When I analyze Siemens Healthineers $SHL (+0,11 %) I am not interested in the next quarterly figures, but in the question:

Will the company earn more in 10 to 20 years than it does today?

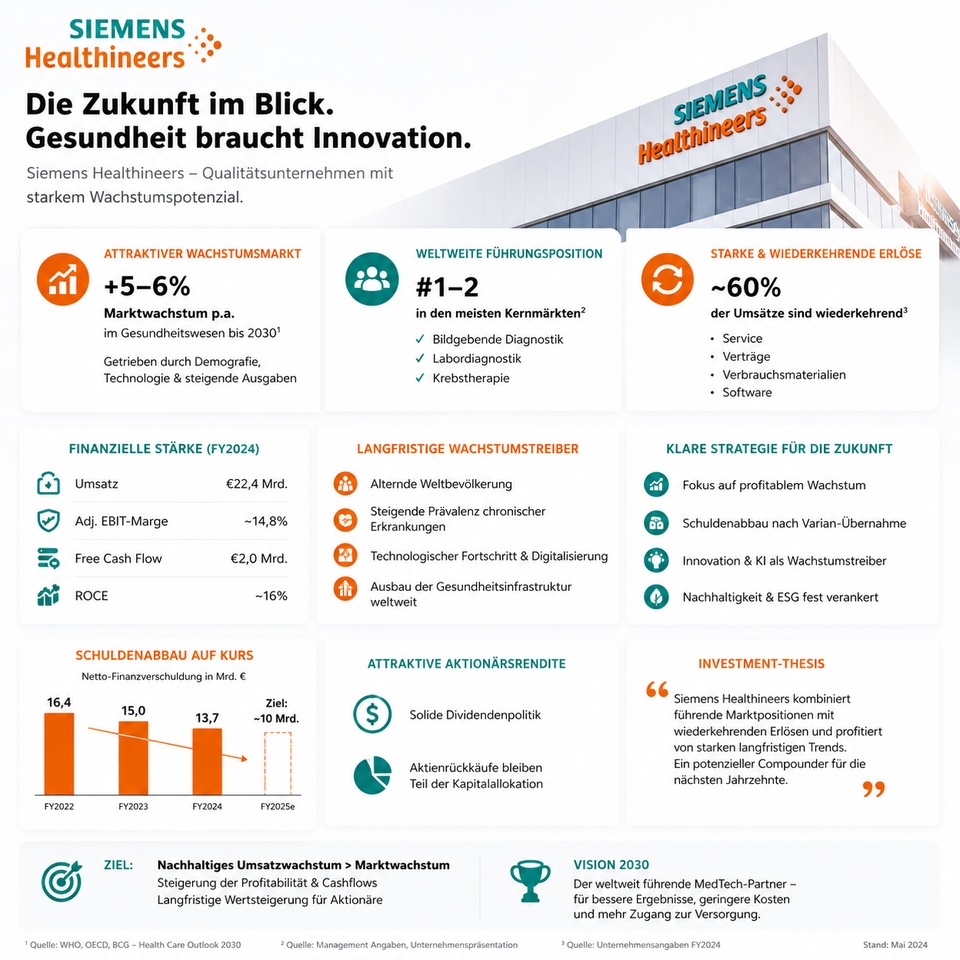

The figures speak for themselves.

Market position

- Global leader in MRI and CT

- Over 70,000 systems installed worldwide

- Customers are mainly hospitals, university clinics and laboratories

- High regulatory hurdles and switching costs

Business quality

- Turnover 2025: around € 22 billion

- Adjusted EBIT margin: around 15%

- Free cash flow: around € 2 billion

- Billions in sales from service, maintenance, software and consumables

A hospital does not replace an MRI system like a laptop. Devices often remain in use for 10-15 years and generate recurring revenue over their lifetime.

The moat

- High acquisition costs

- Long-term service contracts

- Trained personnel

- Regulatory approvals

- Integration into hospital processes

It is precisely factors like these that ensure that market leaders can defend their position for decades.

The tailwind

By 2050, the number of people over the age of 60 worldwide will increase to over 2 billion.

More older people means

- more diagnostics

- more cancer treatments

- more cardiovascular diseases

- more imaging procedures

Health expenditure is rising faster than GDP almost everywhere.

Varian takeover

Many investors focus on the debt.

I focus on the strategic position:

Today, Siemens Healthineers earns money not only from diagnosing cancer, but increasingly also from treating it.

This considerably expands the addressable market.

The crucial question

If Siemens Healthineers generates sales of around €22 billion today and healthcare spending continues to rise worldwide in the coming decades:

How likely is it that the company will be worth less in 2035 than it is today?

For me, Siemens Healthineers is not a speculative stock.

It is a quality company with:

Exactly the kind of company that often creates more value in the long term than most market participants expect.

- strong moat

- structural growth

- recurring revenues

- high return on capital

- global market leadership