Country diversification is important!

Foreword:

I have noticed that many people have recently been thinking about adding a little more US exposure to their portfolio. The classic approach is to hold a FTSE All-World and then buy an S&P500 or NASDAQ100. Others consider selling their FTSE All-World and going 100% US. Still others happily buy stocks that already have the highest weighting in their FTSE All-World.

Reasons are often given such as:

- The other countries are just a drag on returns (performance chasing)

- Nothing works without the USA (markets are increasingly correlated)

- US companies earn their money worldwide (and are therefore automatically diversified)

What I find somewhat disconcerting is the matter-of-factness with which long-term portfolios are intervened in. People act as if the future is certain.

In the following, I would like to use the example of the USA to explain, as briefly and thoroughly as possible, why the above reasons are no substitute for country diversification.

I have linked the most important sources at the end.

1. valuations

In an article from 2021 entitled "The Long Run Is Lying to You" [1]

Cliff Asness showed that from 1980 to 2020, almost all of the outperformance of the S&P 500 versus the EAFE index (21 developed countries excluding the US and Canada) can be explained by the increase in the price of US stocks relative to their cyclically adjusted earnings.

US equities outperformed by around two percent per year, but adjusted for valuation changes, the outperformance was only around 0.4 percent per year. Adjusting for valuation changes is important because current valuations are one of the most meaningful metrics we have for estimating expected returns. If equity valuations are higher, returns will tend to be lower in the future, as described in: "Accounting valuation, market expectation, and cross-sectional stock returns" [2]

The 2022 paper "Is The United States A Lucky Survivor: A Hierarchical Bayesian Approach" [3] shows that U.S. stock returns have beaten their own expected returns by about two percent per year, which can be explained by two things.

A: U.S. companies have done better than expected due to disasters that did NOT occur. (such as Japan bubble in 1990, civil war, war at home, political instability, debt crises...) This has led to a learning process (B).

B: A learning process in which investors have come to believe that US equities are safer over time, which has driven up their valuations. (the author assumes a turkey illusion https://en.wikipedia.org/wiki/Turkey_illusion)

2. currency risk:

If you heavily overweight a country / currency area in your portfolio, you are exposing yourself to currency risk, whether consciously or unconsciously. A bet on the USA is also a bet on a strong US dollar.

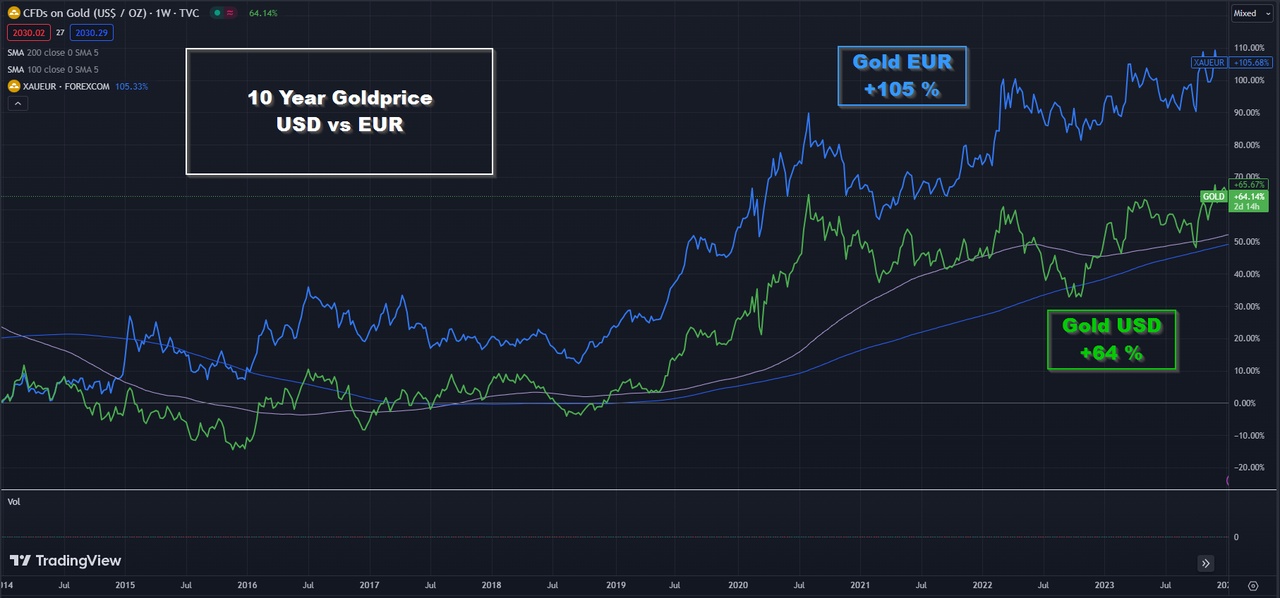

What does this mean in practice? If the USD depreciates against the euro, all assets priced in USD become cheaper. This can be seen particularly well in the price of gold. The USD has done quite well against the EUR over the last 10 years, which is why the

US gold investor only 64 %,

but the EU gold investor made a 105% return. [4]

The same is true for equity returns, US equities have a higher return for foreign currency investors when the dollar is strong and vice versa.

3. company and sector cluster risks

It should also be noted that the

S&P - 500 - has a 37% Information Technology share and the

Nasdaq-100 - 45%.

At the same time, the top 10 positions in the

S&P - 500 - 31.5% and in the

Nasdaq-100 - 45.5%.

The fact that the top positions are in the same sector or at least have significant exposure to it leads to a cluster risk that should not be underestimated. (which does not mean that this has to materialize)

4. correlation of financial markets

It is often pointed out that the stock markets are so strongly correlated as a result of globalization that diversification is becoming less and less important. However, without realizing it, this also implies that the Markowitz model, which forms the basis of modern portfolio theory, is outdated. (https://en.wikipedia.org/wiki/Markowitz_model)

However, the financial community disagrees.

In their 2018 paper "Global Portfolio Diversification for Long-Horizon Investors" [5], the authors Luis M. Viceira & Zixuan (Kevin) Wang documented a significant increase in cross-country return correlations of global equity and bond markets in the period 1986-2016, especially since the turn of the millennium. The main cause of the increase in global return correlations has been financial globalization, which has caused discount rate shocks in markets to become significantly more correlated in the SHORT TERM.

However, LONG-TERM global equity portfolio risk has not increased, optimal long-term portfolios are just as globally diversified and invested in equities as in the previous period, and the expected benefit of long-term investors from holding global equity portfolios has, if anything, increased.

5. summary

The USA belongs in every portfolio! Europe, Japan too! And yes, also the emerging markets and small caps.

However, an MSCI World already has 67% US exposure and a FTSE All-World 58%. You can think about reducing this proportion by buying the other regions. This should reduce the risk and increase the expected value in the long term. [5]

However, many people seem to believe that the last 15 years are more predictive of the future than the last 30, 50 or 100 years. This cognitive bias is also known as recency bias (https://en.wikipedia.org/wiki/Recency_bias) and repeatedly leads to mistakes, especially when investing.

The historically better equity returns in the USA can only be explained to a limited extent by higher earnings growth. [1] Part of the past returns (approx. 2% p.a.) has flowed into the valuation of companies. (the price has risen more than the value)

If the exact same company existed three times, in Germany, Austria and the USA, then the US company would be almost 2X as expensive as the German company and 3.5X as expensive as the Austrian company. http://worldperatio.com/

*(this is a very simplified comparison, as the sector weighting of the countries is not the same, and US tech in particular is historically expensive and has the highest weighting)

The premium described above results in a realistic scenario in which the US underperforms the market without the need for real economic factors. A simple change of sentiment would be enough; the information technology sector, which is particularly highly valued with a P/E ratio of 34.4 and which now accounts for 37% of the index, would be particularly affected.

How do the reasons given in the foreword for overweighting US equities hold up?

- The other countries are just performance chasers

A large part of the outperformance is due to the fact that companies have become more expensive. (Price has risen faster than value) There is no systematic explanation as to why this should continue in the future. High valuations tend to indicate lower returns in the long term. [1],[2], [3]

- Nothing works without the USA (markets are increasingly correlated)

This only applies to short time periods; in the long term, country diversification is just as important as in the past. [5]

- US companies earn their money worldwide (and are therefore automatically diversified)

Regulatory and currency risks are almost impossible to diversify away with US equities. [5], [4]

I hope I was able to give you food for thought...

Sources:

[1] The Long Run Is Lying to You

https://www.aqr.com/Insights/Perspectives/The-Long-Run-Is-Lying-to-You

[2] Accounting valuation, market expectation, and cross-sectional stock returns

https://www.sciencedirect.com/science/article/pii/S0165410198000263

[3] Is The United States A Lucky Survivor: A Hierarchical Bayesian Approach

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3689958

[4] TradingView chart as image file attached (please don't hit me, my TradingView skills are not the best 😅)

[5] Global Portfolio Diversification for Long-Horizon Investors

https://www.nber.org/papers/w24646

https://www.nber.org/system/files/working_papers/w24646/w24646.pdf

"The problem with the world is that the intelligent people are full of doubts while the stupid one are full of confidence." - Charles Bukowski