Hello everyone,

In yesterday's vote, the majority decided in favor of a company presentation of AIXTRON $AIXA (+1.33%) was chosen.

AIXTRON was one of my first stocks many years ago. At a time when the Internet had just been invented. When lighting was still provided by light bulbs.

At that time, AIXTRON was a pioneer in LEDs, which were available as small red diodes. And there was still no thought of using them for lighting. And I was laughed at by some people for investing in a company that produced small red light-emitting diodes. Or builds the machines for production.

The fact that this technology had a future became apparent when Mercedes used these diodes as brake lights in a new S-Class.

A report in the Financial Times spoke of enormous energy savings if these new semiconductor diodes were used in traffic lights.

All these positive reports gave the AIXTRON share an enormous performance boost.

There was a further boost when it became possible to illuminate entire rooms with LEDs and the EU Commission no longer permitted the use of light bulbs.

In the end, I had enough equity from my share price gains to finance a property. But I never completely parted company with AIXTRON. And now the story can continue.

Ladies and gentlemen, I hope I haven't bored you with this little blast from the past.

So let's move on to the present and the future of AIXTRON.

AIXTRON SE is a company based in Germany. The company is a provider of deposition equipment for the semiconductor industry. The company develops, manufactures and installs systems for the deposition of complex semiconductor materials and offers deposition processes, consulting, training, customer support and service for these systems. It also offers peripheral equipment and services for the operation of its systems. The company also supplies deposition equipment for mass production, research and development (R&D) and pre-series production.

Number of employees: 1,057

Research and development (R&D) In addition to the R&D center at the headquarters in Herzogenrath, Germany, AIXTRON maintains a further development center in Cambridge, UK. The laboratories, which are equipped with AIXTRON systems, are used to research and develop new systems, materials and processes for the manufacture of semiconductor structures. The innovation center with over 1,000 m² of clean room space is located at the Herzogenrath site. This center specializes in the development of future system generations, particularly in the area of 300 mm wafer technology.

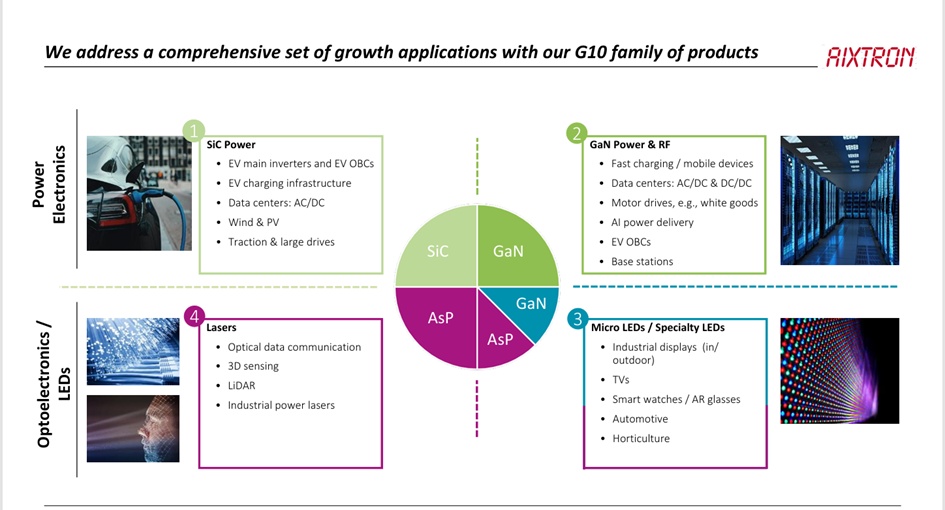

AIXTRON invests specifically in research and development projects to maintain and expand its leading position in deposition systems for applications such as lasers, micro LEDs, specialty LEDs, memristors and the production of wide-band-gap materials for power electronics. The company is also working on innovative 2D nanostructures, which are currently considered to have great potential in research.

AIXTRON aims to secure its technologies via corresponding patents if these are strategically expedient for the Company. As of December 31, 2025, the Group had 306 patent families

Competitive position AIXTRON operates in a global, highly competitive environment for deposition equipment for the deposition of compound semiconductors based on CVD and MOCVD technologies. Key competitors include:

- Veeco Instruments Inc. (USA) ("Veeco")

- Taiyo Nippon Sanso (Japan) ("TNS")

- Tokyo Electron Ltd (Japan) ("TEL")

- ASM International N.V. (Netherlands) ("ASM")

- Nuflare Technology Inc (Japan) ("Nuflare")

- Advanced Micro-Fabrication Equipment Inc (China) ("AMEC")

- Beijing NAURA Microelectronics Equipment Co, Ltd (China) ("Naura")

- Zhejiang Jingsheng Mechanical & Electrical Co, Ltd (China) ("JSG")

- Tang Optoelectronics Equipment Corporation Limited (China) ("TOPEC")

- Agnitron Technology Inc (USA) ("Agnitron")

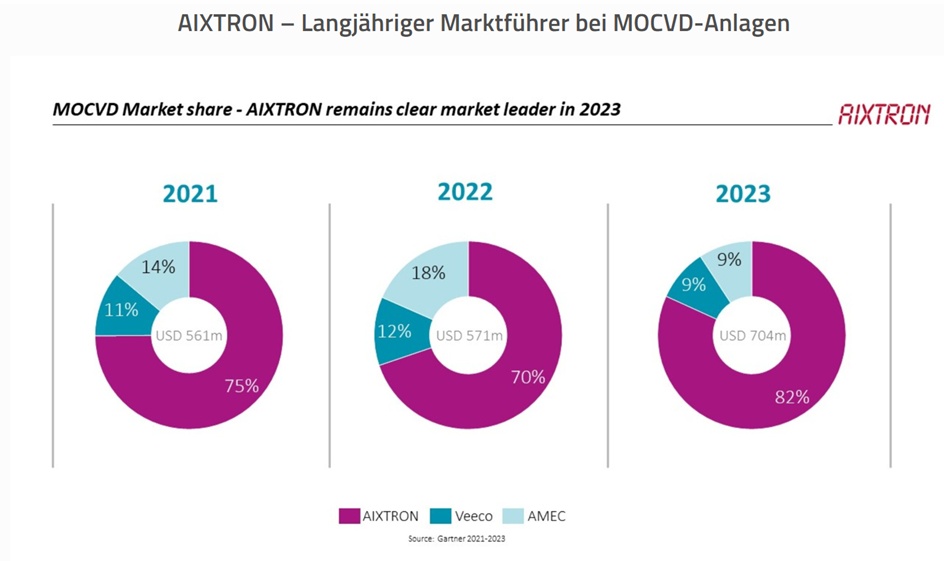

According to data from the market research institute Yole Group, AIXTRON has maintained its global market leadership in MOCVD systems for compound semiconductors in 2024. The estimated market share is 77%. Veeco (USA) follows with 8%, Tokyo Nippon Sanso (Japan) with 5% and AMEC (China) with 4%. According to estimates, the global market volume for MOCVD systems amounted to around USD 550 million in 2024 (previous year: USD 580 million)

In the field of CVD systems for silicon carbide, AIXTRON recorded a market share of around 27% in 2024, according to the Yole Group. This positions the company between ASM (Netherlands) with 32% and Tokyo Electron (Japan) with 16%. The global market volume for SiC CVD systems amounted to around USD 500 million (previous year: around USD 520 million).

AIXTRON's customer base is broadly diversifiedbut 2025 was clear:

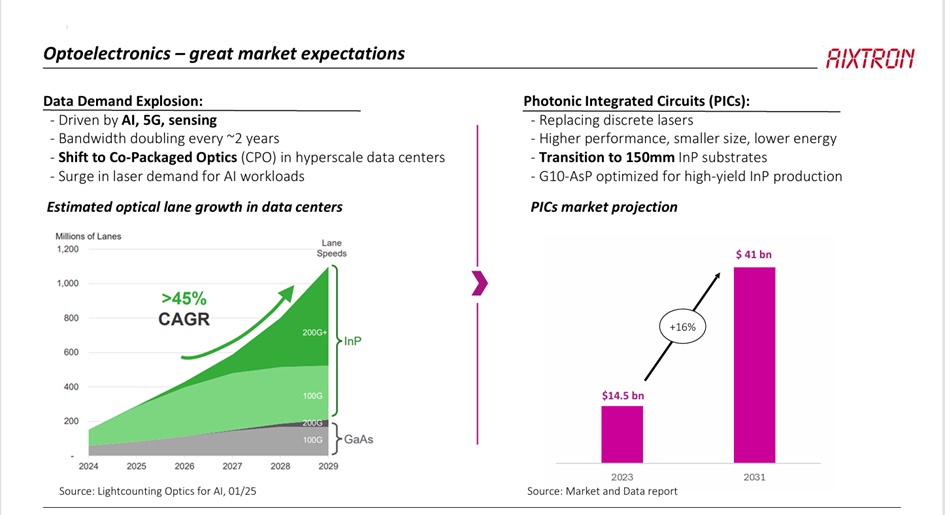

- Optoelectronics = growth driver

- China = strongest market

- Power electronics in the West = weak

- LED/Micro-LED = declining

This structure also explains the volatility in incoming orders and the strategic focus on new platforms (G10-SiC, 300 mm GaN, G10-AsP).

Jefferies rates Aixtron a 'Buy' - Target 36.50 euros

26.3.2026 08:35:01 | Source: dpa

NEW YORK (dpa-AFX) - Analyst firm Jefferies has maintained its Buy rating on Aixtron with a price target of 36.50 euros. Om Bakhda commented on the construction of a new plant in Malaysia in a study published on Thursday. The capacity expansion clearly reflects the confidence that demand will rise sharply in the coming years - especially from Asian customers of the chip industry supplier. He had previously indicated a capacity expansion as a possible share price driver./rob/tih/ck

Aixtron - machine manufacturer in the semiconductor industry could become a major beneficiary of the next wave of AI expansion.

According to the Börse Online (issue 47/2025), the majority of AI investments bypass Germany. However, the M and TecDAX company Aixtron [WKN: A0WMPJ, ISIN: DE000A0WMPJ6] as a latecomer, must be seen as having great potential in its plan to become a supplier of high-tech machines for semiconductors used in the operation of data centers.

A tripling of installed capacities in data centers from the current 82 GW to 219 GW in 2030 will not happen without improvements in the speed and energy efficiency of the semiconductors required.

GaN technology should be in demand with the use of Nvidia's 800-volt database technology

Aixtron addresses precisely these issues with its machines for the production of coated semiconductors, laser technology and optical components. The US hedge fund Kerrisdale sees potential for silicon carbide semiconductors in the energy sector.

However, the new 800-volt database technology from Nvidia is likely to have an even stronger growth impact on Aixtron's business. The 800-volt direct current technology requires semiconductors with gallium nitride (GaN) for a higher switching speed.

Aixtron is one of the pioneers in GaN semiconductor manufacturing equipment. Aixtron is conducting tests with pilot systems with numerous chip manufacturers. If Nvidia uses the new 800-volt technology in all its products from 2027, Aixtron's currently low business volume is likely to increase significantly, as other semiconductor manufacturers are then also likely to rely on corresponding technologies.

Strong market position in the field of coating technologies should ensure a full order book

Aixtron already holds a high market share in coating technology. With the launch of the 800 volt technology, the order book should fill up again significantly from next year at the latest.

The US investor Kerrisdale even believes that Aixtron can achieve annual sales of more than EUR 1 billion in the coming years based on these prospects, after expected sales of EUR 540 million for 2025.

If the business then scales, earnings of up to EUR 2 per share are conceivable from 2028. According to Kerrisdale, if this result is compared with the current multiples of other equipment suppliers, there is a share price potential of more than 200%. Börse Online initially advises a target price of 25 euros for entry (42 % potential).

AIXA FY-2025 Results Presentation.pdf

Geographical distribution of sales:

(2025 EUR)

China 232 million

USA 106 million

Europe (excluding German) 62.22 million

Germany 51.37 million

Japan 46.2 million

Taiwan 35.41 million

Korea 15.87 million

Americas (excluding USA) 4.36 million

Malaysia 1.72 million

Asia (excluding China/Taiwan) 0.97 million

EUR in millions

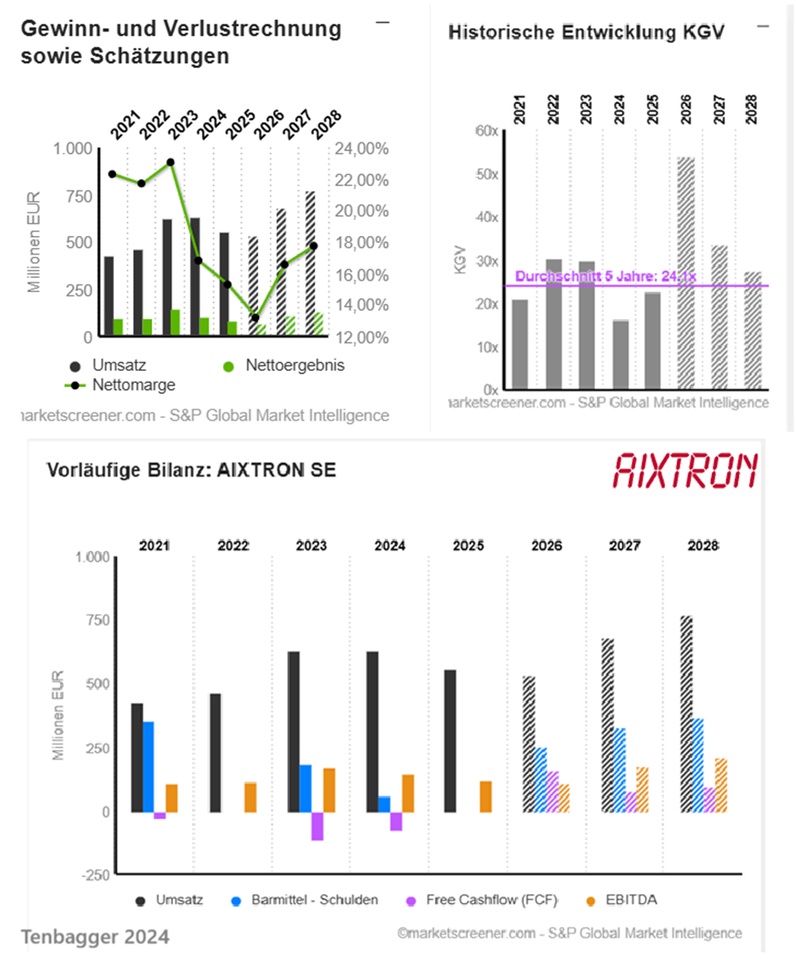

Estimates

Year Turnover Change

2025 556,6 -12,1 %

2026 533,9 -4,07 %

2027 679,8 27,33 %

2028 771,2 13,44 %

Year EBIT Change

2025 100,3 -23,58 %

2026 93,96 -6,31 %

2027 156,2 66,22 %

2028 189,3 21,21 %

Year Net result Change

2025 85,23 -19,81 %

2026 70,49 -17,29 %

2027 112,8 59,97 %

2028 136,8 21,36 %

Year Net debt CAPEX

2026 -251 30,26

2027 -328 28,78

2028 -368 31,07

Year Free cash flow Change

2024 -72,47 34,07 %

2026 160,1

2027 76,65 -52,14 %

2028 94,44 23,21 %

Year EBIT margin ROE

2025 18,02 %

2026 17,6 % 7,55 %

2027 22,97 % 11,4 %

2028 24,55 % 12,86 %

Year Earnings per share Change

2025 0,76 -19,15 %

2026 0,6291 -17,22 %

2027 1,007 60,03 %

2028 1,232 22,34 %

Year Dividend p share Yield

2026 0,1717 0,53 %

2027 0,2213 0,68 %

2028 0,2859 0,88 %

Year FCF Yield

2026 4,68 %

2027 2,29 %

2028 2,86 %

Year P/E ratio PEG

2025 22.8x -1.2x

2026 51.7x 3.81x -3x

2027 32.3x 3.46x 0.5x

2028 26.4x 3.13x 1.2x

Market value 3,671

Number of shares (in thousands) 112,786

Date of publication 26.02.2026

Aixtron since 11.06.2025 approx. 155 percent