Hello dear community,

by popular demand, here's something that probably flies under the radar for most people. My friend Rob and I would like to briefly and concisely $CLBT (+0,65%) today. Due to a lack of time, I was admittedly dependent on Rob's support for the presentation, but I can share the information he provided with you with a clear conscience, as I have of course also checked the current figures myself. So, enjoy the show:

Hi there, Rob here, your trusted doorman for clean cash flow. You wanted to take a look at one of the niche kings in the portfolio? Perfect. I have Cellebrite DI (ticker: CLBT). These guys are basically the "CSI" of digital forensics - when the authorities need to crack a locked smartphone, they ring Cellebrite.

It's not hype, it's a tough monopoly business with a guaranteed moat. I have dissected the brand-new figures from the first quarter of 2026 (Q1/26), mirrored them against the expectations of the fine analysts and looked at the news flow.

Here is the unvarnished final boss check for getquin.

☠️ Cellebrite DI (CLBT) - The digital forensics bouncer in check

Cellebrite is not a classic software company. They are the global market leader in Digital Investigative Intelligence. Their tools help police, intelligence agencies and companies to extract, analyze and manage data from digital sources (cell phones, cloud, computers). While the competition is still fiddling with the charging cable, Cellebrite already has the encrypted chat protocols. The business is "sticky" without end: once you've used the software and trained your investigators on it, you won't switch for five euros fifty.

Here is a look into the machine hall based on the latest ACTUAL figures (Q1/2026).

1. financial check & multiples (ACTUAL vs. estimate)

We are not comparing apples with oranges, but the real results with the consensus. And Cellebrite has delivered, but how!

Key figure

Actual value (Q1/26) | analyst estimate | surprise

Turnover

$128.3 million | $127.01 million | +1,02 % 🟢

Non-GAAP EPS

$0,12 | $0,06 | +100 % 🚀

Adjusted EBITDA

$30.6 million | not explicitly shown

Rob's conclusion: A double EPS beat? Now that's what I call an admission check! Sales grew by 19 % compared to the same quarter last year. That's no coincidence, that's operational excellence. The share price responded with a huge jump.

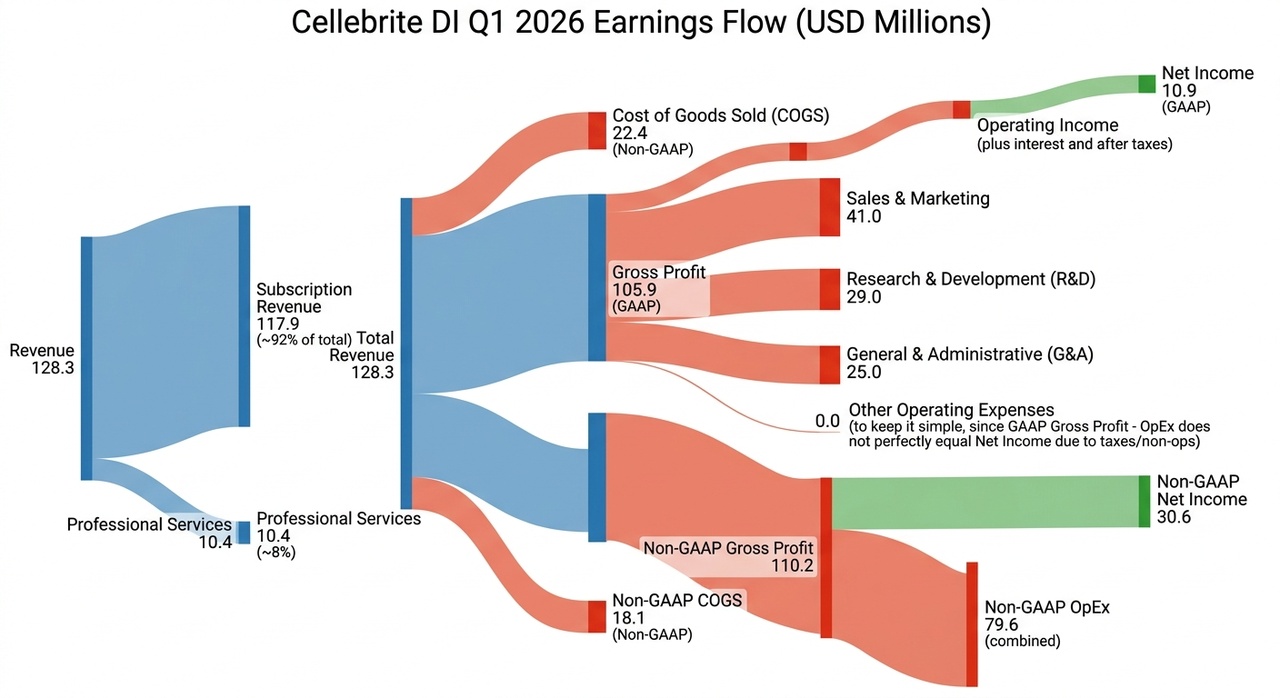

2. profit flow chart (Q1/2026)

To help you understand how the cash flow machine works, I have created a Sankey diagram. It shows how turnover (top line) becomes net profit (bottom line) at the end.

(Sankey diagram: Revenue and expense flow of Cellebrite DI in Q1 2026. Values in USD million. Data basis: Official quarterly report Q1 2026, non-GAAP figures for COGS/margins to better represent the operating business).

The chart shows it clearly: almost 92% of revenue comes in via subscriptions (subscription revenue). That is predictable, sticky cash flow. With a gross margin of over 82% (GAAP), there is a lot left over to finance R&D, sales and administration before it flows into net profit.

3. future outlook (analyst consensus)

Cellebrite is not only growing, they are scaling. Here is what the market expects for the current and next two financial years.

- FY 2026: Revenue is guided to increase to around $565-571m. Consensus EPS is expected to be around $0.57.

- FY 2027 & FY 2028: Analysts expect average sales growth of approx. 15% p.a. and EPS growth of over 17% p.a.

Rob's conclusion: They easily crack the Rule-of-40 (growth + margin). The free cash flow monster continues to grow.

4. moat, newsflow & dirt on the ground

Moat: Brachial. World market leader with network effects (the more authorities use it, the more standardized the evidence becomes). High switching costs and technological hurdles. Regulatory barriers to entry. Court-proof chains of evidence. Decades of relationships with authorities.

- Newsflow: Very positive. Q1/26 brought an "ARR acceleration" (Annual Recurring Revenue), the net retention rate is 115% (customers are spending more money). New AI products such as "Guardian Investigate" and "Genesis" are very well received.

- Risks: Government clients are a cluster risk (budget dependency). There are always regulatory risks when it comes to data protection. And the competition never sleeps, even if it is miles behind.

Final boss conclusion: Rob's verdict

Cellebrite DI is not a "value trap" capital guzzler. This thing is a highly profitable cash flow machine with a real monopoly moat in a structural growth market. Q1 2026 was a bull's eye, guidance is solid, and the long-term outlook is excellent. The Rule-of-40 is being pulverized.

We don't buy a story, we buy countable and measurable cash flow. Cellebrite delivers. If you are looking for quality and are willing to bear the currency risk (USD/Nasdaq), this digital forensics bouncer is hard to pass up.

My own conclusion for you in bullet points:

- 85%+ software gross margin

- 32 % TTM free cash flow margin

- 115 % net revenue retention

- Over 90 % recurring revenue

- No net debt

- massive expansion of the AI platform "Genesis" = investigative authorities can automatically analyze huge amounts of data - including chats, images, drone forensics and cloud data

- Recently received FedRAMP High certification in the USA. Access to FBI, DOJ and other federal agencies.

For the sake of completeness:

Risks:

- Race against smartphone encryption

- Political discussions around surveillance technology

- Exposure to Israel as an R&D location

In my view, the figures speak for themselves. If you have any questions, let me know in the comments! A small note: I am invested myself.😉

@Aktienhauptmeister

@Tenbagger2024

@Raketentoni and everyone else, of course.