Hello, everyone,

Energy and electricity will remain a major topic. When it comes to renewable energy, some investors are often a bit skeptical. But even this form of energy is gaining more and more acceptance.

That’s why I’d like to introduce you to a company in this sector today.

Since I know that our dear @Dividendenopi has been deeply involved with this topic. After all, he was invested in $EKT (+1,25%) invested for a long time. Naturally, I’m particularly interested in his opinion.

But of course, I’m just as interested in your opinions.

SOLV began delivering some of the earliest large-scale solar power plants in the U.S. in 2008. As the projects grew, so did the company’s capabilities—from engineering, procurement, and construction to commissioning, operation, and maintenance. Today, they are a full-lifecycle provider capable of designing, building, operating, and optimizing complex facilities, including high-voltage substations, transmission interconnections, and end-to-end SCADA/network systems. SOLV is known for its leadership in utility-scale solar and battery storage, for bankable execution, and for long-term performance.

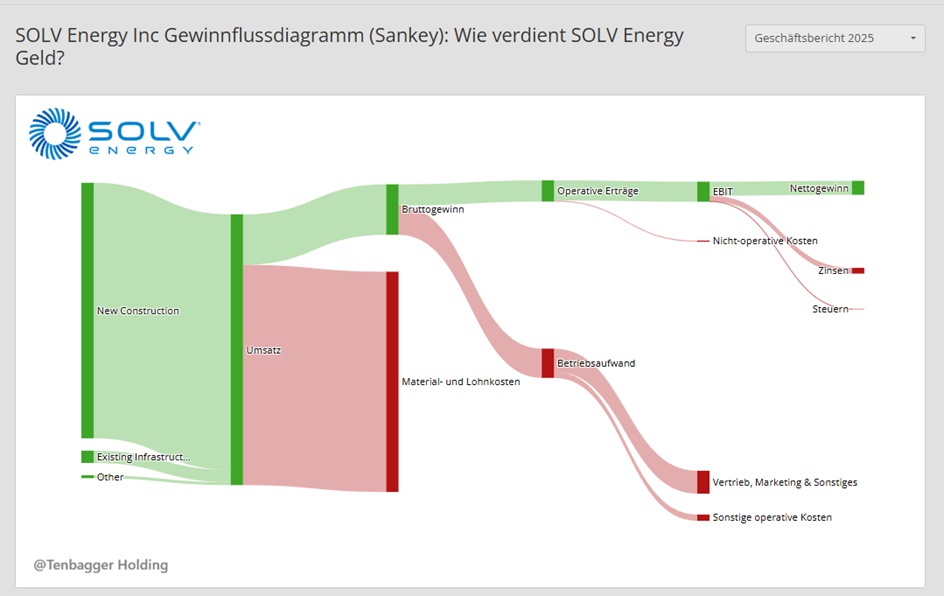

SOLV is a leading provider of infrastructure services for the energy sector, including engineering, procurement, construction, testing, commissioning, operation, maintenance, and retrofitting. Since its founding in 2008, the company has built more than 500 power plants with a generation capacity of 21 GWdc and currently provides O&M services under long-term contracts for 150 power plants with over 20 GWdc of generation capacity.

Demand for electricity is accelerating as data centers grow and U.S. manufacturing recovers. SOLV Energy delivers the large-scale solar and battery storage projects that power these industries on time and at scale. With proven expertise, extensive resources, and full lifecycle capabilities, they build power plants that deliver long-term performance and added value for customers and communities.

2,600 employees, including nearly 1,950 skilled tradespeople.

SOLV boasts:

- 500+ completed projects

- 20+ GW under management

- EPC + O&M customers in 48 U.S. states

- Backlog: $8.0 billion (EPC + O&M)

- 150+ active projects

046aaf8c-2921-4257-9c68-7ea176174113

The presentation explicitly states:

“Accelerating investment in data centers … is driving unprecedented load growth”

“The fastest-growing loads require carbon-free power”

This means:

✔ Data centers are a key driver of demand

- Hyperscalers (AWS, Google, Microsoft, Meta)

- AI data centers

- Colocation providers

These companies require enormous amounts of renewable energy, often through PPA structures.

✔ SOLV benefits directly from EPC projects

Data centers do not build solar plants themselves—they enter into PPAs with developers. These developers then contract EPC players like SOLV.

✔ SOLV clearly positions itself as a “data center enabler”

The presentation shows:

- 5× higher load growth driven by data centers

- Solar + BESS as the preferred solution for data centers

- SOLV as #2 EPC and #2 BESS contractor in the U.S.

→ This is a direct strategic focus on the data center boom.

🧠 3) Juan’s Conclusion (short & clear)

Juan says: SOLV doesn’t name any clients, but the pattern is clear: large utilities, IPPs, and infrastructure investors. The key point: Data centers are now one of the strongest drivers of demand, and SOLV, as an #2 EPC + #2 BESS contractor, is perfectly positioned to build precisely these projects.

In short: No names, but clearly data center exposure—and it’s growing.

May 4, 2026

SOLV Energy veröffentlicht die Finanzergebnisse des ersten Quartals 2026 am 12. Mai 2026

May 4, 2026

April 1, 2026

SAN DIEGO, February 12, 2026 (GLOBE NEWSWIRE) – SOLV Energy, Inc. (“SOLV” or the “Company”) (Nasdaq: MWH), a leading provider of infrastructure services to the energy industry, announced today the completion of its public offering of 23,575,000 shares of its Class A common stock, which also included

February 12, 2026

Juan’s Take on SOLV Energy’s Financial Metrics for 2025–2028

(short, concise, investor-focused)

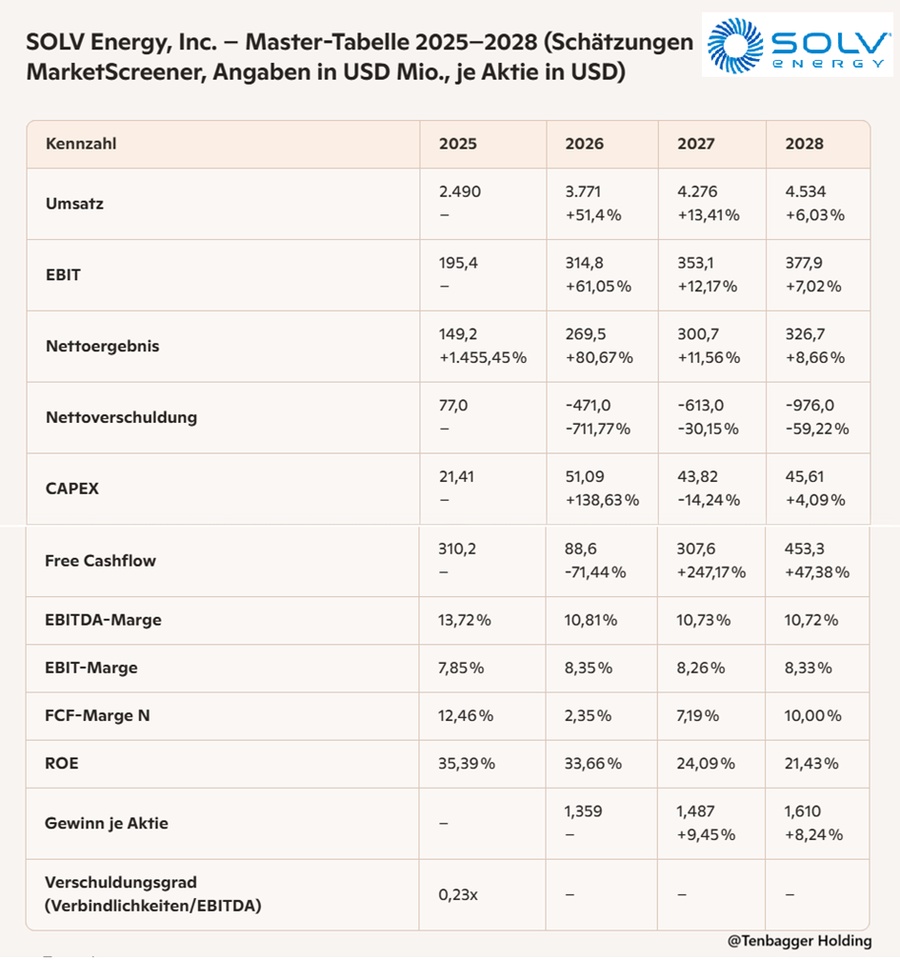

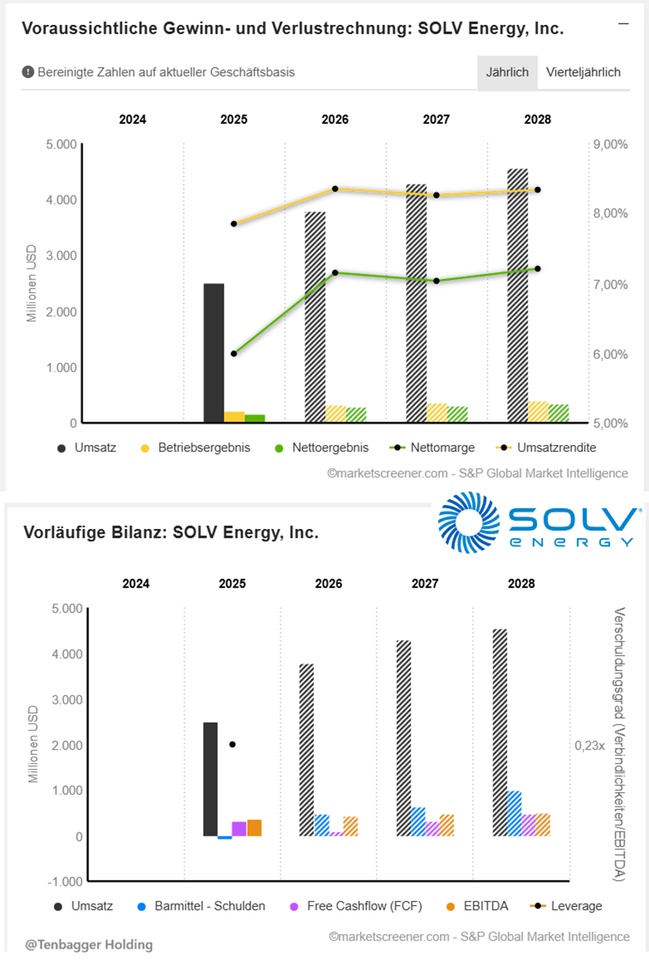

Juan says: SOLV Energy delivers a strong growth profile, but with significant fluctuations in cash flow. Revenue and EBIT are rising steadily, while margins remain stable in the single-digit range. Free cash flow fluctuates sharply—first rising, then plummeting, then rebounding strongly—which is typical for project-heavy solar and EPC businesses.

The net debt turns deeply negative starting in 2026, which is a clear balance sheet advantage. EPS is growing at a solid double-digit rate, but overall profitability remains modest.

In short: Top-notch growth, strong balance sheet, volatile cash flow—a solar pure play with momentum but a cyclical pulse.

Market value 4,853

Number of shares (in thousands) 115,349

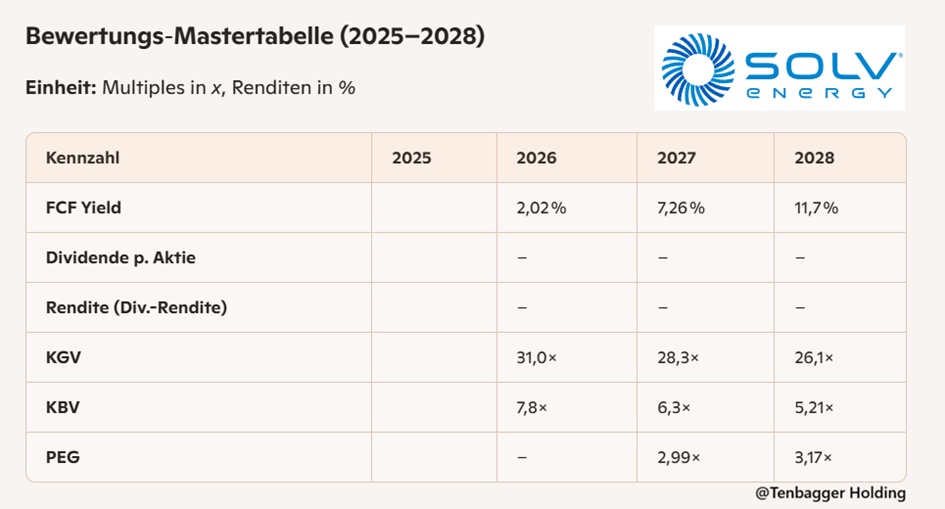

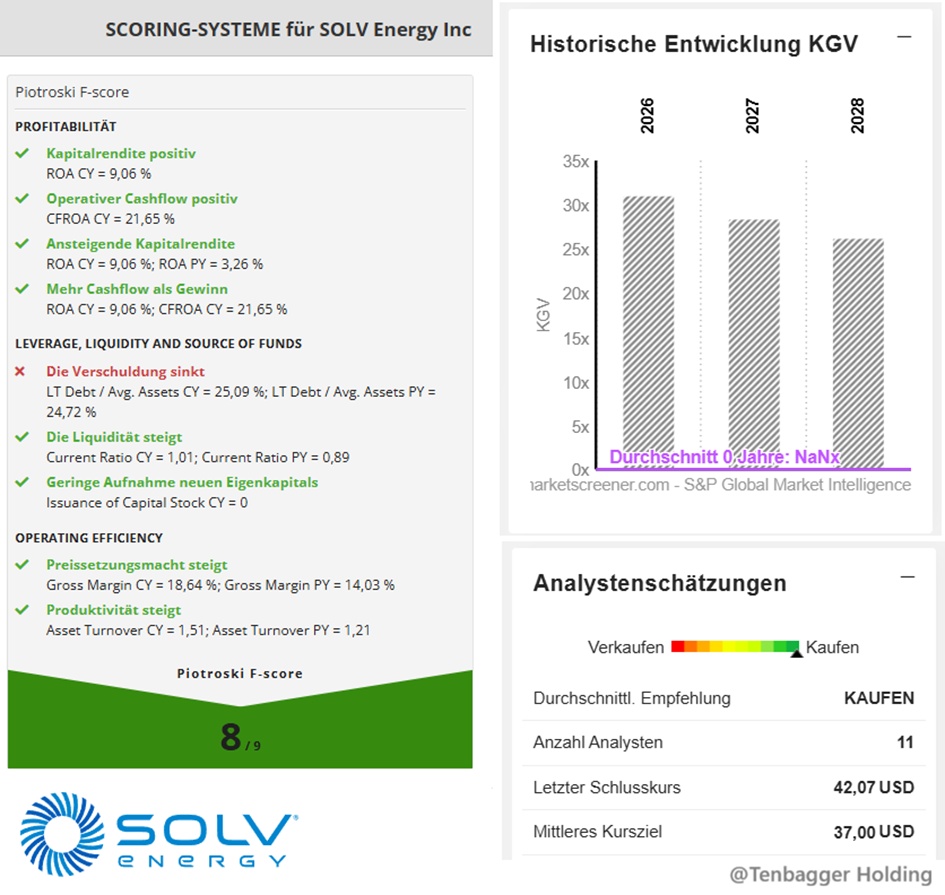

Juan’s Conclusion on the 2026–2028 Valuation Metrics

(short, precise, investor-focused)

Juan says: SOLV Energy looks like a typical high-growth stock that is just beginning to see its valuation normalize. The P/E ratio is falling steadily from 31× to 26×, while the P/B ratio is falling from 7.8× to 5.2× —a clear indication that the market is increasingly pricing in the company’s growth.

The FCF yield rises sharply from 2% to nearly 12%, which makes the stock significantly more attractive from a fundamental perspective. The PEG above 3 shows, however, that while growth is strong, it is no longer “cheap.”

In short: Valuation is easing, cash flow attractiveness is rising, but the stock remains a growth play with premium potential.

Performance

1 week +5.60%

1 month +48.55%

June 17, 2026, 10:00:00 PM •

Nasdaq (USD)

34.69 USD

June 18, 2026, 1:31:06 PM •

Société Générale (EUR)

29.80 EUR

$mwh