Hello my dears,

while Juan is still traveling in Asia and having fun in a Japanese theme park this weekend. I'm on duty for you and went shopping in Norway.

to Norway's

→ largest discount variety retailer,

to which Price-conscious buyers

→ like the large selection and low prices

And investors love the dividend yield and the good margins for a retail value.

As always, I look forward to your opinions and assessments in the comments.

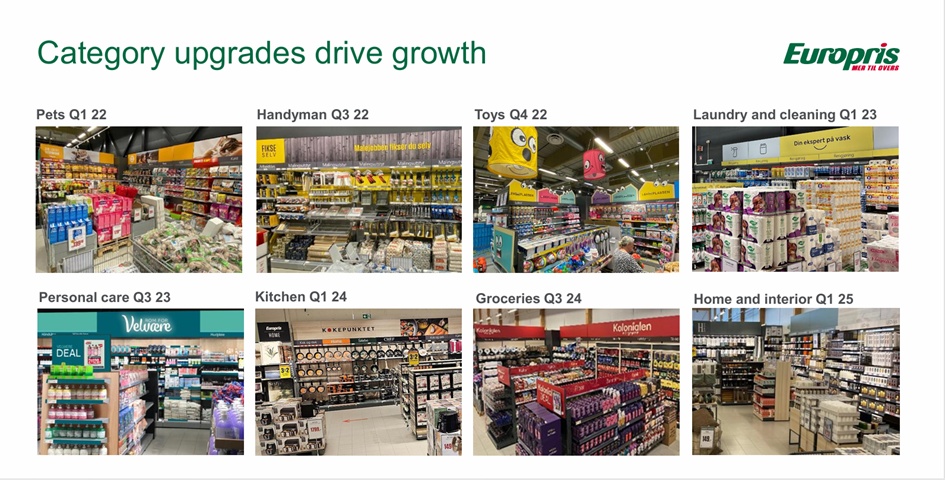

Europris ASA is a retailer based in Norway. The company offers its customers a wide range of private label and branded products in 15 product categories: Personal Care, Food, Laundry and Cleaning, Clothing and Shoes, Hobby and Office, Home Improvement, Travel, Sports and Leisure, Electronics, Chocolate and Snacks, Pet Food and Accessories, Carpets and Home Textiles, Kitchen, Home and Garden, Candles and Interiors, and Storage. The Group's goods are sold through the chain, which consists of a network of directly operated stores and franchise stores throughout Norway.

Number of employees: 4,313

The group consists of Norway's leading diversity chain, Europris, the Swedish retailer

retailer ÖoB and holds a partial stake in the e-commerce groups

Lekekassen and Strikkemekka. The Europris chain operates 289 stores in Norway

(268 directly operated and 21 franchise locations), while ÖoB has 92 directly

directly operated stores throughout Sweden and Lekekassen has two physical stores in Norway.

stores in Norway. The Group's activities are managed from its headquarters in

Fredrikstad, Norway, with logistics centers in both Norway and Sweden.

Solid performance driven by strong customer relevance and conversion,

The first quarter reflected a strong performance in Norway and continued progress in Sweden.

in Sweden. The Europris concept continued to demonstrate its

relevance, with solid sales growth driven by increased store traffic and

store traffic and continued volume growth. The first

quarter showed a robust operating performance and total sales growth of 12.3% year-on-year.

year-on-year growth of 12.3%. An earlier timing of Easter this year is said to have contributed around 6 percentage points to sales growth

(Complete key figures + outlook can be found under the link)

Solide Leistung, getrieben von starker Kundenrelevanz und -umsetzung,

Geographical distribution of sales:

2025 (NOK)

Norway 10.59 bn

Sweden 4.29 billion

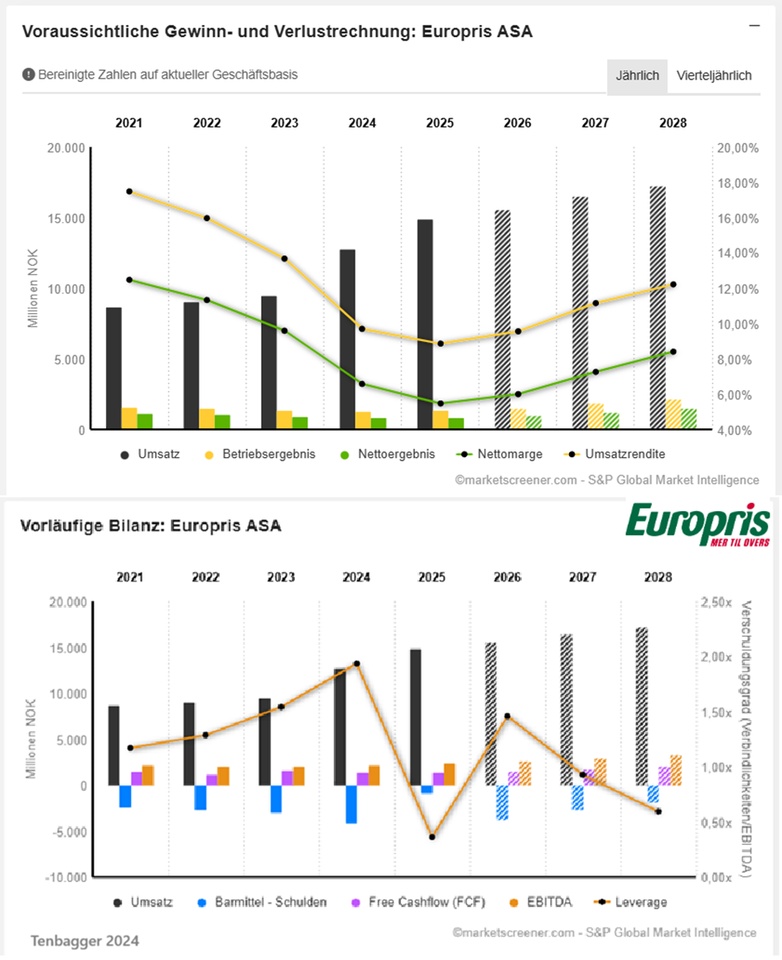

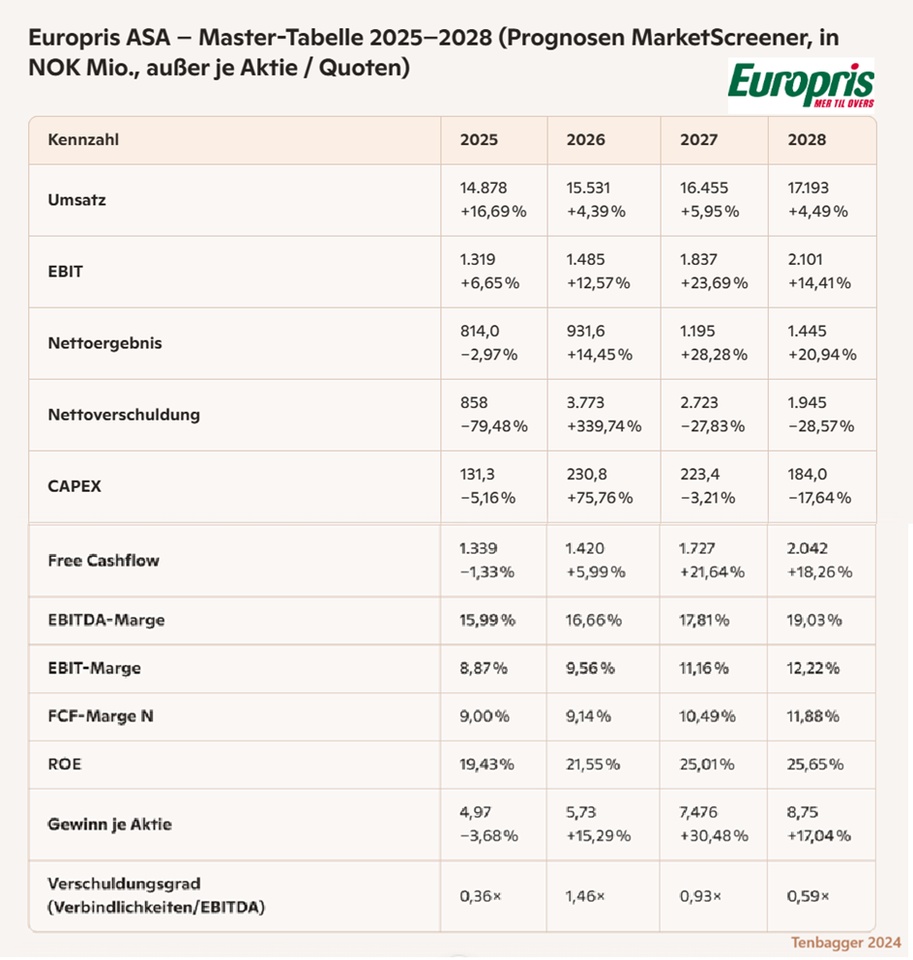

Juan conclusion on the key financial figures (Europris ASA 2025-2028)

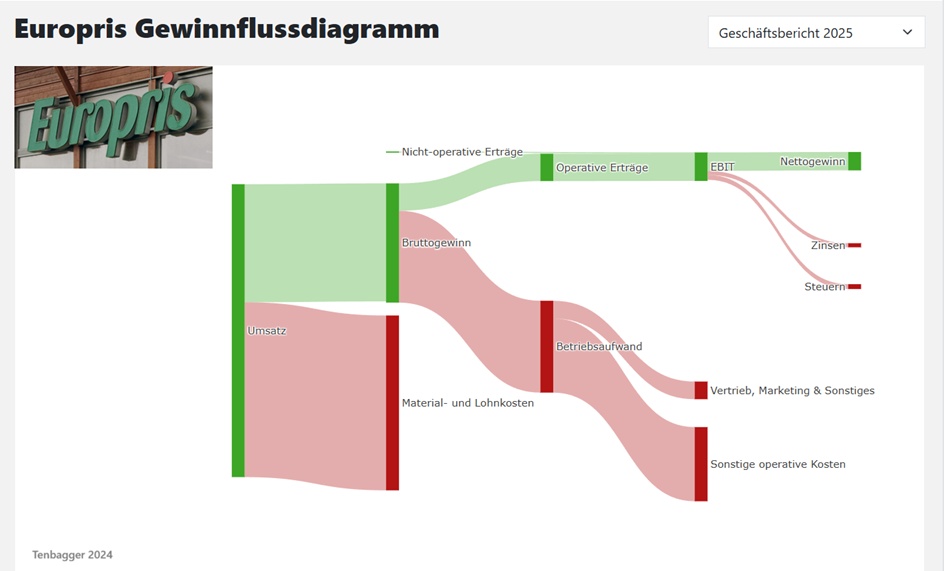

Europris delivers a consistently strong, almost "textbook" foundation: Sales, EBIT and net profit increase steadily every yearand profitability even increases significantly from 2027 onwards. The margins are continuously improvingwhich shows that the business model is scalable and pricing power remains available.

The free cash flow is growing stronglyremains clearly positive and easily covers CAPEX - a quality feature. The ROE development is strong and is in the upper quality segment.

The only outlier: the net debt jumps up in 2026but then falls back again significantly. The leverage ratio remains relaxed and uncritical overall.

In short: Europris has a robust, cash-strong profile with rising profitability and a good return on capital. Operationally clean, financially solid, fast-growing - exactly the kind of setup Juan likes.

Market value 16,185

Number of shares (in thousands) 163,649

Date of publication 28,01,2026

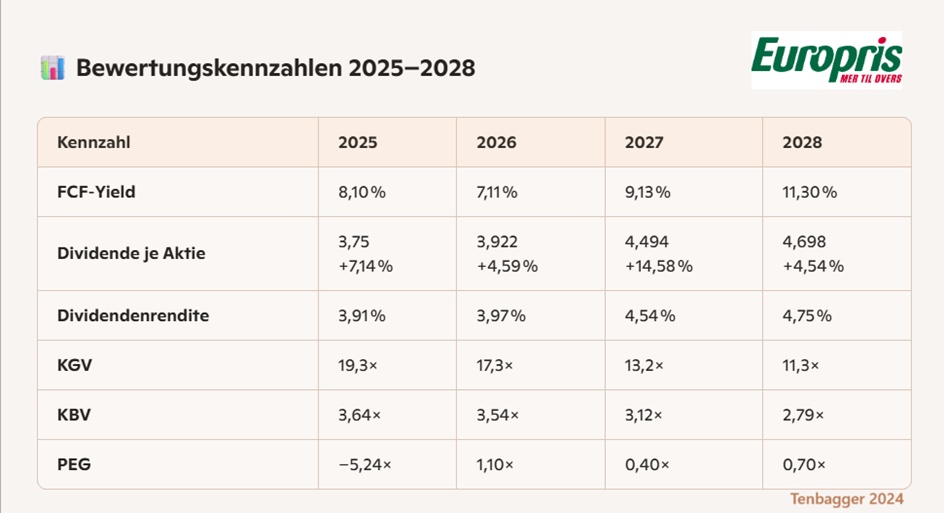

Juan conclusion on the valuation ratios (Europris ASA 2025-2028)

On the valuation side, Europris looks like a classic "quality compounder" that has just entered a more attractive valuation zone into a more attractive valuation zone. The P/E ratio is falling year on yearwhile profits and cash flows are rising - a setup that removes valuation pressure and creates scope for re-rating.

The FCF yield picks up strongly from 2027 and reaches a double-digit level in 2028. This is remarkably strong for a defensive retailer with stable cash flows. At the same time, the dividend yield remains solidly risingwithout the distribution burdening the balance sheet.

The PEG slips into the "sweet spot" zone from 2027 below 1 - a clear signal that growth and valuation fit together again. P/B ratio is also falling continuously, reflecting the rising return on capital.

In a nutshell: Europris is getting cheaper every year, while quality, cash flow and growth are improving. Exactly the kind of valuation profile that Juan likes to take a closer look at.

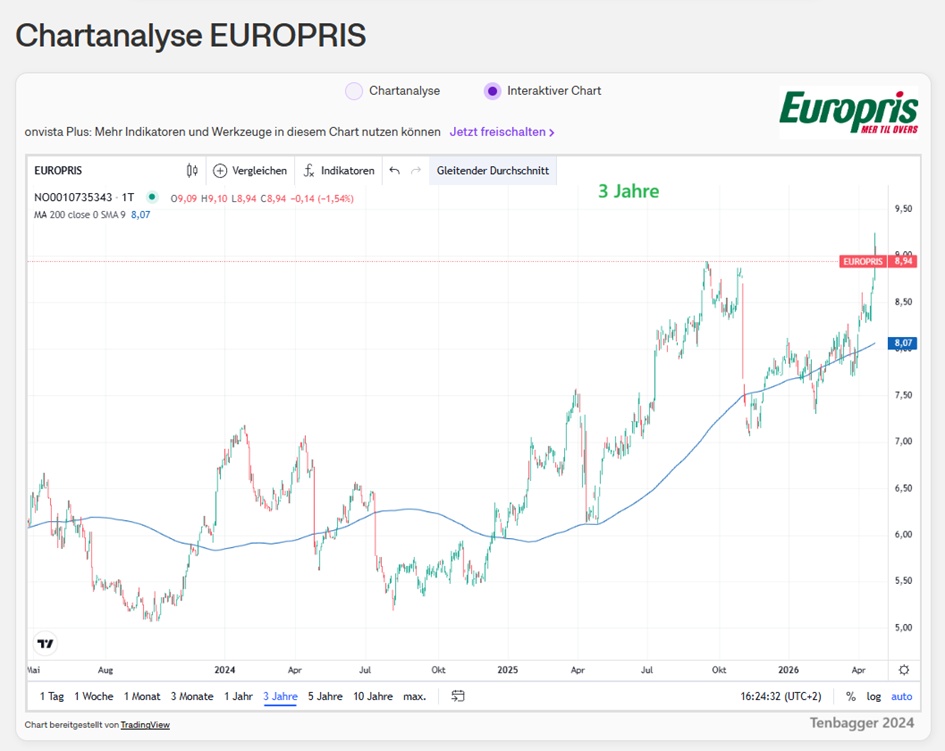

PRICE 8.945€ (25.04.2026 at 12.25)