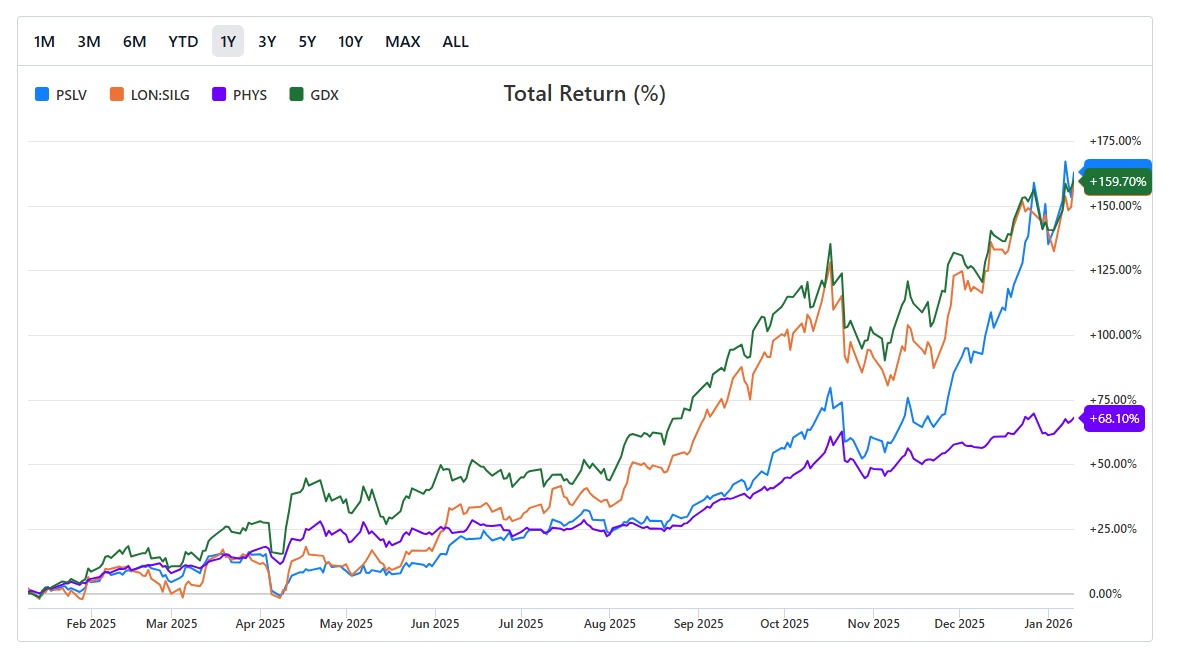

On January 30th the price of silver ($965310) (+4,07 %) crashed over 30% in one day. Since then the price has been relatively flat (but still volatile). Does that mean the end of the historic silver squeeze that was happening? In my opinion it does not and here are three reasons why I think silver could soon start a new leg up.

1. Physical Drain Is Breaking the Paper Market

The crisis in physical silver is no longer theoretical. In just seven days in January 2026, 33.45 million ounces were physically withdrawn from COMEX, roughly 26% of registered inventories vanishing in a single week. Meanwhile, COMEX carries 366 million ounces in open interest contracts for March delivery but holds only 102 million ounces available to settle them. The LBMA's eligible silver stocks have shrunk to approximately 155 million ounces against annual floating demand of 900 million to 1.2 billion ounces. The Shanghai exchange only holds 25 million ounces.

Sprott's data shows the cumulative physical deficit from 2021–2025 totals nearly 800 million ounces. Mine supply has actually declined 7% since 2016, meaning this gap is structural, not cyclical. Industrial users are now signing long-term supply contracts directly with miners, bypassing exchanges entirely. We currently see backwardation (spot price higher than futures price) a signal that buyers no longer trust exchange delivery.

2. China's Export Licensing: The Supply Shock Nobody Was Ready For

Starting January 1, 2026, China replaced its silver export quota system with a strict licensing regime. Only 44 companies have been authorized to export silver globally for 2026–2027. To qualify, an exporter must produce at least 80 tonnes annually and maintain $30 million in credit lines, instantly eliminating hundreds of small and mid-sized suppliers.

The practical effect: China has cut off 60–70% of globally tradable silver supply. This mirrors China's rare earth playbook, first dominate production, then weaponize export controls for geopolitical leverage. The U.S. government, recognizing the strategic dimension, designated silver as a critical mineral in November 2025.

3. The 356:1 Paper-to-Physical Ratio: A Mathematical Impossibility

The most explosive catalyst is the one hiding in plain sight on COMEX's own data: a paper-to-physical ratio of approximately 356:1. For every single ounce of deliverable physical silver in exchange vaults, 356 paper contracts claim ownership of it.

This mirrors and even exeeds the conditions that preceded the 1979–1980 Hunt Brothers crisis, when silver briefly hit $50. The critical difference: the 1979 crisis was driven by private speculators who could be stopped by exchange rule changes. Today's squeeze is being driven by sovereign governments draining physical metal into national stockpiles, a force that no exchange rule change can reverse. China and India are buying physical through spot and deferred delivery contracts, and that metal disappears into state vaults and does not return to market. When short sellers on COMEX are forced to deliver metal they do not have, they must buy at any price. That dynamic, once triggered at scale, is what transforms a strong bull market into a historic repricing event.

The Gold-Silver Ratio Math

The final piece is simple arithmetic. The historical monetary gold-to-silver ratio averaged 15:1 to 16:1 when both metals functioned as money. With gold currently trading above $4,500 per ounce, a reversion to a 15:1 ratio produces a silver price of $300 per oz. The ratio currently sits near 60:1. The correction, when it comes, tends to be violent and fast.

TLDR;

The market fundamentals didn't change since last year. There is still a fundamental shortage, there is still a possible short squeeze and the gold/silver ratio is still relatively high. All pointing to a significantly higher silver price in the near future.

What are your views on silver? Is the run over, or will we see more explosive price action? I'm still holding on to my position. Are you?