Netcompany is a structurally growing, highly profitable digitalization champion with clear margin expansion, strong FCF growth and falling debt.

The share offers you:

- Stable growth through public sector digitization

- Significant margin improvement

- Strong increase in free cash flow

- Rapidly decreasing debt

- High return on equity (ROE)

- EPS explosion → Genuine value creation

In short: 👉 Netcompany is a high-quality compounder in the European IT sector. 👉 Very attractive for long-term investors. 👉 Risks are manageable, high upside due to scaling.

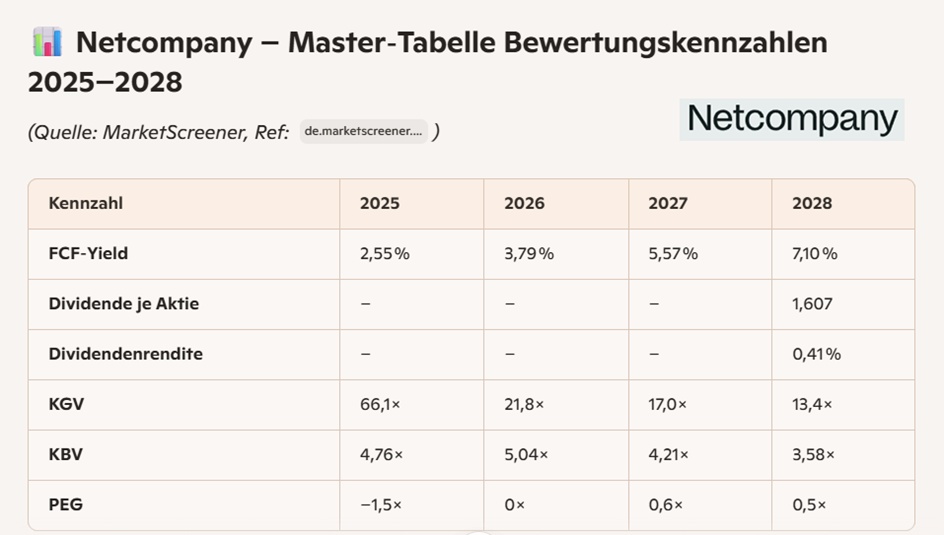

🔹 Value (valuation)

The valuation shows a clear easing over the coming years.

- P/E ratio falls massively: 66× → 13×

- FCF yield rises sharply: 2,55 % → 7,10 %

- P/B ratio falls: 4,76× → 3,58×

- PEG 2027-2028 attractive: 0,6× / 0,5×

Value conclusion: Netcompany is transforming from an expensive quality share to a fairly valued, FCF-strong compounder story. In 2028, the share looks clearly undervalued relative to growth.

🔹 Growth (growth)

The valuation ratios reflect healthy, structural growth growth.

- Stable sales growth (public sector + platform business)

- EPS rises sharply → Valuation multiples fall

- PEG in the "sweet spot" from 2027 (<1)

Growth conclusion: Netcompany is not a high-growth techbut a solid mid-growth digitizer with scalable platforms. The growth is predictable, resilient and high-margin.

🔹 Quality (quality)

The rating shows a company with high operational quality:

- increasing margins → higher return on capital

- FCF yield increases → cash flow quality improves

- P/B ratio remains moderate → no overheating

- PEG low → Growth at reasonable prices

Quality conclusion: Netcompany is a high-quality digital infrastructure player with strong margins, high customer loyalty and clear scalability.

🎯 Overall valuation (short & honest)

Netcompany is expensive in 2025 - but clearly attractively valued in 2027/2028. The share is developing into a quality compounder with falling multiples and rising cash flow power.

👉 Value improves significantly 👉 Growth remains stable 👉 Quality is high and continues to rise

For long-term investors this is a very good profile.

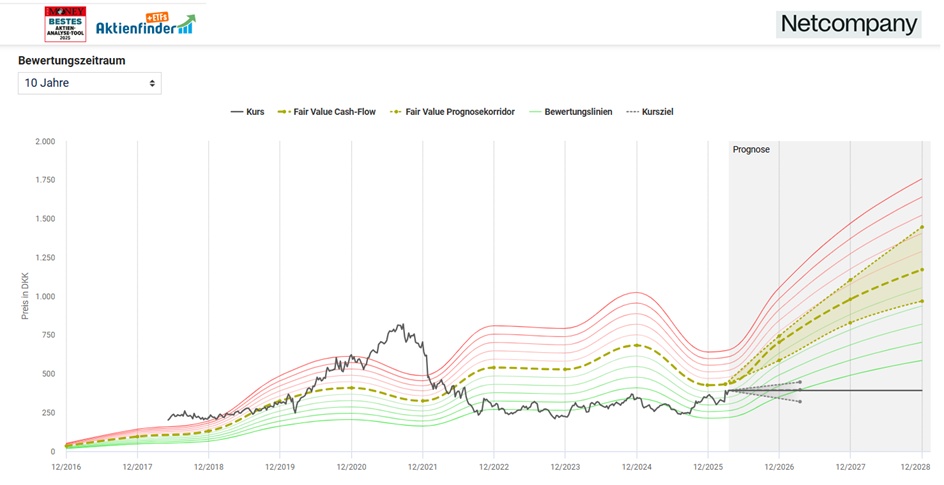

The key figure with the highest stability for the Netcompany Group share is the operating cash flowwhich is used below for the valuation. The KCV calculated from this key figure KCV (price/cash flow ratio) calculated from this ratio is 30.44 which is 4.23 points below the historical average of 34.67 for the last 10 years. From this perspective, the Netcompany Group share appears to be favorably valued to be favorably valued.

The fair value of the Netcompany Group share is calculated over the 10-year valuation period selected above. The average KCV in this case is 34.67.

Multiplied by the operating cash flow per share of DKK 12.48 over the last 4 quarters, the fair value of the Netcompany Group share is fair value of DKK 432.74. The current share price of DKK 391.81 is 9.5% below this fair value, which means that the share is slightly undervalued appears to be slightly undervalued.

Share price 53.60€ (17.04.2023 11.43 a.m.)