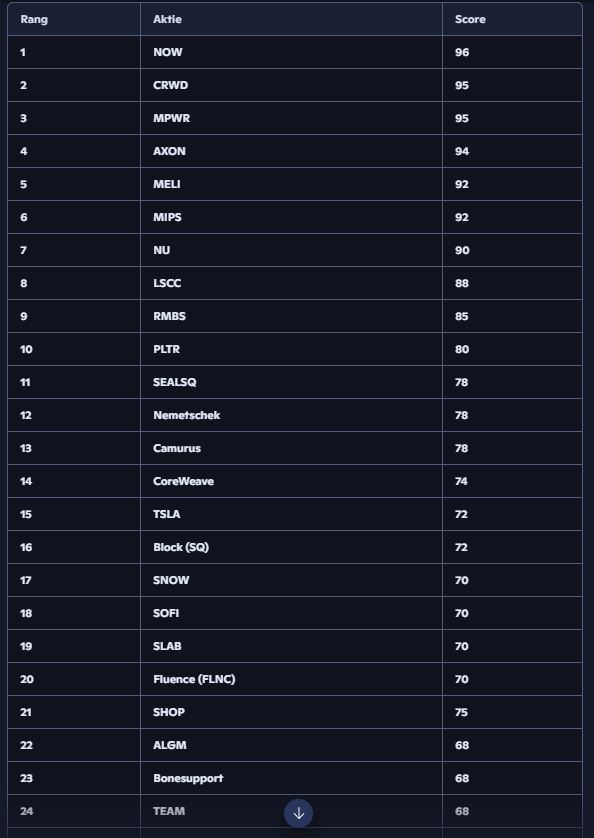

Over the weekend, I ran my stocks and my watchlist through a quality check once again. The AI was designed to evaluate companies based on 10 metrics (1–10 points per metric / max 100 points): moat, margins, EPS CAGR, balance sheet quality, TAM, future prospects, resilience, innovation, and management.

I found it particularly interesting how high up $MIPS (-1,96%) and $LAES (-1,75%) ranked. The business model of $MIPS (-1,96%) sounds rather boring and seems unremarkable, but the numbers are impressive. $LAES (-1,75%) At first glance, it looks like just another AI gimmick, but under the hood, it doesn’t look half bad. Is anyone here keeping an eye on these companies?

Positives:

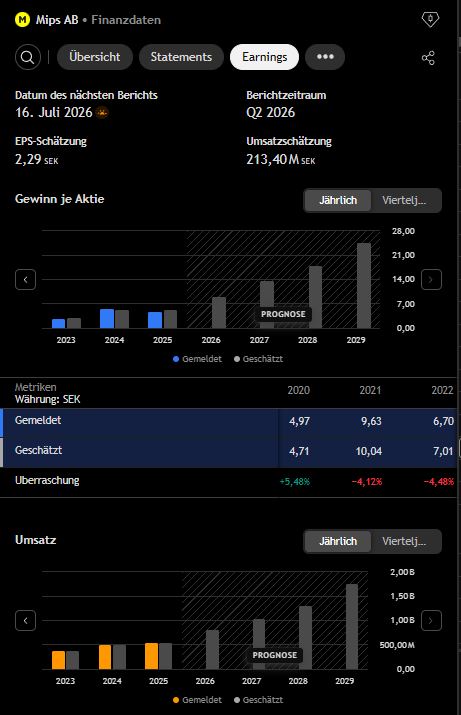

-MIPS has one of the purest IP moats in the entire small- and mid-cap universe

-A 70–75% gross margin for a physical product?

-EPS CAGR >25% and economies of scale

-MIPS management is the only one among the 40 companies to receive an 11/10 score from the AI

Negatives:

-TAM only 7 points because the safety TAM is limited

Positive:

-SEALSQ has a net cash position, which is is absurdly high

-SEALSQ is not a typical semiconductor player. It operates in a niche with extremely high barriers to entry

-PQC (post-quantum cryptography) is a regulatory S-curve

-asset-light security semiconductor (no factories, no millions/billions in CapEx)

Negative:

-EPS not yet fully scaling

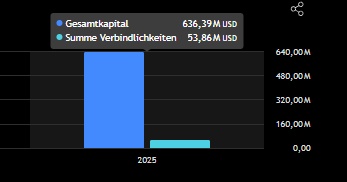

Balance Sheet $LAES (-1,75%)