Hello my dears,

Today we are introducing you to a company by the numbers.

Many people say that buying before the numbers is a bit like playing the lottery.

That's why today we're looking at a company that has performed well.

Do you think now is a good time to buy after the figures?

05,05,2026

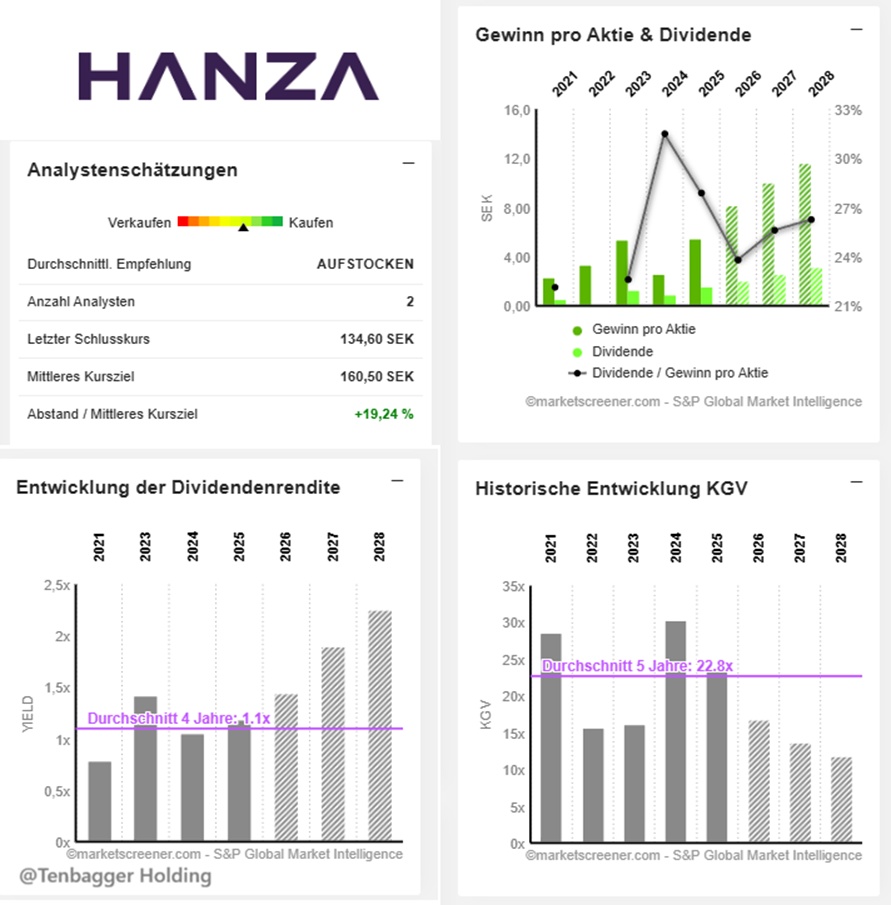

🧾 Brief summary Q1 report HANZA AB

- Profit: SEK 128 million (previous year: SEK 40 million) → +220 % increase

- EPS: SEK 2.08 per share (previous year: SEK 0.90) → adjusted: SEK 2.15

- Sales: SEK 2.646 billion (previous year: SEK 1.326 billion) → +99,5 % Growth

💬 Juan's conclusion

"HANZA delivers an explosive Q1 - sales doubled, profit tripled, scaling is going perfectly."

Hanza ABformerly Hanza Holding AB, is a manufacturing company based in Sweden. The company offers its customers a combination of consulting and customized manufacturing solutions in the fields of mechanics and electronics. The company's activities are divided into three business segments: The Main Markets segment, which comprises manufacturing clusters within or close to Hanza's primary geographic customer markets, which include Sweden, Finland, Norway and Germany; The Other Markets segment, which comprises manufacturing clusters outside of Hanza's primary geographic customer markets. It comprises HANZA's production clusters in the Baltic States, Central Europe and China; and the Business Development segment, which mainly comprises Group-wide functions within the parent company as well as Group-wide projects and functions that are not allocated to the other two segments. Hanza AB was founded in 2008 and has branches in Sweden, Finland, Estonia, Poland, the Czech Republic, Germany and China.

Number of employees: 3,431

The factories are strategically located close to each other in so-called production clusters in order to exploit synergies between the different technologies and enable shorter delivery times, less transportation, lower emissions and lower overall costs.

With a total production area of 170,000 square meters - spread across 18 factories in seven countries in Europe and Asia - Hanza offers complete development and manufacturing in the fields of electronics, mechanical processing, sheet metal processing, heavy mechanics, cable harnesses and complex assembly.

HIGHLIGHTS 2025

- FEB: New factory inaugurated in Sweden 8,800 sqm assembly hall in Töcksfors, improved process and efficiency.

- MAR: Acquisition of Leden completed Closed acquisition of Leden, strengthening of mechanics in Finland/Estonia (including 21,000 m² Oulainen)

- MAR: Defense program LYNX launched In response to a new geopolitical situation with a special program targeting the defense industry.

- JUL: Agreement to acquire Milectria, a leading manufacturer of electrical equipment and systems for the defense industry

- OCT: Milectria acquisition completed

- OCT: Agreement to acquire BMK (~1,500 employees; ~ SEK 3.3 billion in annual sales), completion of the HANZA Strategic Plan 2025 and positioning of HANZA among the largest listed contract manufacturers in Europe.

- NOV: New factory in Finland 10,000 m² in Oulainen, Finland to support further capacity expansion.

- DEC: New factory in Sweden Factory expansion in Mechanics Årjäng, Sweden completed

- JAN 2026: BMK acquisition completed

The acquisition of the German company BMK makes HANZA one of the largest listed contract manufacturers in Europe.

- JAN 2026: Supplier of the Year HANZA awarded Supplier of the Year by 3M in competition with over 6,000 suppliers.

- HANZA was voted Saab Supplier of the Year

Outlook HANZA. Annual Report 2025 BMK establishes a new platform in Germany. Structural trends support our direction. The LYNX program (defense and security) is expected to create new market opportunities

Qi 2026

Year-end report 2025

Geographical distribution of sales:

2025 (SEK)

Sweden 2.32 billion

Finland 1.49 billion

Germany 585 million

Other Europe Union 482 m

Norway 280 m

Estonia 237 million

The Rest of Europe 167 million

Poland 164 million

North America 141 million

Elsewhere in The W 90 million

The Czech Republic 70 million

🔧 Juan summary (short & direct)

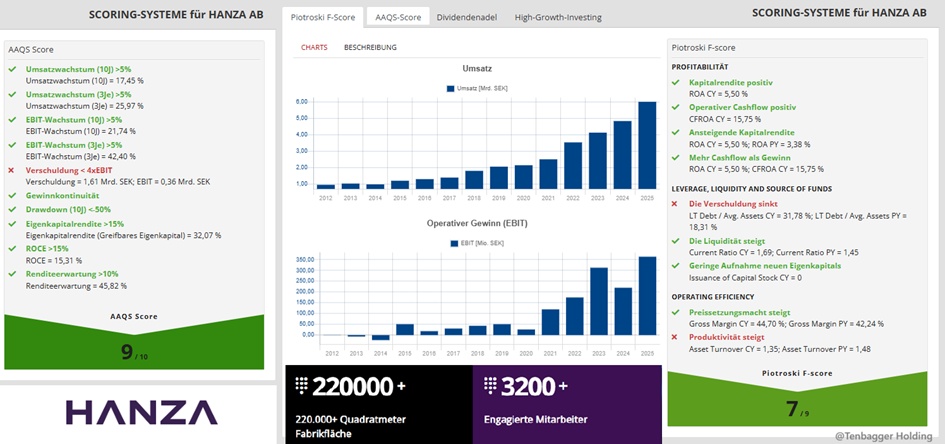

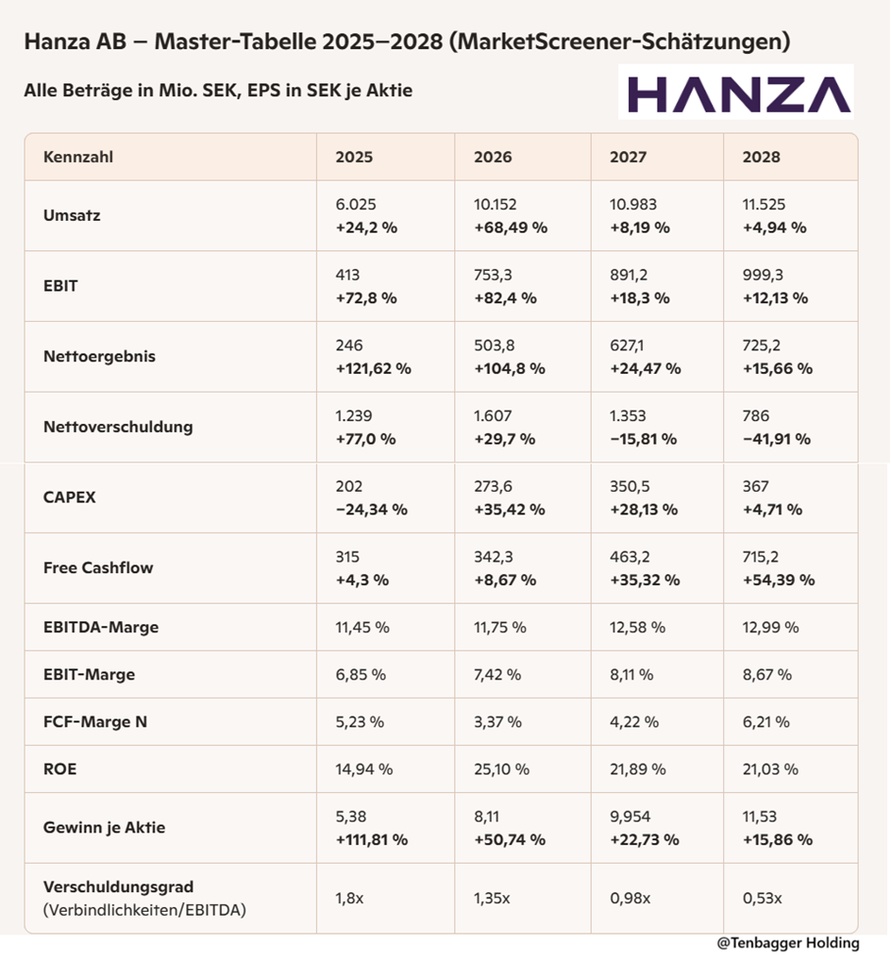

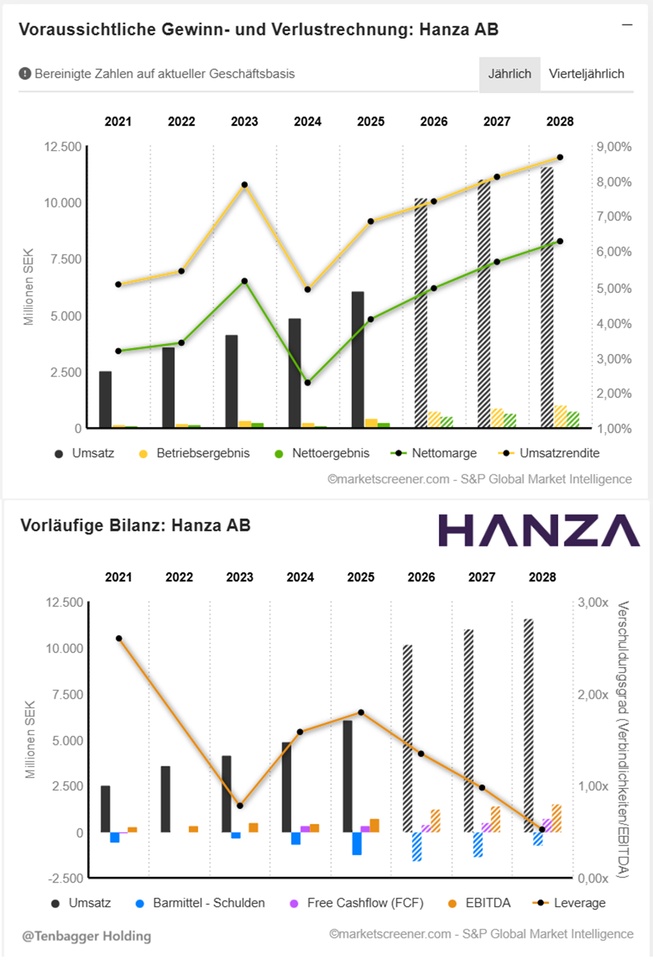

"Hanza delivers picture-book growth: sales high, margins high, cash flow high - and debt is falling like a stone. 2026 is the big leap, 2027-2028 the quality phase. To me, this looks like a clean-scaling industry champion."

"Hanza is growing brutally, improving margins and rapidly reducing debt. This is the kind of industrial compounder the market loves."

Market value: 8,453

Number of shares (in thousands) 62,798

Date of publication 24.02.2026

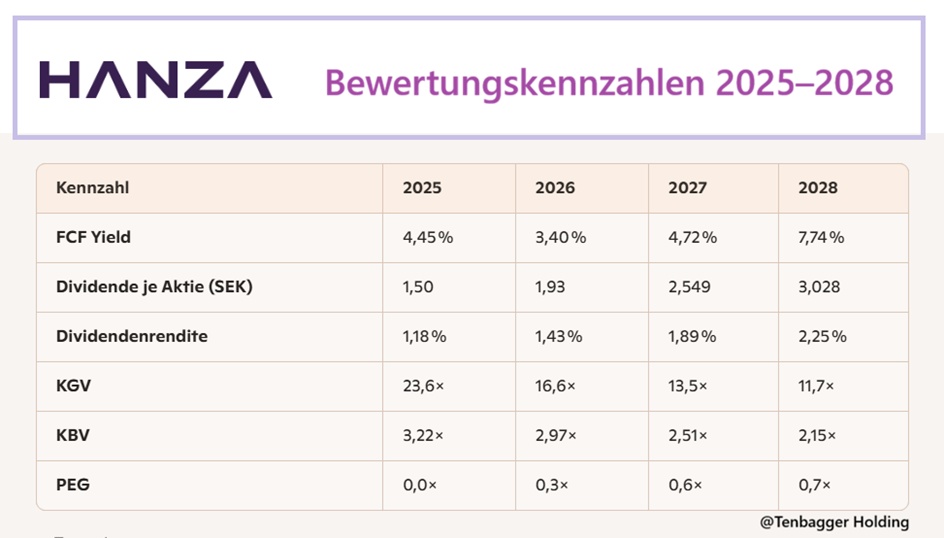

"Valuation falls faster than earnings rise - exactly the mix that attracts the market."

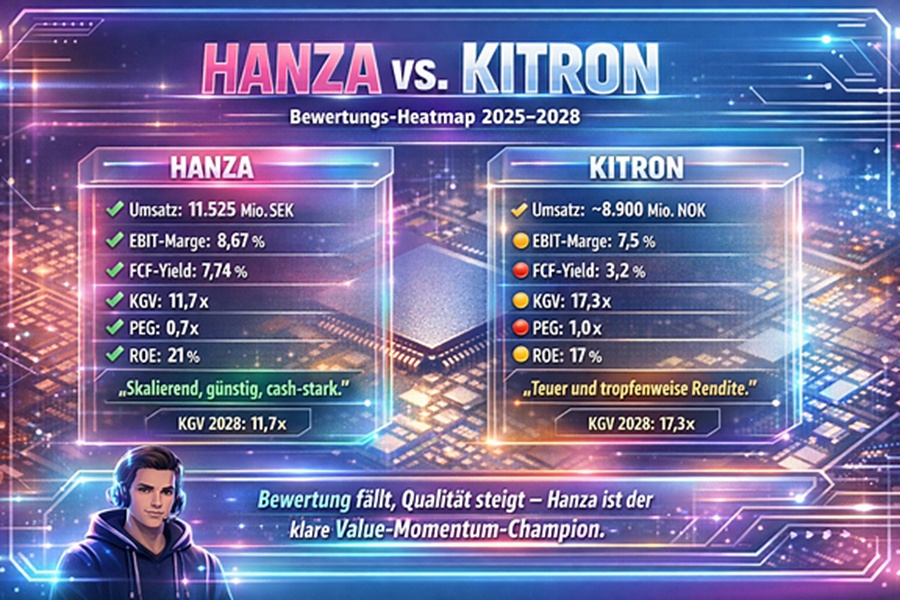

HANZA $HANZA (+1,81%)

KITRON $KIT (+1,12%)

"Hanza is pulling away from Kitron - stronger growth, better margins, double the cash power.

Kitron remains solid, but Hanza has long been in the value momentum orbit."

PRICE: €16.62 (07.05.2026 at 13:26) @Raketentoni