In the course of my research on Christopher Hohn, I came across an exciting turnaround story in which 100% is possible in 2 years. I would like to share this with you. I find it exciting. Today I will also be building up the first position in this company. It's about Cellnex $CLNX (-0,02%) . But first a few words about Chris Hohn:

Who is actually Chris Hohn? First of all: Sir Christopher Hohn is the man behind the hedge fund TCI. He is one of the most successful activist investors in the world. His style: he makes extremely concentrated bets on companies with a "moat" (such as Visa, GE or Alphabet) and forces the management to make radical price changes when necessary. He does not invest in hope, but in hard-hitting cash flow machines.

This is exactly what Cellnex ($CLNX) (-0,02%) has done.

The back story: Growth at any price

Cellnex $CLNX (-0,02%) was the darling of growth investors for years. The model: buying up radio masts throughout Europe, financed by cheap debt. But with the turnaround in interest rates, this no longer worked. The share price plummeted and the debt burden put massive pressure on the share price.

Hohn's intervention

Hohn saw the intrinsic value of the infrastructure, but lost patience with the strategy. He increased his stake to around 9% and forced the upheaval:

- Management change: He demanded the resignation of the old management and appointed Marco Patuano as the new CEO.

- Change of strategy: No more expensive acquisitions, focus on the balance sheet and cash flow.

- Asset sales: Sale of peripheral businesses (e.g. in Austria and Ireland) to pay off debt faster.

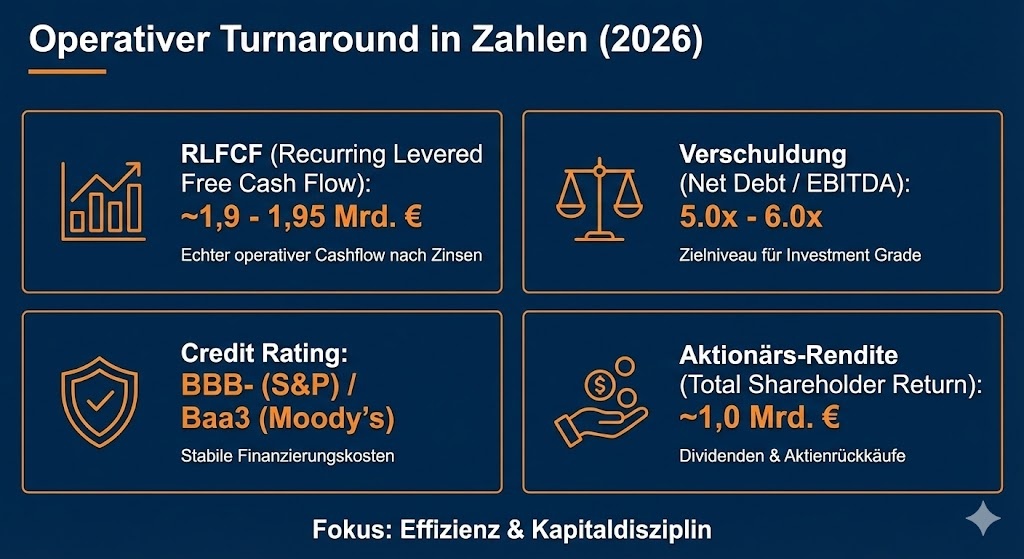

The turnaround in figures (the cash flow engine)

The key figures for 2025/2026 show that Hohn was right. The focus is no longer on sales figures, but on what remains at the end:

- Operating cash flow (RLFCF): Cellnex now delivers a massive Recurring Levered Free Cash Flow of approx. 1.9 to 1.95 billion euros, which means 17% yield (!)

- Cash flow growth: RLFCF per share is growing at rates of over 13 %.

- Debt: The ratio has been reduced towards 5.0x to 6.0x EBITDA which would have improved the investment grade rating (BBB-) and stabilizing interest costs.

- Shareholder return: The target for 2026 is to generate approx. 1 billion euros to shareholders (divided into dividends and share buy-backs).

Cellnex $CLNX (-0,02%) will publish its results for the 2025 financial year on February 27, 2026 will be presented. This date is regarded as the "moment of truth" for the strategy driven forward by Chris Hohn (TCI).

Conclusion

The story is simple: Cellnex has stopped being a "perpetual construction site" and is starting to become a "toll booth". Now that Chris Hohn has trimmed the company for efficiency, the focus is on how this massive cash flow increases the value per share. The turnaround is no longer a promise, it is already taking place in the figures.

The share has been oscillating around €25 for several months. It has very probably bottomed out after a few years. I have built up my first position.

#Cellnex

#ChrisHohn

#TCI

#Turnaround

#Cashflow

#ValueInvesting

#Infrastruktur