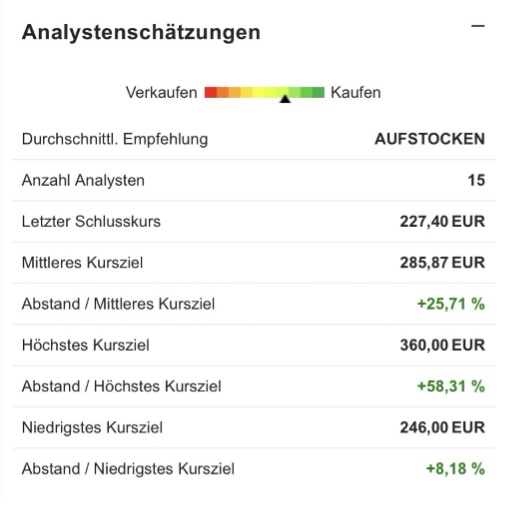

It's been a long time since I've written a stock analysis. But today it's that time again, it will be about Hannover Re $HNR1 (+0,36 %). As always, we will systematically analyze the share and then give a conclusion at the end. Of course, as always, this is not investment advice and only reflects my own opinion.

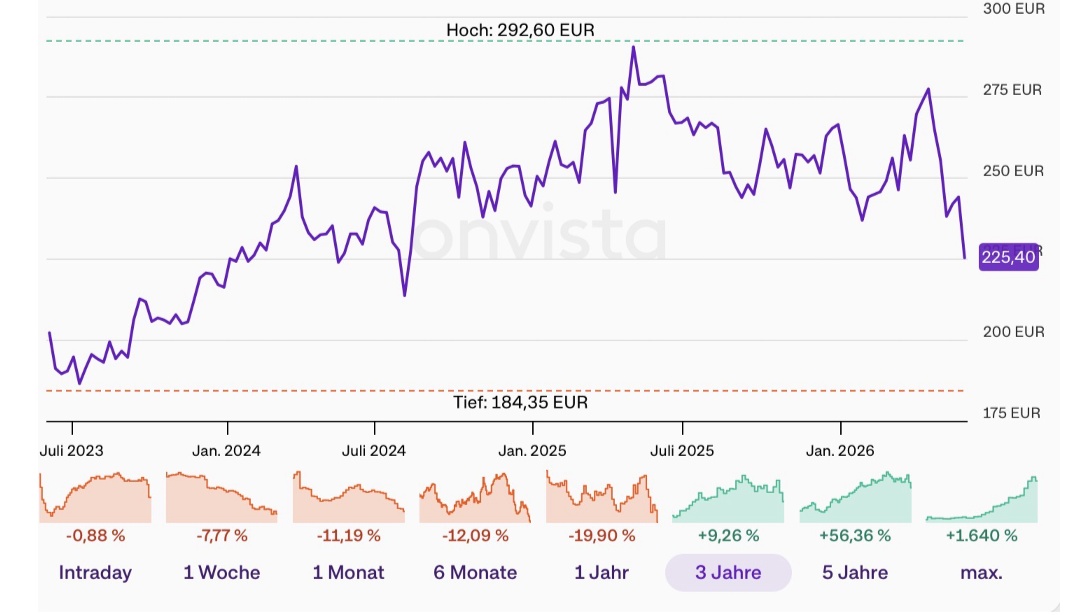

The share has lost 23% since its high of €292.60 and is currently trading at €225.40.

In terms of the chart, we are now falling from above onto a larger support area. If this holds, the price could stabilize and perhaps even end this correction. However, if we fall below it at the end of the week, the probability of further losses increases. Looking only at the chart, I would put Hannover Re on my watch list and keep a very close eye on it. In principle, however, I can imagine that we have not quite reached the end yet.