Hello community,

Since the high in 2020, the Alibaba share price has fallen massively. Sentiment is at rock bottom. But that is precisely what makes an in-depth analysis so exciting. Is the fear exaggerated or justified?

Let's take a deep dive into the figures and the story behind the Chinese giant.

WHAT'S BEHIND ALIBABA $BABA (-0.19%) 🇨🇳

Alibaba is much more than just an online store. It is a huge ecosystem that is currently reinventing itself and splitting into six parts:

🔵 Taobao & Tmall GroupThe e-commerce centerpiece.

🔵 Cloud Intelligence Group: The AWS of China and the basis for the future of AI.

🔵 Cainiao Smart Logistics: The logistics network.

🔵 Other divisions: Local Services, Global Digital Commerce & Entertainment.

ALIBABA IN FIGURES (TTM) 📊

The real story is in the key figures - where stagnation meets massive profitability.

💰 Turnover TTM~$130 bn (+5% YoY)

👥 Annual Active Consumers: ~1 bn (stable)

☁️ Cloud revenue: ~$15 bn (growing & profitable again)

💸 Free cash flow (FCF) TTM: ~$21 bn (extremely high cash generation)

🏦 Net cash position: ~$60 bn (massive war chest)

✅ P/E ratio (forward): ~8 (historically extremely favorable)

OPPORTUNITIES & RISKS

THE UPSIDE 🟢

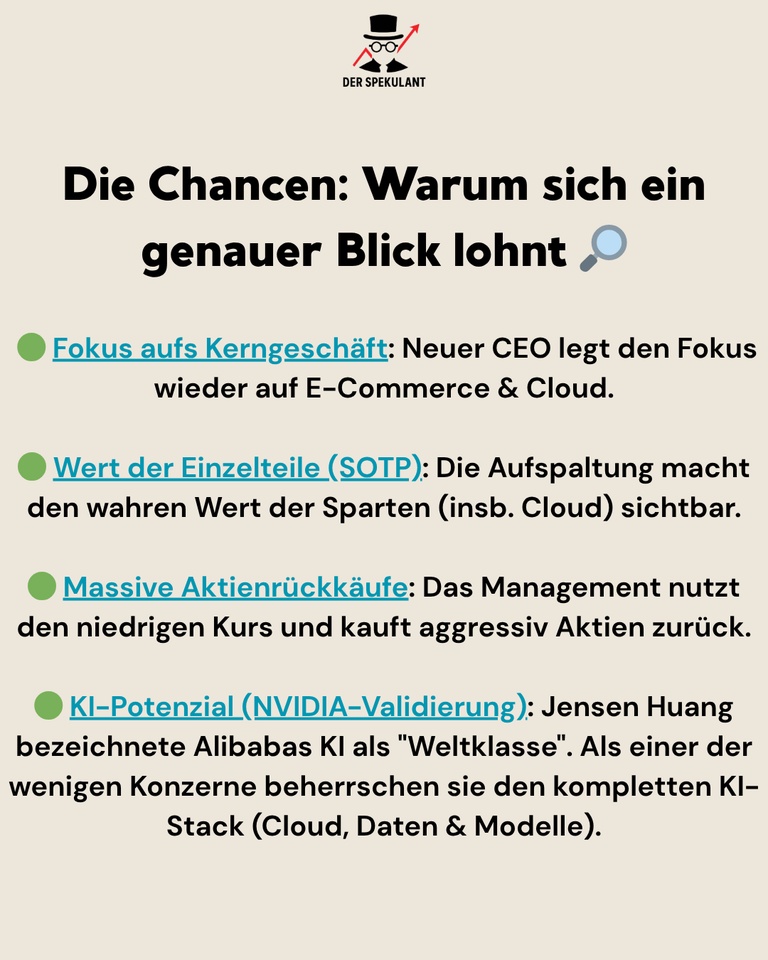

🟢 Value of the individual parts (SOTP): The breakdown makes the true value of the divisions (esp. cloud) visible.

🟢 Massive share buybacks: Management uses the low share price to aggressively create value for shareholders.

🟢 AI potential (NVIDIA validation): NVIDIA CEO Jensen Huang recently described Alibaba's AI model as "world class". They have mastered the complete 'AI stack' (cloud, data & models).

THE RISKS 🔴

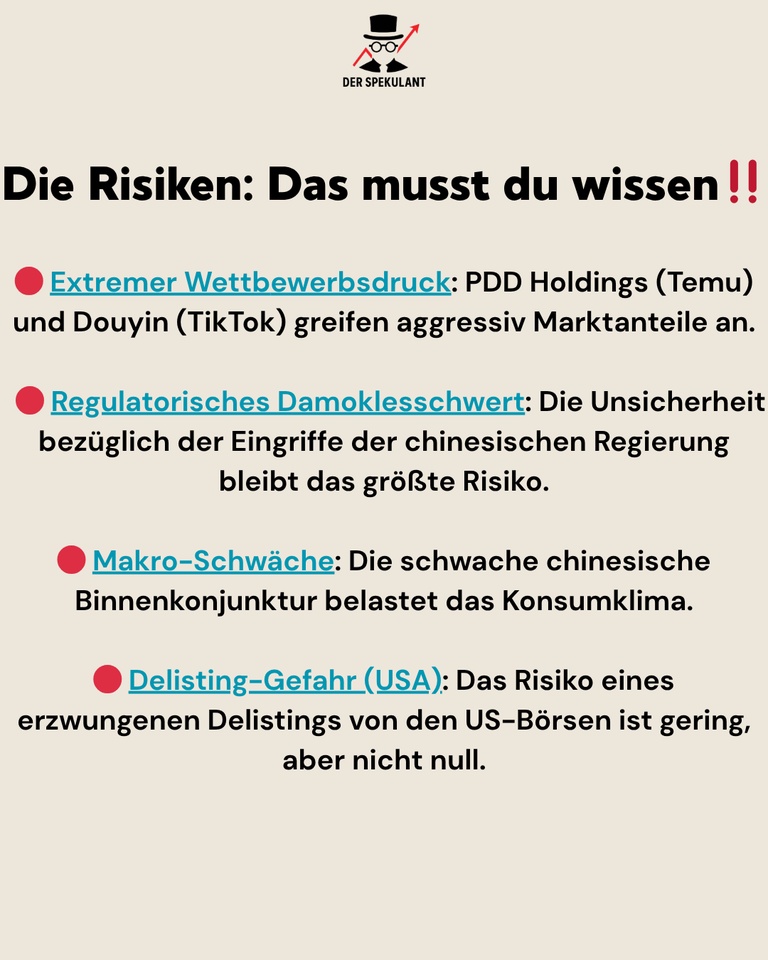

🔴 Extreme competitive pressurePDD Holdings (Temu) and Douyin (TikTok) are aggressively attacking market shares.

🔴 Regulatory sword of Damocles: Uncertainty regarding intervention by the Chinese government remains the biggest risk.

🔴 Macro weakness: The weak Chinese domestic economy is weighing on the consumer climate.

CONCLUSION & MY STRATEGY ⚖️

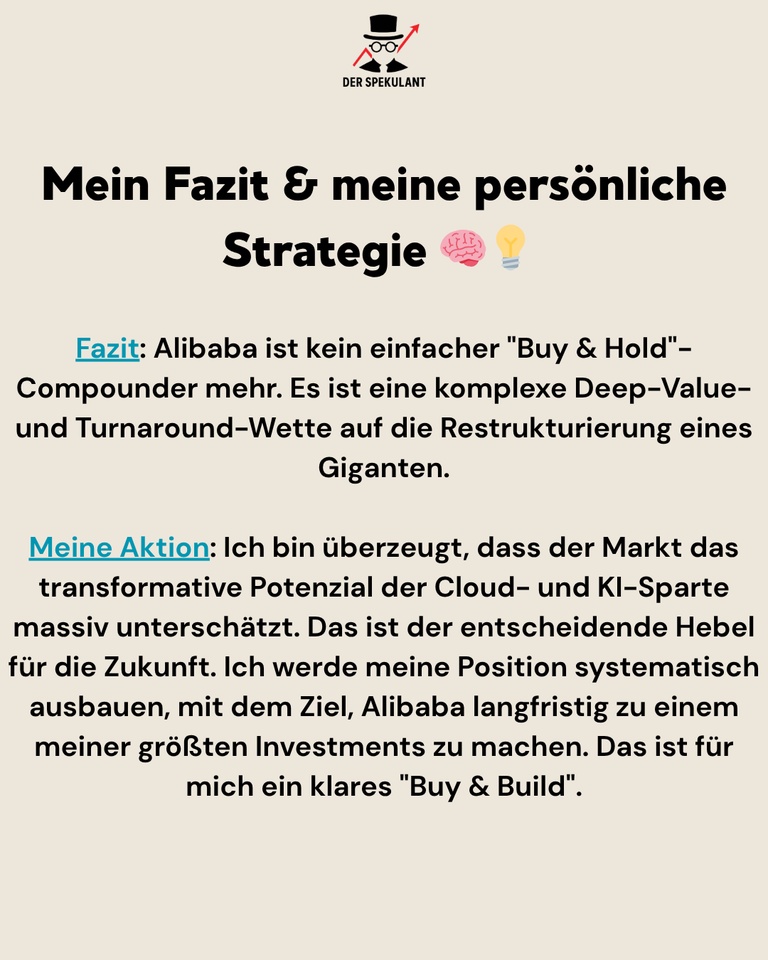

Alibaba remains a complex bet with valid risks, from competition from PDD to unpredictable regulation from Beijing.

For me personally, however, the long-term opportunity that lies in the cloud and AI division outweighs the risks. Today's valuation mainly prices in the risks, but hardly the enormous potential that can be leveraged through the restructuring and the AI technology validated by Jensen Huang.

The investment thesis:

My investment is a bet on the re-rating of the group, driven by the future monetization of cloud & AI, while the massive cash position and share buybacks provide downside protection.

My action:

I will systematically build my initial position into one of my core positions over the coming months and years. For me, this is a clear "buy & build" investment for the next decade.

How do you see it?

Is the risk too high or is this the definition of an anti-cyclical opportunity?

Looking forward to the discussion! 👇

#alibaba

#baba

#stockanalysis

#tech

#china

#ecommerce

#cloudcomputing

#valueinvesting

#künstlicheintelligenz