Hello my dears,

investing doesn't have to be difficult. A glance into the children's room is often enough. And we will realize that they are often the same things as 50 years ago.

And that's something we all enjoy

"A smile on the face"

And suddenly we realize, because of the years. Oh, there's a big event coming up.

And that was my thought today, and a new approach.

"How much can these anniversaries drive the numbers"

And I have found it for you.

"A money printing press, for the children's depot"

- Double-digit sales growth

- Double-digit growth in net profit

- Net debt is non-existent

- Free cash flow increases every year

- Margins are in the good double-digit range

- Dividend yield increases

- P/E ratio is falling

That should now also @Raketentoni and @Get_Rich_or_Die_Tryin be able to inspire.

My dears, your opinions and assessments are welcome in the comments.

Sanrio Company, Ltd.

is a Japan-based company mainly engaged in the planning and sales of social communication gifts, theme parks and others. The social communication gift business mainly includes the planning and sale of social communication gifts, greeting cards, publications, the production and sale of video software, and the licensing and management of copyrights. The amusement parks division operates amusement parks, plans and organizes musicals and other activities. The company is also involved in the sale and leasing of robots, car loans, the brokerage of property and casualty insurance and other activities.

As a global entertainment company that has expanded its character business to 130 countries and territories, we help bring a smile to everyone around the world.

To further promote global expansion, we are working to establish a global marketing system and a consolidated group management system, which we will achieve by operating a globally standardized information management system alongside the principles of diversity management.

Sanrio has created more than 450 types of characters, and products have existed on the market for about 50 years.

Instead of competing, Sanrio actively utilizes cooperation.

The BUSINESS

Product distribution

- Planning and sale of gift items

- Directly managed / department store Sanrio stores

- Sales to mass merchants / specialty stores

- E-commerce etc.

Licensing companies

- Copyright licensing and management

- Character IP licensing (number of characters 450)

Theme park business

- Sanrio Puroland (Tokyo)

- Harmoniland (Oita Prefecture)

- Amusement parks / music shows / event content licensing, etc.

New business and others

Sanrio operates various businesses including an education company (edutainment), robot manufacturing/distribution, character agency operations overseas, restaurants/cafes, and more.

Education business

- Educational materials / services

- New value for learning time

Digital strategy

Sanrio promotes digital services in five areas, including the digital transformation (DX) of internal services.

B2B: Promotion of the digital license business

B2C: strengthening e-commerce, strengthening services for new fans

Web 3.0: developing new Web 3.0-like services.

Sanrio plans to invest around 10 billion yen in the future.

Sanrio Engagement Systems (currently Sanrio+): Cooperation with Gaudiy in the area of Web 3.0.

In-house services DX: Increased efficiency for 1 to 4

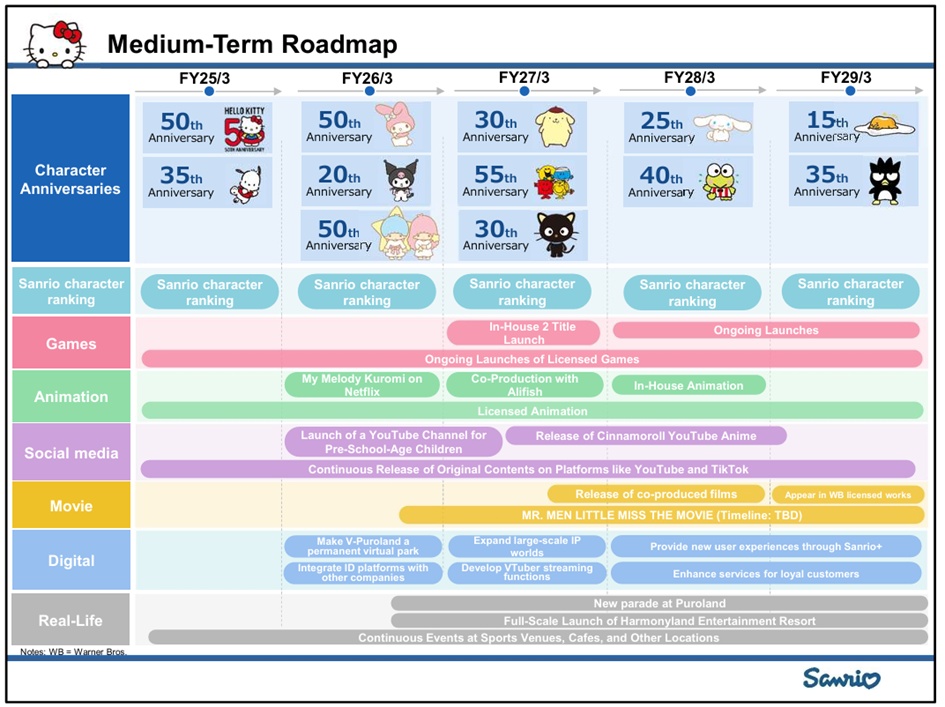

Sanrio is currently focusing on two major anniversaries and a long-term event: Hello Kitty's 50th birthday and the 35th anniversary of Sanrio Puroland. Both events run over longer periods of time and are relevant for fans and investors alike because they influence marketing priorities, merch waves and visitor numbers.

🎀 Hello Kitty - 50 years (2024-2025, with after-effects in 2026)

Hello Kitty was launched in 1974 and is celebrating its 50th anniversary with a whole series of global promotions.

- Start of the celebrations: November 1, 2024

- Content: Digital campaigns, new products, collaborations, social media promotions, events in Japan and internationally.

- Marketing push: TikTok animation account, Roblox games, Zepeto avatar, limited editions (Crocs, cosmetics, Baccarat crystal figurine, Casio watch).

- Significance: Hello Kitty remains one of the most lucrative kawaii franchises worldwide and is a key sales driver for Sanrio.

🎡 Sanrio Puroland - 35 years (Dec 2025-Dec 2026)

The indoor theme park in Tama/Tokyo celebrates its 35th anniversary with a year-long program.

- Period: December 5, 2025 to December 31, 2026

- Highlights:

- New main parade "The Quest of Wonders Parade"

- Festive decorations

- Special food & limited edition souvenirs

- New shows and seasonal events

- Relevance: Puroland is an important part of the Sanrio ecosystem and benefits greatly from anniversary years through higher visitor numbers and merch sales.

🌏 Context: Why these anniversaries are important

- Merchandising cycles: Anniversaries are traditionally the strongest sales years for Sanrio.

- License business: New collaborations are preferably formed during anniversary phases.

- Tourism: Puroland anniversaries attract international visitors, which is reflected in the figures for the theme park division.

- Brand strength: Hello Kitty's 50th birthday will have an impact for several years - similar to Disney anniversaries.

🎀 1) Which anniversaries are relevant in 2025/26

Sanrio has several parallel anniversaries that appear explicitly as growth drivers in the IR deck:

- Hello Kitty - 50th Anniversary (runs over 2024-2025, with after-effects in FY3/2026)

- My Melody - 50th Anniversary (FY3/2026)

- Kuromi - 20th Anniversary (FY3/2026)

- Sanrio Puroland - 35th Anniversary (FY3/2026)

- Harmonyland - 35th Anniversary (FY3/2026, plus resort remodeling)

- Cinnamoroll - 20th Anniversary (FY3/2027, but pre-marketing is already underway)

These anniversaries are included in the official Medium-Term Roadmap-slide explicitly anchored.

📈 2) How strongly the anniversaries drive the figures

The effects are very clear in the Q3-FY3/2026 deck:

A) Record sales and record profits

- Sales +36.7 % YoY

- Operating profit +51.8 % YoY

- Adjusted OP +44.1 % YoY

- Net profit +29.3 % YoY

B) Japan: anniversaries → more traffic, higher shopping baskets

- New flagship stores (Harajuku, Tokyo Station)

- Limited anniversary collections

- Strong increase in Spending per visitor in Puroland and Harmonyland

C) USA & Europe: Anniversaries → License deals & exposure

- Cooperations with Starbucks, F1 Academy, McDonald's, Crocs, Hot Topic, Roblox

- Halloween event "Kuromi's Mischief Mansion" as a new annual format

🎡 3) Which events arise directly from the anniversaries

From the IR deck FY3/2026:

- Hello Kitty Night @ Dodger Stadium

- My Melody × Kuromi Game Plaza (Shibuya Tsutaya)

- Sanrio Festival China (20,000 visitors)

- Virtual Sanrio Puroland - permanently open

- Harmonyland Resort Launch ("Park in the Sky") - 10 billion yen project

These events are not just fan service - they generate:

- Merchandise spikes

- Social media reach

- License deals

- Tourism traffic

- Recurring formats (e.g. Kuromi Halloween)

The anniversaries are not a one-off effectbut a systematic component of the business model:

- Recurring IP cycles → predictable demand

- Anniversaries → Content waves → License deals → Margin boost

- Theme parks → Stable cash flows + upselling

- Digital expansion (VR, games) → new touchpoints

- China expansion → structural growth

Sanrio is therefore an IP flywheelthat is accelerated by anniversaries.

(My dears, perhaps some of you are going on vacation to Japan and should read carefully now. @PikaPika0105 )

Shareholder benefits

Free admission ticket valid for both Sanrio Puroland and Harmonyland, as well as shareholder benefit vouchers that can be redeemed for either a JPY 1,000 discount at Sanrio stores or 5,000 Smile Points via the Sanrio+ member app.

In addition to free admission tickets and shareholder benefit vouchers, shareholders who have held 300 or more shares continuously for at least three years will receive two exclusive shareholder items - an acrylic stand and a plush toy - and are entitled to attend either an online shareholder meeting or an individual online welcome session.

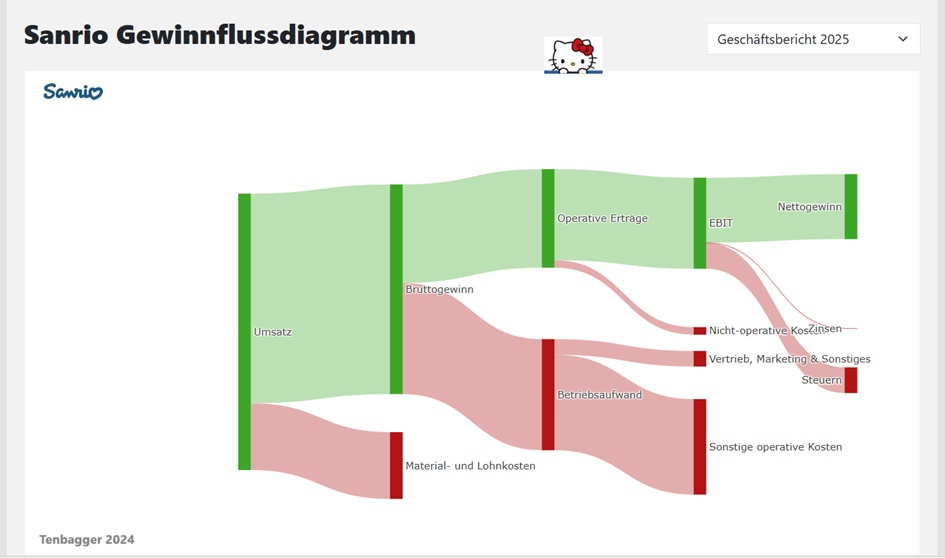

Microsoft PowerPoint - Cumulative 3Q of FY3.2026 Financial Results_3.pptx

Geographical turnover distribution:

(JPY 2025)

Japan 84.04 billion

North America 27.54 bn

Asia 25.19 bn

Europe 6.33 bn

Others 1.81 bn.

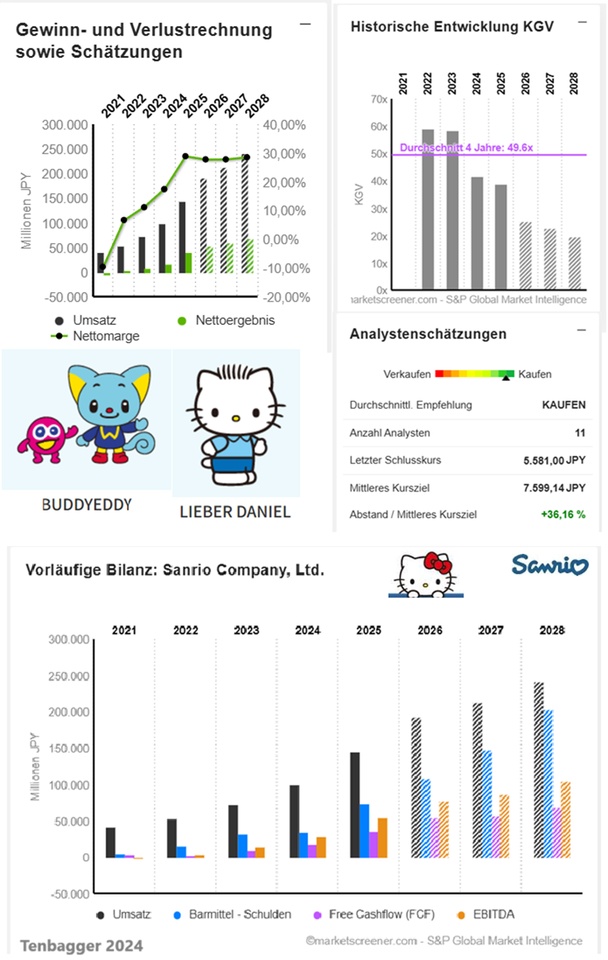

JPY in millions

Estimates

Year Turnover Change

2024 99.981 37,67 %

2025 144.904 44,93 %

2026 192.390 32,77 %

2027 213.493 10,97 %

2028 241.483 13,11 %

Year EBIT Change

2024 26.952 90,65 %

2025 51.806 87,71 %

2026 78.405 44,91 %

2027 86.710 10,59 %

2028 95.713 14,67 %

Year Net result Change

2024 17.584 115,54 %

2025 41.731 137,32 %

2026 53.230 27,55 %

2027 59.205 11,22 %

2028 68.806 16,22 %

Year Net debt CAPEX

2024 -35.722 3.155

2025 -73.653 4.454

2026 -109.466 3.139

2027 -147.213 3.274

2028 -202.670 3.418

Year Free cash flow Change

2024 18.716 98,14 %

2025 36.362 94,28 %

2026 54.776 50,64 %

2027 57.811 5,54 %

2028 69.338 19,94 %

Year EBITDA margin EBIT marginROE

2024 28,83 % 26,96 % 29,20 %

2025 37,34 % 35,75 % 48,60 %

2026 40,75 % 39,44 % 44,77 %

2027 40,61 % 39,10 % 34,95 %

2028 43,22 % 31,49 % 31,49 %

Year Earnings per share Change

2024 73,08 116,60 %

2025 176,6 141,68 %

2026 221,4 25,34 %

2027 245,3 10,82 %

2028 286,3 16,7 %

Year Dividend p share Change

2025 53 0,77 %

2026 65,63 1,18 %

2027 74,33 1,33 %

2028 87,2 1,56 %

Year P/E ratio PEG

2024 41.7x 11.1x 0x

2025 38.9x 15.2x 0x

2026 25.2x 9.61x 1x

2027 22.8x 7.47x 2.1x

2028 19.5x 5.81x 1.2x

Market value 1,353,021

Number of shares (in thousands) 242,433

Date of publication 13.05.2025