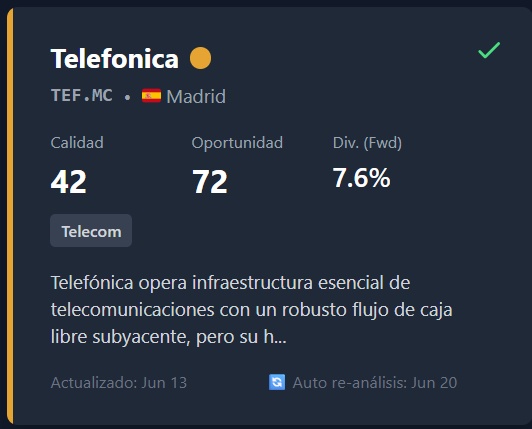

I’ve been invested in Telefónica for as long as I can remember. It’s always been undervalued.

However, my system now places it in the CAUTION quadrant. Why?

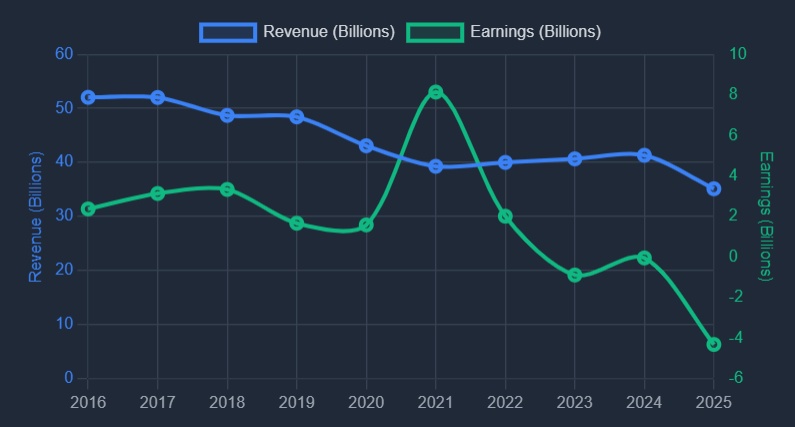

- It detects a persistent structural contraction in long-term revenue, reflected in a -4% CAGR over the last 10 years, while the core business requires high and ongoing capital investments for the rollout of 5G and fiber

(data from EODHD, chart from DividendQuad)

- Several dividend cuts over the past 10 years, including a 50% cut this year

- A recent amendment to the Spain-Brazil double taxation treaty closes a long-standing tax loophole, resulting in a structural and permanent tax increase on profits