Preface:

It could be so easy after all, you take your hard inherited money and put it into a stable growing economy and BOOOOM!!!! Excess returns!!!

So all-in Guyana, Macau, Fiji, Mozambique and Afghanistan?

NO? Why not? Too hardcore? ...

All right, then India, China, Brazil, Mexico, Indonesia?

I can already tell that some people here have started to prick up their ears...

But Daddy knows what you want, you wanted the fast-growing developed markets:

USA, Norway, Israel ... don't think I haven't noticed you all diligently buying the

MSCI Norway ETF $ENOR and MSCI Israel $EIS diligently. It is even rumored that there are people who save the NADDAQ 100 $QQQ but I personally think that's a rumor 😉.

But joking aside, what does economic growth mean for shareholders, does it increase the expected return?

Unfortunately, the data is somewhat sobering. In the next article, I would like to show you why you can and should ignore economic data as a long-term investor.

Have fun.

1. the economy is not the stock market. The stock market is not the economy.

The economy:

describes the complex interplay of economic activities. It comprises various participants:

Companies, produce goods and services.

Households, individuals and families demand these and act as employees.

States and government authorities set the economic framework conditions.

The stock market:

Is a pricing mechanism that converts future profit expectations into today's prices.

The market efficiency hypothesis (https://de.wikipedia.org/wiki/Markteffizienzhypothese) is taken as a basis. All existing economic data and expected future economic data are already included in the price. In order to generate an excess return from this level, future economic data must be better than assumed. The higher the optimism, the less likely it is that expectations will be exceeded.

In the Fama-French five-factor model (https://en.wikipedia.org/wiki/Fama%E2%80%93French_three-factor_model), "growth" does not appear as a factor. This means that growth stocks have not generated excess returns over long periods of time. The simplest explanation for this is that in the past investors were systematically prepared to pay too much for growth and / or growth did not materialize to the extent calculated.

2. GDP growth <?> Share returns

In a 2010 MSCI research paper "Is There a Link between GDP Growth and Equity Returns?" [1] found no link between GDP growth and equity returns. It is argued that in today's integrated world you have to look globally rather than locally. But even globally, no correlation could be found.

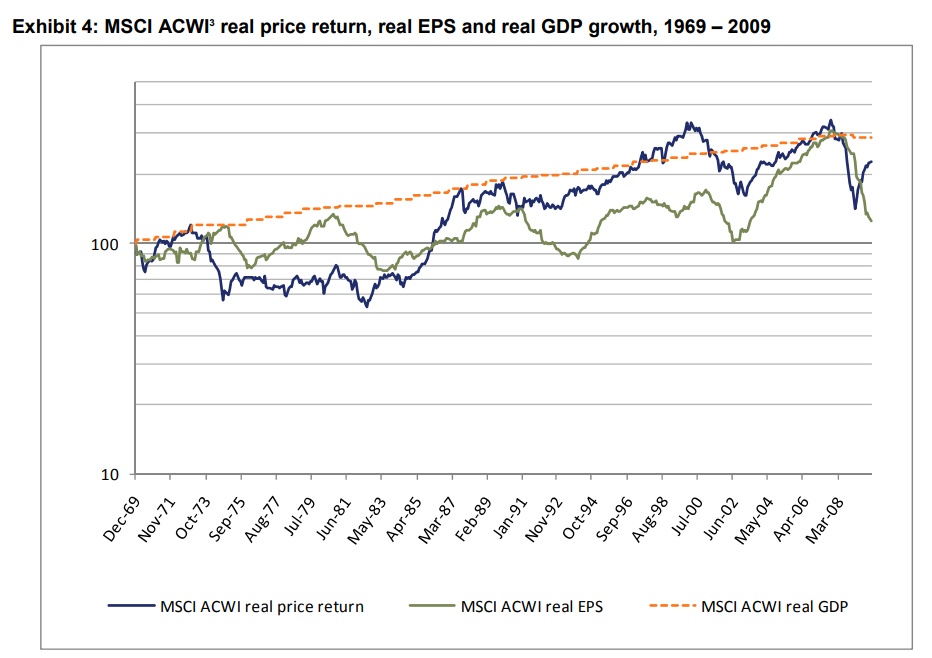

As can be seen in graph [1.1] (Appendix), stock prices (blue line) correlate with earnings per share (green line), even if the correlation is not perfect, it is still much stronger than the correlation of stock prices (blue line) with real GDP growth (orange line).

The reason for this is EPS dilution. When a market grows, at some point it becomes so attractive that new companies turn to this market. The pie gets bigger, but more and more companies want to eat it. It is bad for shareholders if new companies are founded that compete with their own investments. The available capital has to be spread across more and more companies.

William J. Bernstein & Robert D. Arnott came to the same conclusion in their paper "Earnings Growth: The Two Percent Dilution". [2]

3. real per capita GDP growth

Jay R. Ritter examined in his 2012 paper "Is Economic Growth Good for Investors?" [3], Jay R. Ritter examined the relationship between inflation-adjusted per capita GDP growth and equity returns in developed countries and emerging markets from 1900 to 2011.

The surprising result is the same for both. Over long periods of time, stock returns correlate negatively with per capita GDP growth.

It looks as if employees and consumers are the main beneficiaries. A shareholder gains nothing from full employment. Lower prices for the end consumer due to increased productivity do not increase shareholder value.

Companies are facing ever-increasing competition. There is a pressure to innovate and invest in order not to fall behind. This puts pressure on profits.

Note:

Correlated negative does not mean that share prices fall when per capita GDP growth is high, but returns tend to be lower.

Summary:

Economic growth is not a prerequisite for share returns. What primarily interests a shareholder is earnings per share. Earnings growth can be achieved through a variety of measures, sales growth is just one of them.

In the past, investors have tended to overpay for future growth. There is no reason to believe that this has changed.

If expectations are too high, even good economic data can disappoint.

It is largely irrelevant whether there is good or bad news, what is relevant for share prices is whether it comes BETTER or WORSE than expected.

In the long term, share prices correlate with EPS.

In growing economies, new companies are constantly entering the market. This creates increasing competitive pressure. Consumers and employees, not investors, are the main beneficiaries of this brutal cut-throat competition, which is seen as the driver of innovation in capitalism.

I have also tried to find the opposite, but have not come across anything reliable.

Has anyone found publications that have come to different conclusions? Then let me know!

Sources:

[1] Is There a Link between GDP Growth and Equity Returns? - MSCI Barra Research Paper No. 2010-18

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1707483

https://www.msci.com/documents/10199/a134c5d5-dca0-420d-875d-06adb948f578

[1.1] Appendix 1 - Exhibit 4: MSCI ACWI3 real price return, real EPS and real GDP growth, 1969 - 2009

[2] Earnings Growth: The Two Percent Dilution - William J. Bernstein & Robert D. Arnott

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=489602

[3] Is Economic Growth Good for Investors? - Jay R. Ritter 2012

https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1745-6622.2012.00385.x

https://www.evidenceinvestor.com/evidence/is-economic-growth-good-for-investors/

"All the problems of mankind stem from man's inability to sit still alone in a room."

-Blaise Pascal