The year is over, the last dividend has been collected. The result is great, next year will be better.

My YTD performance (-3% with dividends) is probably one of the worst on Getquin. I was too busy buying blue chip stocks in drawdown than chasing the market.

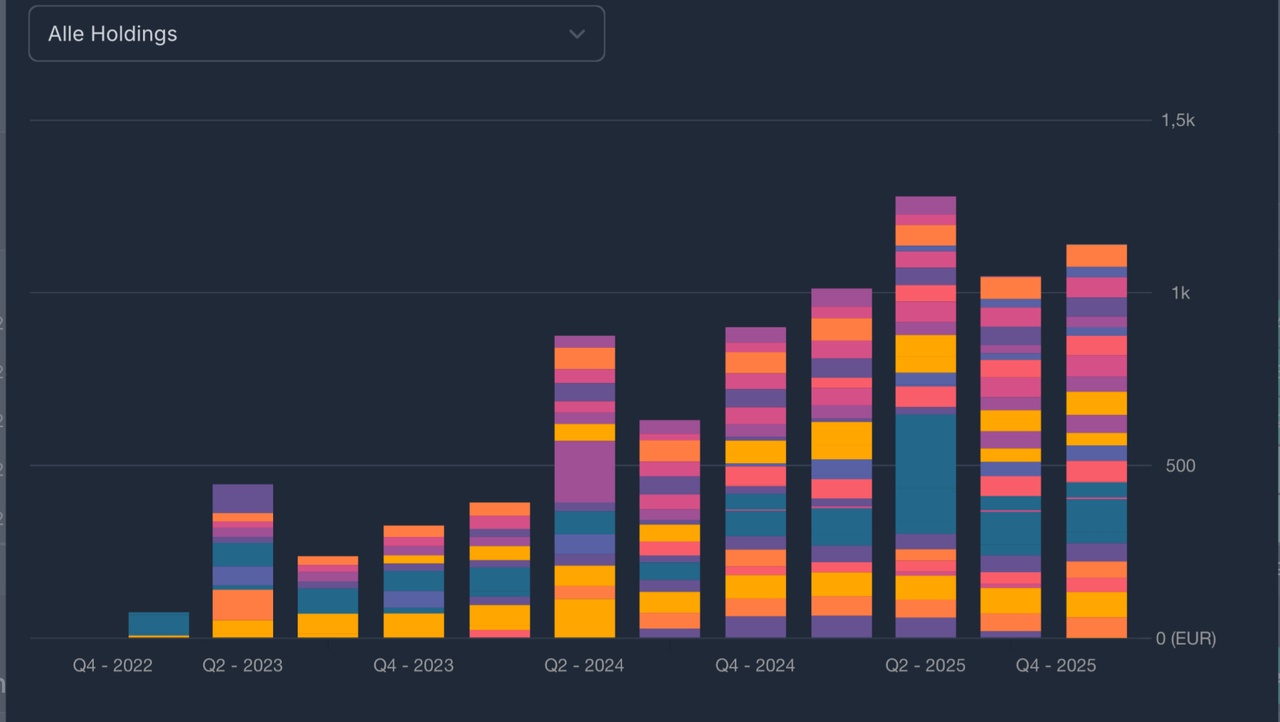

The portfolio now pays out over 5% gross p.a..

At the same time, the average dividend growth of the companies in the portfolio is over 8% p.a. based on the last 10 years. (Dividend growth is most important to me).

My 2026 target is clearly defined:

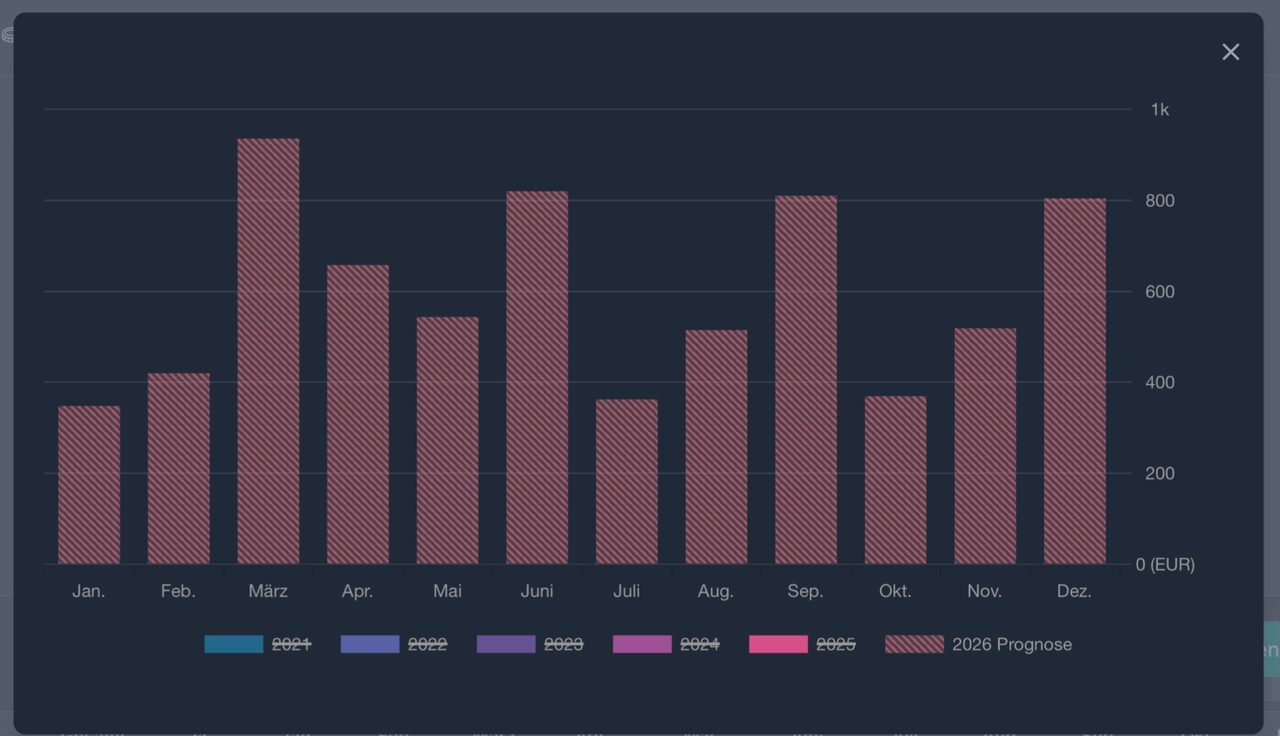

Gross annual dividends of over €10,000 without worsening long-term dividend growth.

Currently, my dividends are over € 7,100 gross (2026), which corresponds to around € 450 net per month.

Shares like $UPS (+0,3%), $GIS (+1,32%), $TGT (+0,68%), $DGE (+0,55%), $LYB (-2,21%) are unfortunately ruining my share price performance. However, this does not mean that I will no longer buy these companies. I tend to secure historically high dividend yields (YoC).

The focus is not on short-term performance, but on sustainable cash flow, rising dividends and long-term wealth accumulation.

My TTWROR since the beginning of my investment career is 54% (after tax) while an All World is slightly above 60%.