Hello,

Today I want to show you an alternative to shares, especially for younger savers, namely real estate investments, because this alternative will come in the next few years with the interest rate cuts.

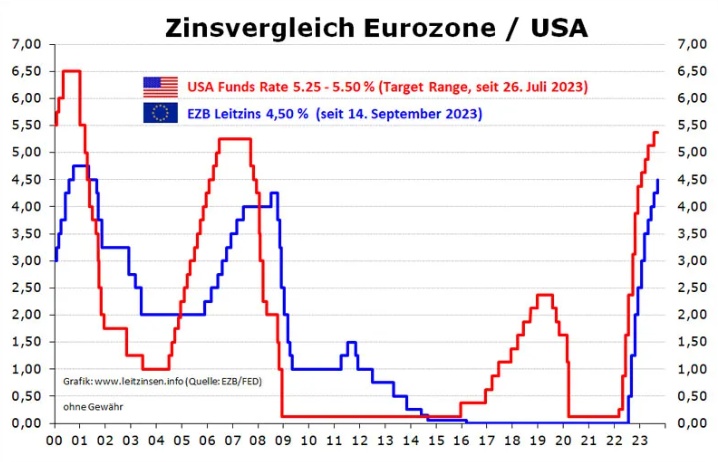

This is because it is important to find a good time to buy. In my opinion, this is the phase where the first interest rate cuts start to peak until the time when every layman has realized that interest rates are low. At the low point of interest rates, you won't be able to buy cheap apartments because the owners know this and demand high prices.

An example from me.

Apartment 73m2

Year of construction 1963

Purchase price 80k with additional costs 84k

ECB interest rate cuts started in 2009 and reached their lowest point in 2015.

I started looking for an apartment in 2010 and of course bought without an estate agent.

Borrowing 84k

Interest rate 2.8% approximately

Installment 672 euros with special repayment option

I paid it off in full within 5 years and then bought my next property in 2015.

Assuming I had repaid it over 10 years without unscheduled repayments:

Then I would have about 13,800 euros in interest expenses

Gross rental income for 10 years amounted to 93k

Service charges 37.5k

Renovations 4k

Net rental income 51k

minus interest 37k

In the case of this property, this means that a tenant helped me build up assets from zero to 100 with an average monthly installment of 37k / 120 = 308 euros.

If I had saved it with "MSCI World" as an alternative, for example, I would have had to save 700 euros from my monthly income for a savings rate of 700 euros.

But with this property, I only saved 700 - 300 = 400 euros.

Now let's simulate this further for 2015.

If I had saved it with MSCI World, I would have to liquidate this position when I buy a property later, as the bank won't accept it as collateral.

But if you already own an apartment, the bank will accept it as collateral. Professionals even negotiate with the bank to such an extent that the bank should take the market value into account so that better interest conditions are possible.

A second point:

The bank does not accept shares and their dividends as income.

Half of the rental income from the first apartment is included as income in the household calculation.

Many people will now come along and say that real estate is overvalued. I counter this with these arguments and additionally with the argument that "shares are even more overvalued".

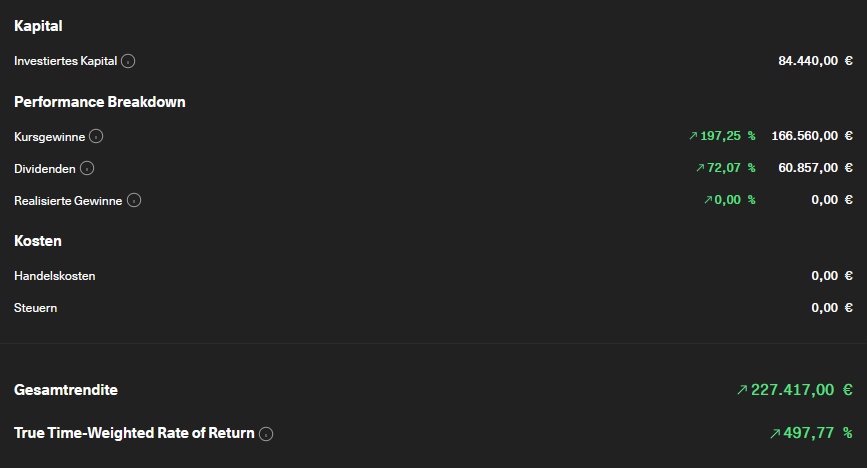

Third point: the performance of real estate is much better in the long term than that of shares, as you can gradually build up your assets. (see performance comparison of the apartment above vs. MSCI World vs. Allianz).

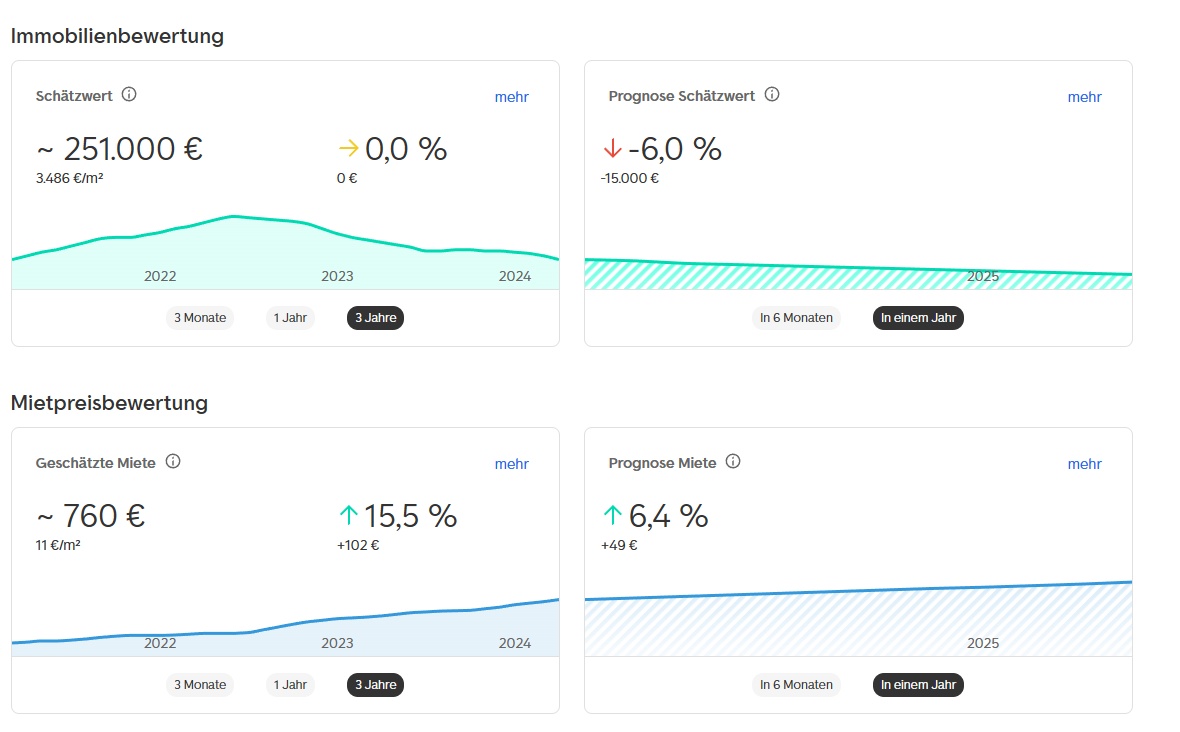

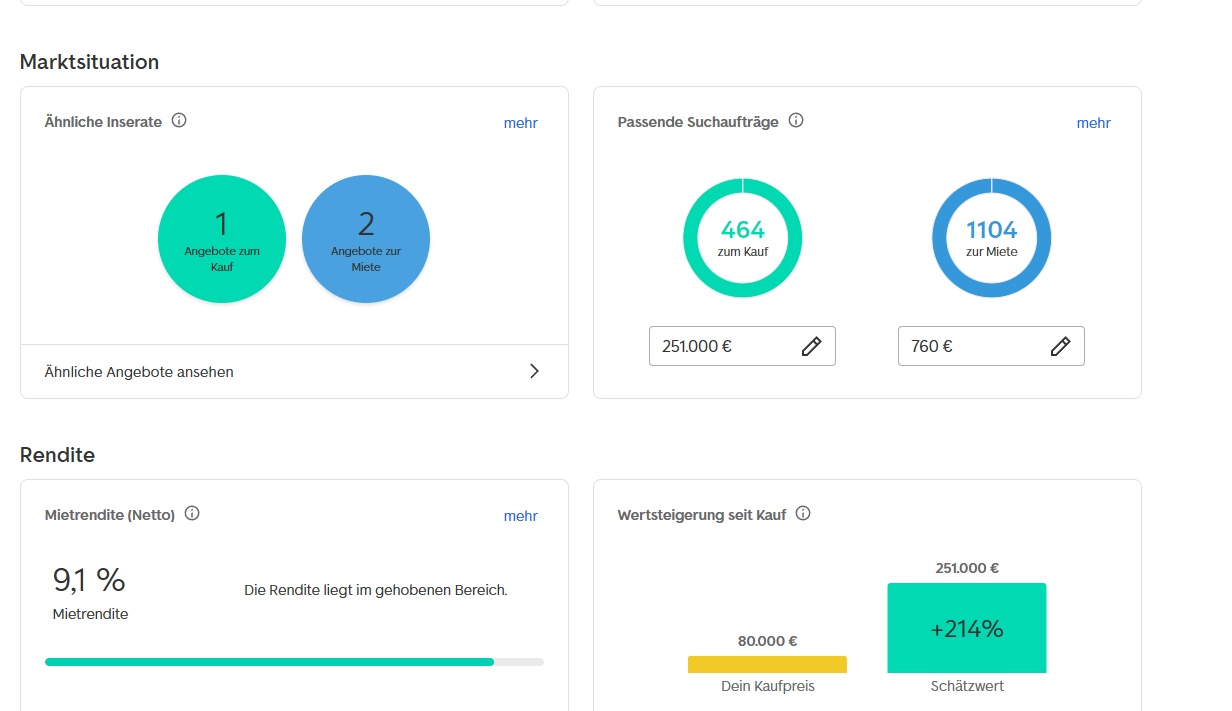

According to Immoscout, the current market price is 250k.

The important thing is to build up strategies.

Of course, you then have to deal with the matter (purchase agreement, rental agreement, tenant, property management, etc.).

Change of tenant:

I had a total of 4x tenant changes from 2012 to 2024.

This is the point where you have to take care of the apartment the most. But you can manage that without any problems. This is also the time when you have the highest rent increases.

The current demand is so high that I pick the best tenants to the best of my knowledge and belief.

But the HUGE ADVANTAGE here is not only the arguments from above but also the PLANNING SECURITY. You can't say that about shares.

Furthermore, you definitely don't invest as much time as with shares, which are always volatile.

I hope this helps some of you to look at alternative investments.

If I ever have time, I will post a similar post on "fixed-interest bonds" and then on "emerging market bonds".