After weeks away, I’m back ✌️

Things have been a bit quiet around here over the past few weeks because I was on a tour of Japan. Unfortunately, that meant I wasn’t able to contribute regularly or write posts here 🙇♂️

It was actually my first trip to Japan, and I have to admit: I’m absolutely thrilled and fascinated by this country! 🇯🇵

If you haven’t had the chance to travel to Japan yet, I can’t recommend it highly enough.

Even though the focus was, of course, on traveling, I couldn’t help but keep my eyes open for exciting companies and business models.

And that’s exactly why I’d like to introduce a company today that particularly impressed me during my trip. I had the opportunity to view the company not only from an investor’s perspective but also to experience it firsthand as a customer. In fact, I even visited the stores several times. What can I say? The company literally blew me away. The way the stores are set up, the layout, the product selection, the presentation of the merchandise, and the entire shopping experience left a lasting impression on me.

Today, I’m talking about Pan Pacific International Holding (Don Quijote) $7532 (-2.9%)

While the global retail world is glued to Amazon’s quarterly figures $AMZN (+0.03%) or laments the decline of brick-and-mortar retail in the West, a retail empire has established itself in Japan that breaks all the traditional rules of e-commerce: Pan Pacific International Holdings $7532 (-2.9%) , world-renowned for its iconic discount chain Don Quijote (“Donki”).

PPIH $7532 (-2.9%) doesn’t build online stores and doesn’t rely on sterile, algorithmically optimized shelves. PPIH $7532 (-2.9%) builds physical labyrinths that trigger the human hunting instinct. The company is the undisputed ruler of Japan’s discount retail sector and, through its “experiential shopping” concept, is challenging the dominance of online retail.

The difference from regular supermarkets is fundamental: Standard retailers sell interchangeable consumer goods through price wars—PPIH $7532 (-2.9%) sells a “treasure hunt” model with an integrated negative cash conversion cycle. The more domestic inflation takes its toll, or the more massive the global tourism boom sweeps over Japan, the more crowded the aisles at Don Quijote become. Without PPIH $7532 (-2.9%) , there would be no duty-free souvenir hotspot in Japan and no successful export model for Japanese food culture throughout Asia.

1. The Business Model: The Labyrinth Principle of Retail Success ⚙️💎

PPIH $7532 (-2.9%) controls the influx of impulse buyers in the Asian region through a perfectly balanced triad that combines operational leverage with an ingenious working-capital-based financing model.

① The Store Network (Experiential Shopping Infrastructure): PPIH $7532 (-2.9%) develops and operates the Don Quijotestores, the massive MEGA Don Quijotecenters, and the supermarket chains Apita and Piago. Whether in Tokyo’s high-traffic downtown districts (Shibuya, Shinjuku) or strategically located in other Asian countries (DON DON DONKI), these stores attract a steady stream of customers thanks to their 24/7 hours of operation.

② The “Treasure Hunt” Moat (Impulse Purchases): The true stroke of genius in this model: The intentionally winding aisles, crammed to the ceiling, create sensory overload. Statistically, customers spend significantly more time in the store. Since the product selection is constantly changing (clearance items, trendy products, exotic goods), every shopping trip becomes an adventure. This cannot be replicated online—Amazon’s algorithm cannot replicate the fun of unplanned discovery.

③ The scaling lever: Since PPIH $7532 (-2.9%) settles payments for its customers’ merchandise immediately in cash or by card, but—due to its enormous market power—does not have to pay suppliers until weeks later, PPIH operates with a negative cash conversion cycle. PPIH $7532 (-2.9%) collects the money, before its suppliers’ invoices are due. Growth is thus essentially financed as an interest-free loan through operating activities.

2. The Strategy: Why Inflation and Tourism Drive PPIH $7532 (-2.9%)

📐

PPIH’s strategic unique selling proposition $7532 (-2.9%) is based on a relentless ability to adapt to macroeconomic trends, fueled by two megatrends:

The global tourism boom & tax-free monopoly: Japan is experiencing an unprecedented influx of foreign tourists. Don Quijote has established itself as the undisputed No. 1 destination for duty-free shopping (cosmetics, snacks, luxury secondhand goods). The tax-free sales are skyrocketing and generating extremely high-margin revenue, as tourists statistically fill significantly larger shopping baskets than locals.

Private-Label Margin Leverage (Passion People / PB): To counter domestic inflation, management is radically increasing the share of its private-label brands (Private Brand / OEM). Private-label volume recently climbed rapidly to over 317 billion JPY. Since private labels eliminate the intermediary’s margin, PPIH is structurally increasing its gross margin while simultaneously guaranteeing the lowest prices in the country (trading-down effect).

Store Consolidation via M&A: PPIH $7532 (-2.9%) is not only growing organically domestically but is also skillfully acquiring struggling competitors (such as the Olympic Group via a stock swap) or traditional chains to transform their locations into highly profitable Donkistores in the blink of an eye.

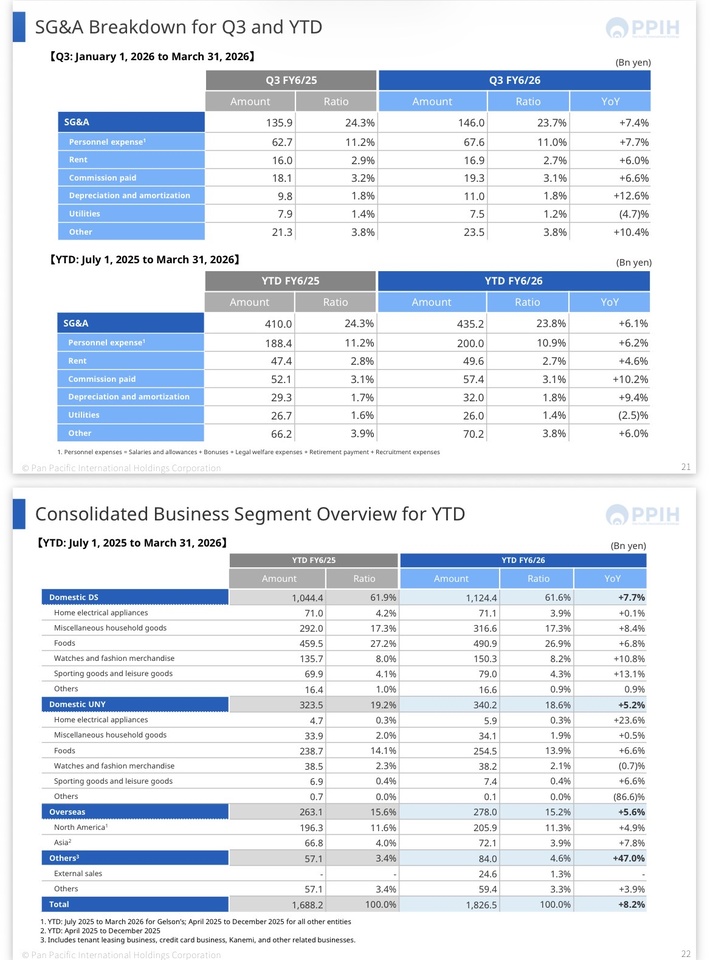

3. Key Figures 📊

Market capitalization: ~2.5 trillion JPY (approx. 15 billion EUR). A liquid, crisis-resistant heavyweight on the Tokyo Stock Exchange.

🚀Revenue growth (5-year CAGR):

+9.4% – a phenomenal and consistent growth rate for a traditional retailer.

🚀EBIT Margin / Operating Leverage:

7.2% – This may sound low compared to tech stocks, but in the discount retail sector, it’s absolutely top-tier. The operating leverage is working perfectly: While revenue recently rose by 7.2%, operating profit (EBIT) skyrocketed by +15.8%.

🚀Return on Invested Capital (ROIC):

13.4% – An outstanding figure for a capital-intensive retailer, well above the local Japanese cost of capital (WACC: 5.85%).

🚀EPS growth (5-year CAGR):

+16.1% – Demonstrates the high quality of earnings per share growth.

🚀Balance Sheet Strength:

Net Debt/EBITDA of 1.4x. Despite recent issuances of new unsecured bonds to finance expansion, the balance sheet remains rock-solid. An interest coverage ratio of 24.0xmakes the competition in the West look outdated.

4. Why is the stock so exciting RIGHT NOW? 🚀

✅Successful stock split: Last winter, a 5-for-1 stock splitwas carried out. As a result, the price was visually adjusted from the ~4,000 JPY range to the current level of ~813 JPY , making the stock extremely liquid for retail investors and inflows.

✅Technical pullback offers an entry opportunity: From its all-time high of 1,139 JPY, the stock has given up about 25–30% amid a healthy market pullback and is currently trading at an extremely strong technical support level just above the annual low. The “tech tourists” are out; the fair value remains.

✅The “Visionary 2030” pipeline: PPIH $7532 (-2.9%) has smashed its previous, ambitious targets (“Visionary 2025”) a full year ahead of schedule. Now, the strategic rollout of the new grocery format “Robin Hood” is underway, which is expected to generate hundreds of new, highly profitable stores by 2035.

✅Asia as an unsaturated growth market: While the U.S. expansion (Gelson’s) is still being consolidated, international operations in Asia (DON DON DONKI) is delivering a veritable profit explosion (+222% in the segment). The concept of affordable Japanese food culture is a huge hit in Singapore and Hong Kong.

5. Competition & Moat ♟️

The landscape: The traditional Japanese retail sector is fragmented (Aeon, Seven & i Holdings). But in the true experiential discount segment, PPIH $7532 (-2.9%) effectively holds a monopoly. No one else masters the combination of non-food, food, 24-hour operation, and duty-free mass processing on this scale.

E-commerce (Amazon $AMZN (+0.03%)

/Rakuten $4755 (-1.83%) ) No direct competitors. They sell convenience and predictability. Don Quijote sells entertainment, browsing, and the immediate dopamine rush of a bargain.

PPIH’s Moat at a Glance:

⭐️ Unique store psychology: The labyrinth-like layout prevents quick online price comparisons and maximizes revenue per square meter through impulse purchases.

💪Purchasing Power & Supplier Leverage: Thanks to its sheer purchasing volume, PPIH secures $7532 (-2.9%) secures clearance items and brand-name goods at prices no other brick-and-mortar retailer can match.

🔁Negative Cash Conversion Cycle: A financial moat that allows PPIH $7532 (-2.9%) to expand faster than the competition without burdensome bank loans.

6. Risks ⚠️

❗️Yen appreciation risk (FX/tourism): A significant portion of the current earnings potential depends on the weak yen, which drives tourist flows to Japan. If the Bank of Japan (BoJ) were to raise interest rates drastically and the yen were to appreciate sharply, this would dampen the tax-free boom.

❗️U.S. Margin Headwinds: The U.S. business (Gelson’s in California) operates in a highly competitive, high-price market and is currently dragging down the rock-solid margins of the Asian business slightly.

❗️Overseas execution risk: Cultural incompatibilities abroad could slow expansion. Not every market reacts as enthusiastically to the chaotic Donkiconcept as Southeast Asia does.

✍️My personal conclusion & Reaper bonus

PPIH (Don Quijote) $7532 (-2.9%) is, fundamentally, an absolutely exceptional phenomenon in the global retail sector. The company delivers the growth rates of a tech stock, protected by a brick-and-mortar concept that is immune to digitalization. Following the healthy technical correction in the spring of 2026, the CRV has become extremely attractive. Here, top quality is available at a reasonable price.

💀 Jack’s Verdict:

“PPIH is the antithesis of the dying retail sector in the West. While Walmart $WMT (-0.92%) and Co. spend billions trying to chase Amazon $AMZN (+0.03%) online, Donki is simply building a physical maze, and people are flocking to their stores. The best part for us investors: After the 5-for-1 split this winter, the stock looks ridiculously cheap on paper, and a forward P/E of 22 for a cash flow machine with negative working capital is almost outrageously fair. Anyone who doesn’t at least invest an initial tranche at ~810 JPY to profit from the unstoppable surge in tourism to Japan is fundamentally beyond help. Quality comes at a price, but right now we’re getting it at a discount.”

REAPER RATING: 🟢 STRONG BUY

REAPER SCORE:

8.4 / 10

@Get_rich_or_Die_tryin @Tenbagger2024

@Raketentoni

@PikaPika0105

@Dividendenopi

@Stocktective

@schlimmschlimm and, of course, everyone else ✌️