I've been looking for a company from the emerging markets that might be a good fit for my portfolio for a while now.

Far away from the big earnings, I struck today and bought the first tranche. $PAC (+1.06%) has now moved in with me.

For those who are interested, I have put together the most important information so that you can get a rough overview.

The text comes without AI very quickly in bullet points 🧐

$PAC (+1.06%) offers a boring business, but it is very profitable and could be of interest to some people who are interested in cash flow 💸.

It operates 12 airports, mainly in Mexico and one in Jamaica among them:

- Guadalajara (important for industry)

- Tijuana (keyword nearshoring/USA)

- Los Cabos & Puerto Vallarta (tourism)

As you can already guess, the main income comes from regulated tariffs for landings/take-offs and from the non-regulated business of duty-free and parking.

Who is responsible for the positive development?

Raul Revuelta Musalem (CEO) has been at the helm since 2018 $PAC (+1.06%) since 2018 and is considered one of the most effective CEOs in the transportation sector. With over 20 years of experience in finance and infrastructure, the money seems to be in good hands with him. The main focus is on cost control and maximizing margins with over 65% EBITDA a flagship for such a cost-intensive sector.

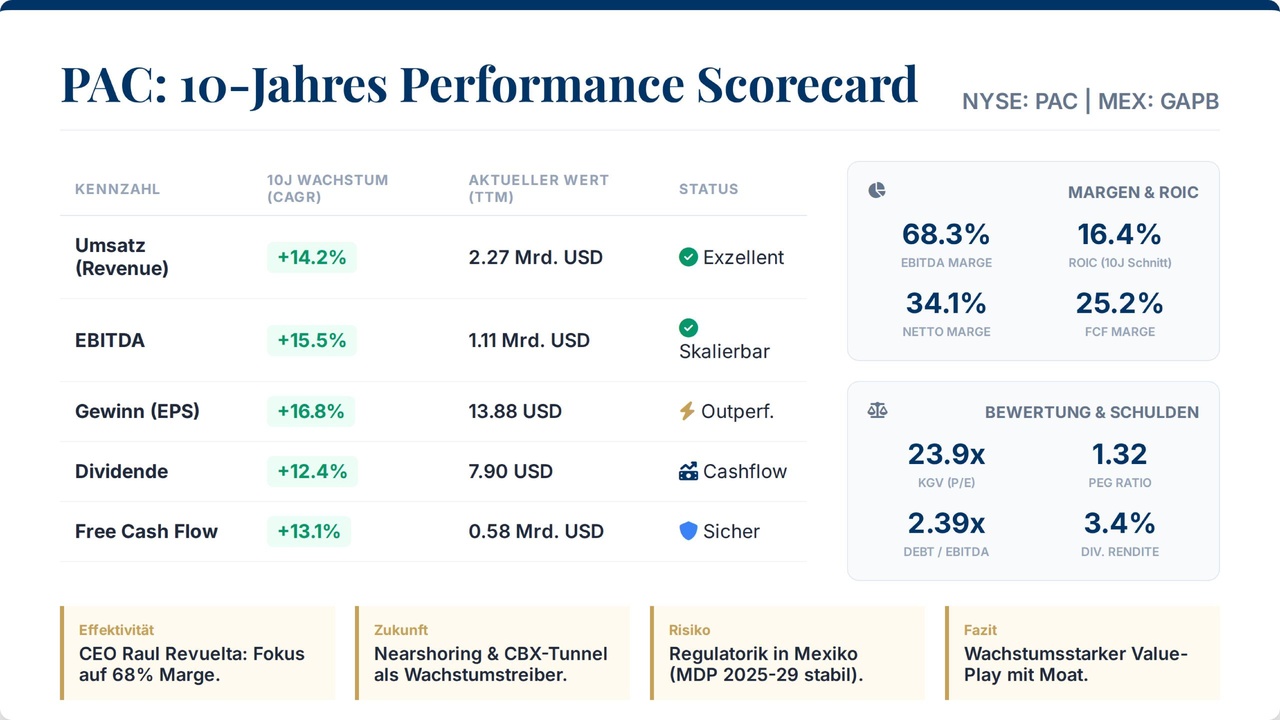

Without further ado, here is a quick and dirty overview of some of the most important data 🛩️

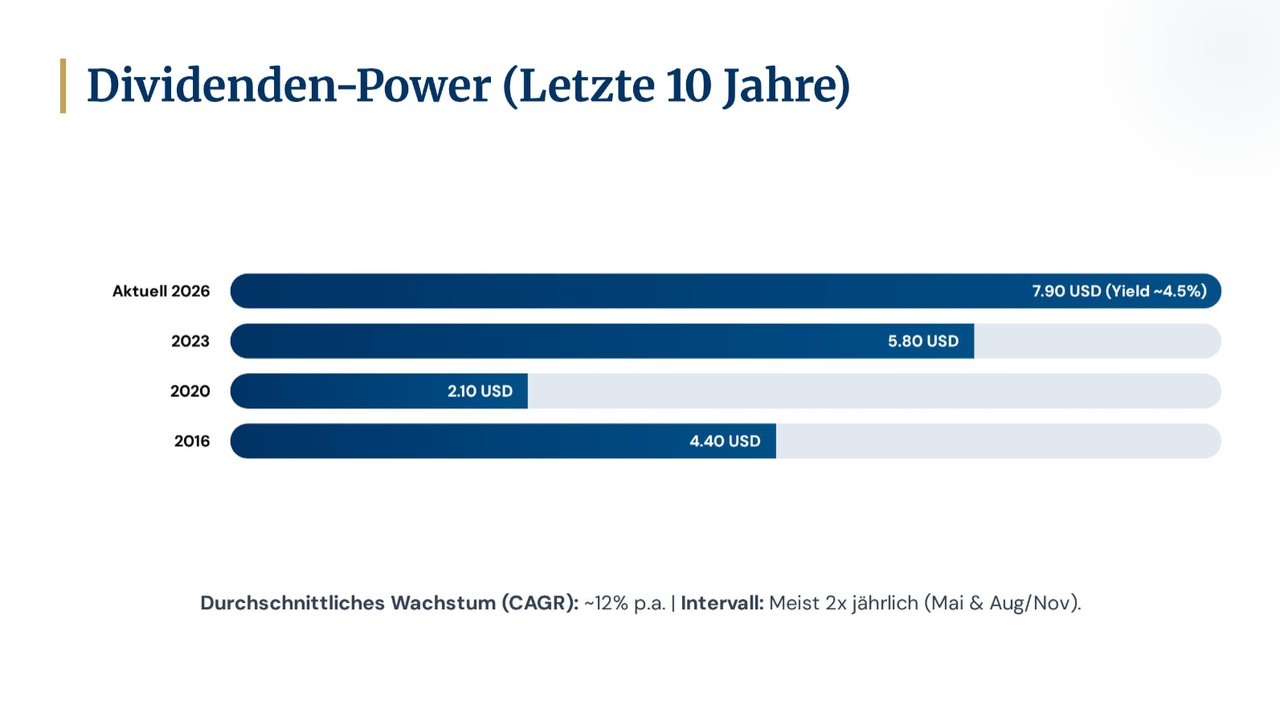

My Monk thinks that the very reliable and predictable quarterly dividends of the strong US stocks are excellent, but I believe that we cannot deny the Mexicans entry based on their performance.

The recovery after Covid is decent and I think the figures speak for themselves. This is less about speculation and quick price gains, but it is a quality company from Latin America with relatively good growth prospects ✅

What is the current situation? There was a small dip in February that I unfortunately wasn't able to take with me, as the passenger figures from tourism were somewhat disappointing. Otherwise, the share price seems to be moving in the right direction again, and I think it's currently still available at a fair price.

But what does the near future hold?

- The World Cup in Mexico, where we could see very good figures in the short term

- Relocation of industry from China to Mexico, where Mexican transshipment points could benefit as Mexico is an increasingly important partner of the USA

- Keyword CBX, $PAC (+1.06%) is making efforts to enter the market operationally. The Cross Border Xpress is virtually an exclusive terminal that connects San Diego and Tijuana, thus simplifying the normal crossing of borders.

- Tariffs and investments with the state are already signed and sealed until 2029, so there are no surprises here for the time being

What about the risks?

- Clearly subject to $PAC (+1.06%) political regulation

- Global crises ala Covid can seriously affect the business

- Currency risk/emerging markets

Why did I choose $PAC (+1.06%) decided? On the one hand, the figures are more than solid, there is a certain moat and there is no need to be afraid of the competition, plus there is a synergy on my infrastructure bet that includes Mexico/USA & Canada, which is why I invested in $CP (+0.99%) at the end of last year. I am aiming for a size of around 20 shares for the time being, and I would also like to $CP (+0.99%) hopefully I can complete this by the end of July.

What do you think of boring cash flow moats? Have I missed something and am I completely wrong? Will Mr. Prompt be gracious with my thought processes? 😰 @Raketentoni

PS: Despite ADR and the NYSE being open, you pay a decent spread here, so I can't actually sell anymore 🫡