Week 10 of 2025 delivers a tanker market of contrasts. VLCCs remain flat with balanced tonnage, while Suezmax tightens and lifts rates in Europe and West Africa. Aframax softens under weak demand, as clean tankers—MRs and LRs—display regional divergence: LR2s recover in the East, but MRs face pressure in the West. Geopolitical risks escalate with U.S. tariff threats, potential Iranian interdictions, and Canada’s export surge, impacting $6.7bn of U.S.-listed tonnage. Investors eyeing shipping or oil markets face a blend of stability, opportunity, and uncertainty.

This update spans VLCC, Suezmax, Aframax, MR, and LR trends, plus key external drivers. From rate shifts to regulatory clouds, here’s the latest—volatility remains a fixture.

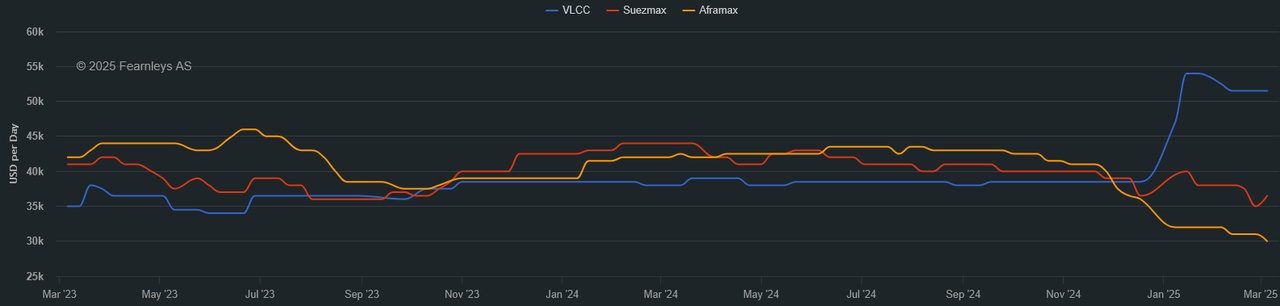

⏬ VLCC Market: Steady with Latent Potential

VLCCs stayed level this week, with MEG to China (TD3C) at WS* 57.10 ($38,342/day round-trip TCE, up $1,000 w-o-w) and West Africa to China (TD15) at WS 58.50 ($40,633/day TCE). U.S. Gulf to China (TD22) plunged $767,500 to $7.28M ($36,497/day TCE), reflecting a $4,700/day drop. MEG/East rates held at WS 57 for modern ships—older units saw discounts—while West Africa activity rose above WS 60, bolstering owner sentiment despite weak U.S. Gulf exports. Breakwave Advisors flags tight dark fleet supply, with Iran’s February loadings down 37% m-o-m due to “clean” STS vessel shortages and Shandong bans. China’s refining strength (gasoil at historical norms, gasoline two-thirds above) contrasts Brent’s 2021 low—OPEC+ cuts easing and Russia sanction talks could lift VLCCs. Investors might note this stability, with geopolitical shifts as a wildcard.

⏳ Suezmax Market: Tight Lists Push Rates

Suezmax enjoyed a busy Tuesday, with Europe and West Africa cargoes trimming tonnage lists and nudging rates up. Nigeria to UK Continent (TD20) gained 2.5 points to WS 87.83 ($36,548/day TCE), and CPC to Med (TD6) hit WS 100.9 ($39,838/day TCE), while MEG to Med (TD23) reached WS 91. Five cargoes remain open, suggesting further upside as sentiment strengthens—TD20 and TD6 both rose 2.5 points from last fixtures. In the U.S. Gulf, tonnage is tight for March 10-20, with solid WTI exports to Europe, yet Aframaxes at WS 150 snag stems from Suezmaxes. MEG tonnage is scarce, but quiet volume and laycans shifting to mid-March dampen owners’ leverage. Breakwave sees VLCCs leading geopolitically, but Suezmax resilience here hints at regional gains—cargo flow will be key.

⏱️ Aframax Market: Demand Lags, Rates Soften

Aframax markets opened the week quietly in the West. North Sea’s scant activity left a long prompt tonnage list, easing TD7 (Cross-UK Continent) to WS 107.5-110 ($27,000/day TCE) with downward pressure building. Mediterranean/Black Sea demand weakened, dropping TD19 (Cross-Med) 3.5 points to WS 121.28 ($29,733/day TCE), as prompt ships linger and Suezmaxes dominate. In the Americas, Mexico’s stem cancellations tanked TD26 (Mexico/U.S. Gulf) and TD9 (Covenas/U.S. Gulf) 10 points to WS 132.78 ($25,687/day TCE) and WS 130.94 ($24,833/day TCE), while TD25 (U.S. Gulf/UK Continent) fell 15 points to WS 143.89 ($34,447/day TCE). Canada’s Trans Mountain Pipeline spiked exports 59% y-o-y to 373,000 bpd, with Aframaxes (75% of Vancouver loads) serving Asia—yet U.S. tariffs loom large. Ballasting remains viable; softness may deepen without a demand spark.

1 Year T/C - VLCC SUEZMAX AFRAMAX ECO / SCRUBBER - March 5th

⏸️ MR Market: Western Pressure Persists

Medium Range (MR) tankers faced a softening week. MEG’s TC17 (35kt MEG/East Africa) peaked at low WS 220s early but fell to WS 211.79 as activity cooled. UK-Continent’s TC2 (37kt ARA/U.S. Atlantic) dropped from WS 152.5 to WS 135 ($13,500/day TCE), and TC19 (37kt ARA/West Africa) hit WS 157.81 ($19,216/day TCE), chipped away over five days. In the U.S. Gulf, TC14 (38kt U.S. Gulf/UK-Continent) eased to WS 85, TC18 (U.S. Gulf/Brazil) fell to WS 137.86, and TC21 (U.S. Gulf/Caribbean) lost $35,715 to $403,571—bottoming out amid slow demand. Breakwave notes NW Europe CPP loadings supporting TC2, yet rising MR ballasters from a closed U.S. Gulf arbitrage cap gains. Russia’s 9% February diesel drop adds supply pressure—MRs may struggle unless U.S. summer demand shifts the tide.

⏹️ LR Market: Eastern Gains, Western Stagnation

Long Range (LR) tankers showed regional splits. MEG LR2s rose, with TC1 (75kt MEG/Japan) up 6.11 points to WS 130 and TC20 (90kt MEG/UK-Continent) steady at $3.3M, fueled by diesel and jet demand—Breakwave sees light distillates driving Pacific LRs. LR1s lagged, with TC5 (55kt MEG/Japan) down 3.75 points to WS 134.69 and TC8 (65kt MEG/UK-Continent) dipping to $2.67M, reflecting quieter activity. West of Suez, TC15 (Med/East) held at $2.85M, but UK-Continent’s TC16 (60kt ARA/West Africa) fell from WS 123.61 to WS 113.33 as demand faltered. Breakwave flags rising LR availability in MEG short-haul trades, capping rate upside despite naphtha import potential for Asia’s refinery season. LR2 resilience contrasts LR1 and Western softness—watch distillate trends for direction.

🌐 Geopolitics & Risks: Costs and Flows in Flux

External forces are rattling the market. The U.S. considers interdicting Iranian tankers (1.7M bpd exports, a 4-year high) via the Proliferation Security Initiative, risking trade disruptions. Trump’s $1M-$1.5M fees on Chinese-built ships threaten $6.7bn of U.S.-listed tonnage—Teekay Tankers (44.4%), Frontline (35.8%), and others face hikes that could raise freight costs or divert buyers to non-U.S. crude. Canada’s 59% export surge (373,000 bpd) via Trans Mountain aids Aframaxes, but 10% U.S. tariffs cloud the outlook. Breakwave sees VLCCs gaining most from 2025’s turbulence—China’s discounted crude demand persists despite sanctions. Investors might weigh tariff exposure against tonnage tightness—uncertainty’s baked in.

🚨 Outlook: Diverging Fortunes

VLCCs could rise if Russia sanctions ease or Iran flows shift, favoring mainstream tonnage per Breakwave. Suezmax may firm further with Europe/West Africa cargoes, though U.S. Gulf lags. Aframax softness persists without demand, despite Canada’s boost, while MRs face Western pressure and LRs eye Eastern distillate gains. Geopolitical risks—tariffs, interdictions—could lift costs, favoring compliant tonnage, but mute U.S. export edges. Investors might find selective plays—VLCC and Suezmax strength versus MR/Aframax risks—amid a volatile backdrop.

💬 Your Take?

Where do you see tankers heading? Bullish on VLCCs, or wary of MR softness? Share your view—let’s dive in! 🚢

*The Worldscale (WS) rate is a system used to calculate tanker freight rates, where WS 100 represents a standard base rate for a specific route. Rates above or below this benchmark indicate how much more or less a charterer will pay relative to the base cost. A higher WS rate means better earnings for shipowners, while a lower WS rate means lower transportation costs for charterers.