Endesa ($ELE (-0,93%) ) recently triggered a 🟢 OPTIMAL rating in DividendQuad. It's a great example of why traditional metrics don't always tell the whole story for capital-heavy sectors.

While its P/E of 18.28x currently looks slightly elevated, utilities have massive physical assets that depreciate on accounting books but maintain economic value. When we look at the metric that better reflects true cash generation for this sector—Price to Funds From Operations (P/FFO)—Endesa is trading at a very attractive 9.78x.

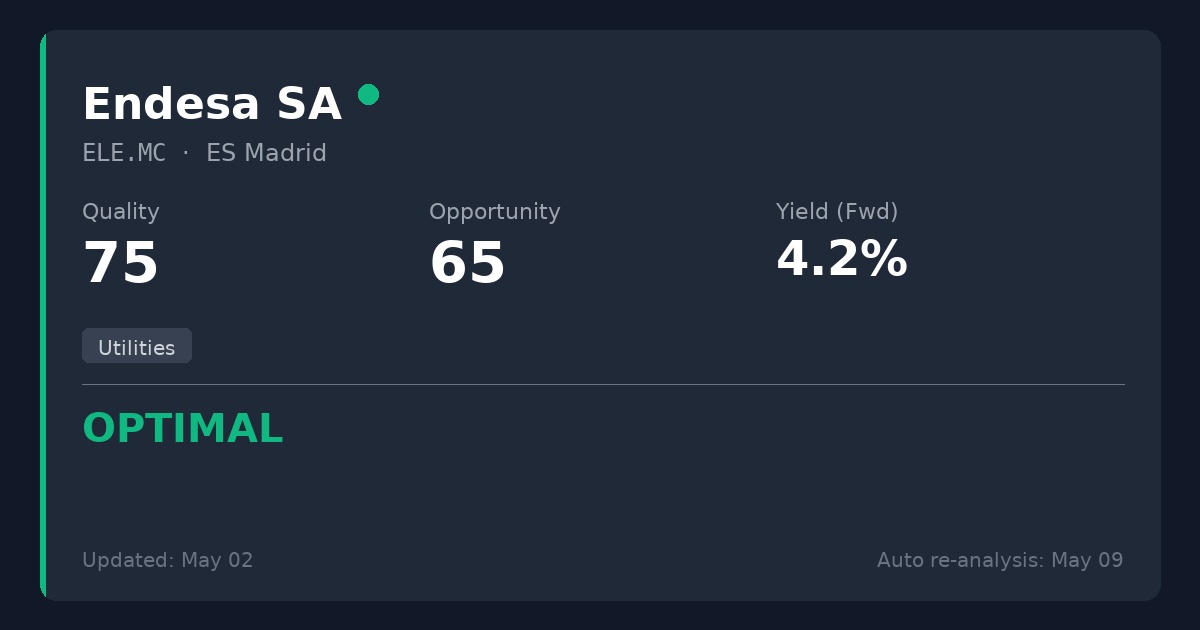

The Quad Stats:

• Quality Score: 75/100

• Opportunity Score: 65/100

• Dividend Yield: 4.20%

• Net Debt/EBITDA: 2.01x (Exceptionally strong for a utility)

• Cash Flow Payout Ratio: 34.3%

The Temporary Problem:

The stock is trading at a discount to its historical cash-flow valuations due to a confluence of short-term noise:

A recent one-time $570M arbitration penalty (which prompted a reactive dividend cut)

A CEO transition after 12 years (with parent company Enel asserting more control)

Regulatory probe headlines regarding historic blackouts

Ultimately, we are looking at a dominant market position with highly predictable, regulated cash flows. The 4.2% yield is extremely well-covered by real cash (34% FCF payout), backed by a balance sheet that is surprisingly fortress-like for the sector.