PVA TePla ($TPE (-4,46%)

) is one of the most strategically important European specialty machine manufacturers in the semiconductor ecosystem. The company supplies the core technologieson which silicon wafers for AI chips, power electronics and solar products are produced - a niche market with extremely high barriers to entry.

⚙️ What does PVA TePla do?

➡️ Crystal Growing Systems: Foundation for 200mm & 300mm silicon wafers (Logic, Power, AI).

➡️ Metrology & quality inspection: Ultrasound, CT scanning, wafer inspection - essential for yield & defect detection.

➡️ Plasma & vacuum systems: Surface treatment & material technology.

➡️ CustomersTop semiconductor manufacturers, photovoltaics, research, battery tech.

📍LocationWettenberg (Hesse), globally active in USA, Asia & Europe.

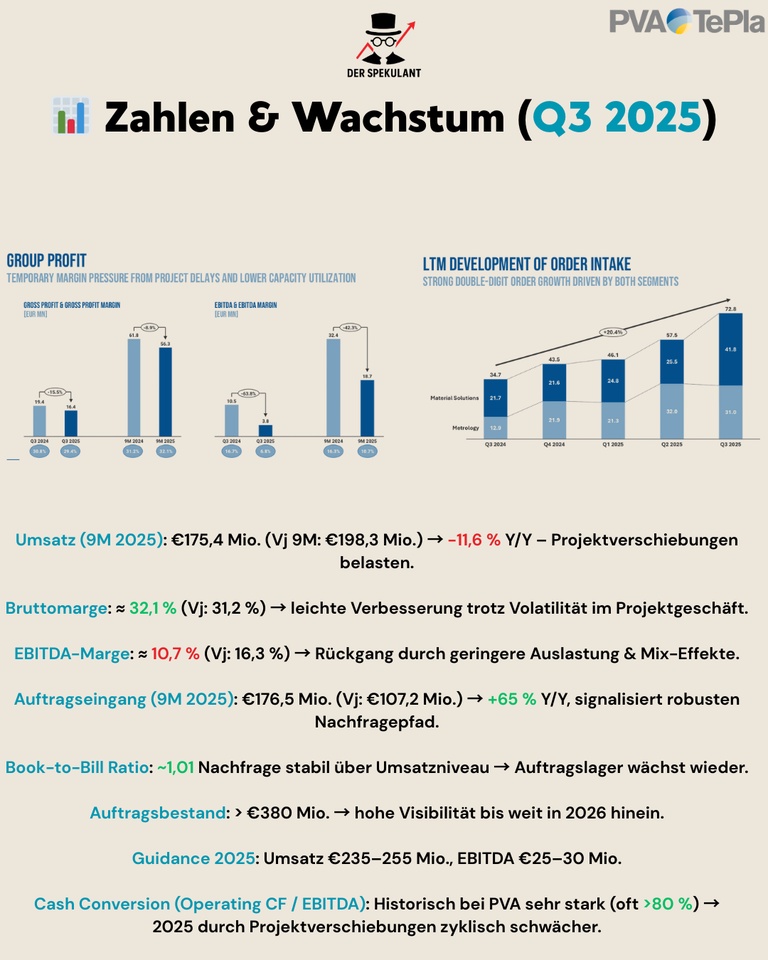

📊 Figures & growth (Q3 2025)

📊 Turnover 9M: €175.4 million (previous year €198.3 million) → -11,6 % (project postponements)

📊 Gross margin: ~32,1 % (previous year: 31.2 %) → slight improvement

EBITDA margin: ~10,7 % (previous year 16.3 %) → lower capacity utilization

📊 Incoming orders: €176.5 million (previous year €107.2 million) → +65% Y/Y

📊 Book-to-bill ~1.01 → Stable demand

📊 Backlog: > €380 million → Capacity utilization until 2026

🔮Guidance 2025: Revenue €235-255 million, EBITDA €25-30 million

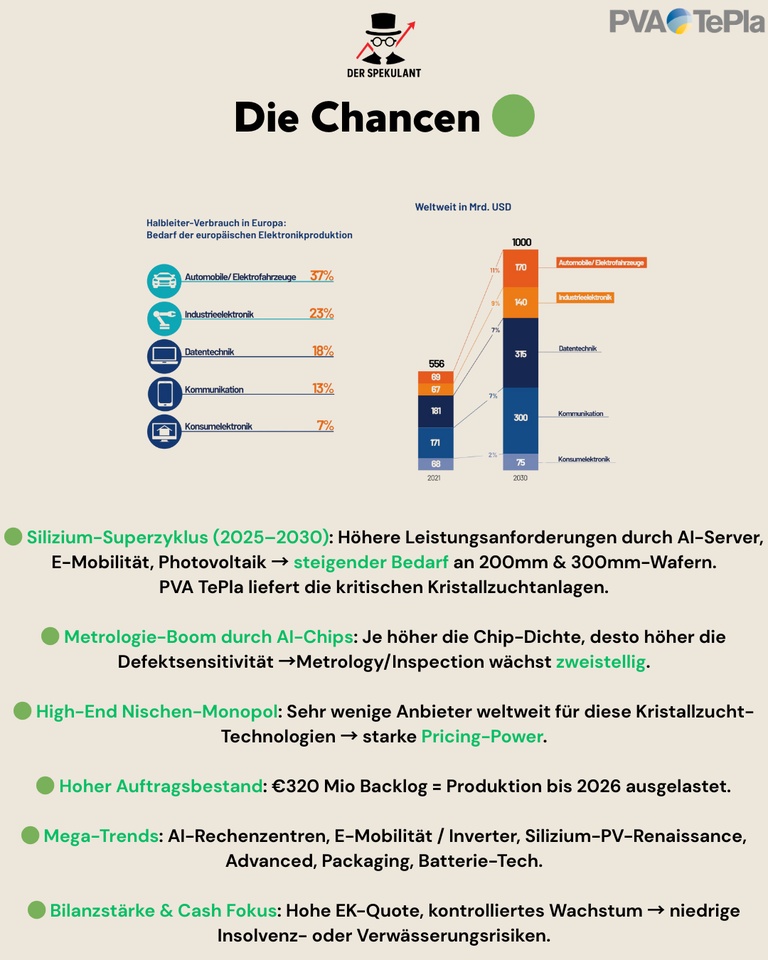

🟢 The opportunities

🧠 Silicon supercycle (2025-2030)AI servers, e-cars & PV drive global wafer demand → PVA supplies the key technologies.

📈 Metrology boom due to increasing chip densityMore layers → higher defect sensitivity → strong double-digit growth in inspection & yield optimization.

🏆 High-end niche monopoly: Only a few players worldwide in CZ crystal growing & high-end inspection → Strong pricing power.

📦 High order backlogBacklog €320-380 million → Production firmly secured until 2026/27.

🔋 Mega trendsAI data centers, e-mobility & inverters, silicon PV renaissance, battery tech, advanced packaging.

💰 Balance sheet strength: High equity ratio, low debt → strong profile as a German tech SME.

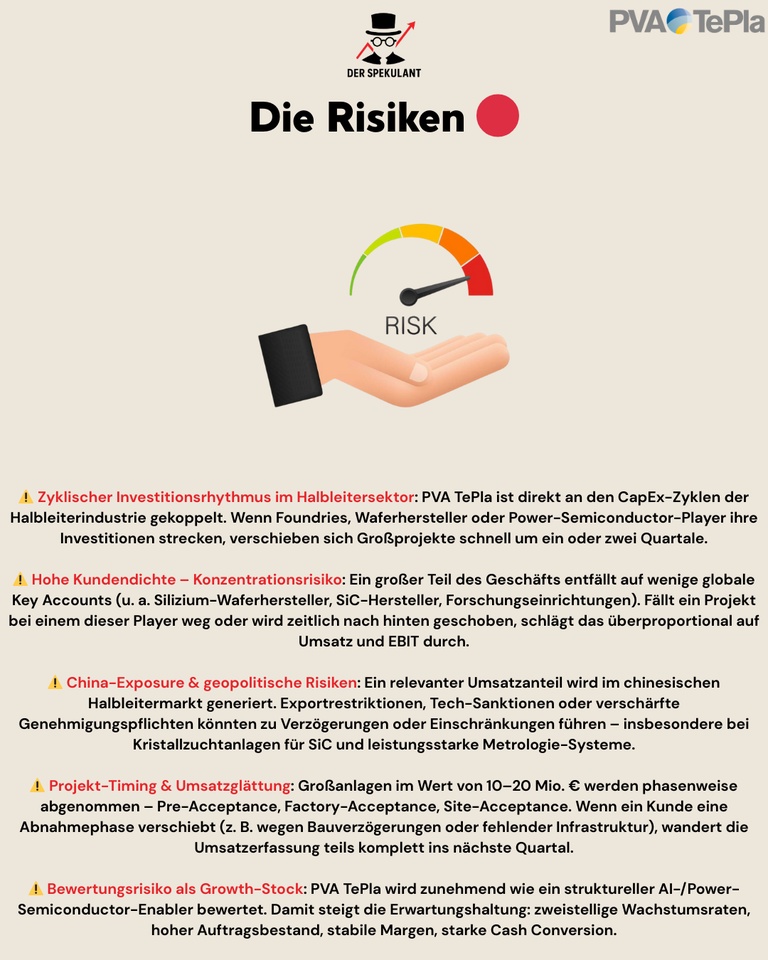

🔴 The risks (professional & detailed)

⚠️ Cyclical investment rhythmPVA TePla is directly linked to the CapEx cycle of the semiconductor industry. When foundries & power semi players postpone investments, large orders quickly slip by one or two quarters. one or two quarters. This creates volatility in sales and margins.

⚠️ High customer density / concentration risksA large proportion is accounted for by just a few global key accounts (silicon wafers, SiC manufacturers, research).

If a project is canceled or postponed, the impact on sales & EBIT disproportionately - typical for specialty machinery manufacturers.

⚠️ China exposure & geopoliticsRelevant sales in the Chinese semiconductor market: export restrictions, licensing requirements or sanctions can lead to delays - particularly in silicon crystal growing and high-end metrology.

⚠️ Project timing & sales smoothingLarge systems (€ 10-20 million) are accepted in phases (pre-acceptance, FAT, SAT). If a customer postpones acceptance, the entire revenue recognition is postponed to the next quarter → high quarterly fluctuations.

⚠️ Valuation riskPVA is increasingly traded as an "AI enabler" & structural growth stock. This means: two-part growth expectations are in the share price. Any margin or cash flow weakness leads to disproportionate corrections.

💡 Conclusion & outlook

PVA TePla remains one of the most exciting German tech hidden champions:

extremely strong structurally in the long termcyclical in the short term. AI chips, PV renaissance, power semiconductors & metrology are the growth drivers until 2030.

🎯 Long-term target

Sales direction €400-450 million, margins 15 %+, strong metrology leverage.

💬 Community question

PVA TePla - underestimated German hidden champion or too cyclical for a tech portfolio?