Mid-April 2025 finds the dry bulk market caught in a stormy swirl of trade wars, weather woes, and shifting cargo flows. Capesize rates falter under tariff pressures, panamax struggles with muted demand, yet supramax and handysize find flickers of resilience. Sanctions, port fees, and production cuts reshape routes, while AI whispers promise for efficiency. This is a sector battling headwinds with grit—let’s chart its course.

⏬ Capesize Market: Weathering the Squall

Earnings Snapshot

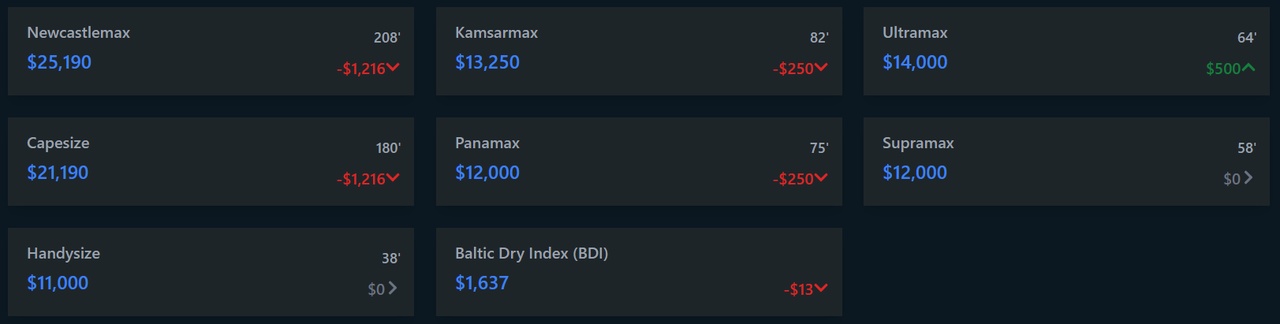

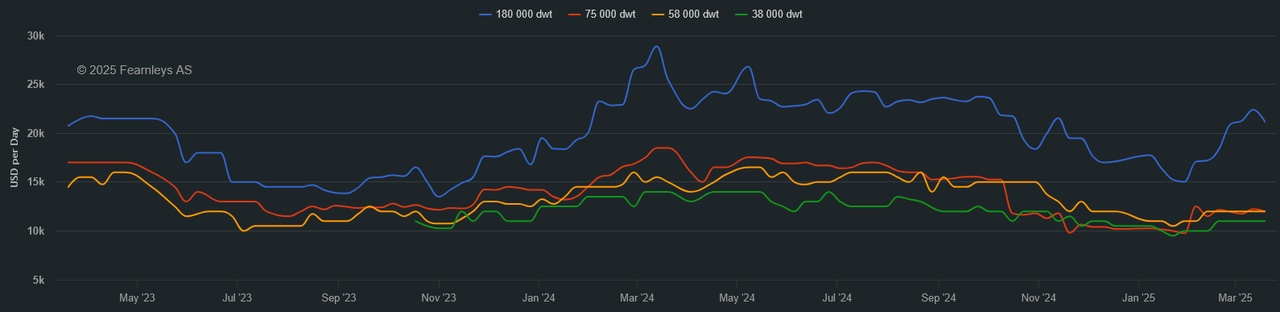

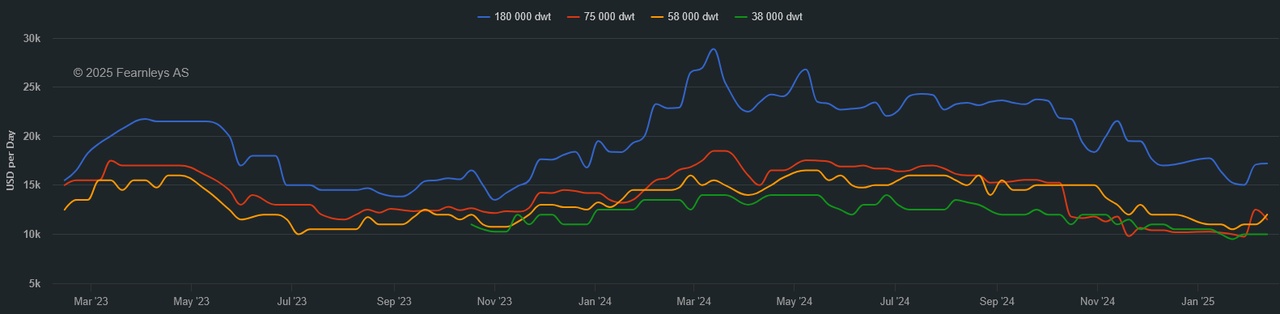

Capesize bulkers, the iron ore titans, sail through choppy waters as rates skid to a six-week low. The Baltic Exchange’s index averages $15,148 per day, a 9% drop week-on-week, with a mid-week dip to $14,367 before a slight rebound. March highs of $24,000 per day feel distant, with West Australia-to-Qingdao (C5) rates plunging to $7.79 per tonne (down 25% weekly, though up 35% in a day) and Brazil-to-China (C3) at $18.74 per tonne after an 18% tumble. Weak Chinese iron ore imports (down 6% year-on-year in March) and tariff shocks drag sentiment, yet fundamentals hint at stabilization.

Demand and Supply Pressures

Extreme weather batters key exporters. Rio Tinto’s Pilbara shipments fall 9% to 70.7 million tonnes in Q1, hit by four cyclones costing 13 million tonnes—2025 guidance leans toward the low end of 323-338 million tonnes. Vale’s Brazilian output slips 4% to 67.7 million tonnes, though sales rise 4% to 66.1 million tonnes. China’s Q1 iron ore arrivals drop 9%, with port stocks down 6 million tonnes to 150 million. Yet, Fearnley Securities eyes April import normalization, and Brazil’s March exports climb 8%. Tariff fears curb Pacific activity—Rio Tinto fixes Dampier-to-Qingdao at $7.70 per tonne—while Atlantic routes like Tubarao-to-West Africa hit $18.15 per tonne.

Global Headwinds

U.S.-China tariffs (145% vs. 125%) and EU countermeasures jolt the market, with Braemar noting a “freefall” tied to Trump’s trade moves. A three-month tariff pause lifts forward freight agreements (FFAs) to $16,000 per day for April and $18,000 for Q2, signaling cautious optimism. However, Vale’s vague 325-335 million tonne guidance and Colombia’s coal cuts (Cerrejon down to 11-16 million tonnes) dim cargo hopes—capesize battles to hold its course.

Iron ore is loaded at the Ponta da Madeira terminal in Brazil - For illustrative purposes

⏳ Panamax Market: Adrift in Uncertainty

Rate Struggles

Panamax bulkers, versatile grain and coal carriers, drift in a softer market. Baltic Panamax Index rates hover around $11,500 per day, down 7% week-on-week, reflecting tariff-driven gloom and weaker coal flows. Secondhand prices for five-year-old vessels fall 12% from Q3 2024 peaks, per Veson Nautical, as global uncertainty stifles demand. Activity remains subdued, with limited fixtures reported—owners eye stabilization as bunker price swings complicate voyage trades.

Regional Dynamics

Colombia’s coal output cuts weigh heavily—Cerrejon’s reduction to 11-16 million tonnes (from 19 million in 2024) slashes capesize and panamax cargoes. Exports to Asia-Pacific (South Korea: 10 million tonnes, China: 6.65 million tonnes) rise, but long voyages (55-67 days) and high freight costs deter buyers. China’s coal imports from Colombia drop to 2 million tonnes in Q1 (from 3.9 million), favoring Australian coal’s $14 per tonne CFR price edge. Panamax shipments fall 24.6% to 11 million tonnes as capesize takes share—owners face a thinning cargo pool.

Trade Shifts

U.S. port fee fears for Chinese-built ships (70% of panamax orderbooks) push buyers toward Japanese tonnage, per Pacific Basin’s Martin Fruergaard. Scaled-back fees ($18 per net tonne, rising to $33 by 2028) ease concerns, but contractual haggling looms. Glencore’s Colombian cuts and EU decarbonization shift coal to Asia, stretching tonne-miles yet exposing fragility—panamax treads water, seeking firmer ground.

Coal being loaded onto a ship in the port of Jiujiang - For illustratives purposes

⏱️ Supramax Market: Flickers of Fortitude

Earnings Resilience

Supramax bulkers, nimble mid-sizers, show grit amid market malaise. Pacific Basin’s supramax fleet earns $12,210 per day, 55% above the Baltic Supramax Index, with Q1 operating margins up 61% to $820 daily. Secondhand prices dip 9% from Q3 2024, but fleet renewal (e.g., purchasing a 2018-built 38,000-dwt handysize) bolsters efficiency. FFAs for Q3-Q4 signal $9,000-plus daily—owners hold steady, banking on cargo coverage.

Activity and Coverage

Pacific Basin covers 95% of Q2 supramax days at $12,400, with 37% of H2 at $12,090—strong bookings shield against softening. China’s equipment exports (up 10.8%) and ASEAN trade (up 7.1% to CNY1.71 trillion) lift minor bulk demand. However, iron ore weakness and Colombia’s coal volatility (February exports down 21.1% year-on-year) cap gains. Supramax thrives on flexibility—steel trades optimize port times, dodging 2024’s congestion woes.

External Forces

U.S. sanctions on Iranian oil and Chinese refiners ripple indirectly, tightening tanker markets and nudging bunker costs. Tufton Assets sees bulkers benefiting from trade rerouting—tariffs spur new routes, favoring supramax’s versatility. AI adoption, led by South Korea, streamlines claims and fixtures—supramax sails with cautious optimism, leaning on operational savvy.

⏸️ Handysize Market: Steady Under Strain

Rate Rundown

Handysize bulkers, the fleet’s smallest stalwarts, navigate with poise. Pacific Basin’s handysize earnings hit $10,940 per day, 37% above the Baltic Handysize Index, with Q2 77% covered at $11,390 and H2 25% at $10,150. Secondhand prices fall 9% from Q3 2024, yet fleet upgrades (e.g., buying a 2020-built 40,000-dwt vessel, selling 21-year-old units) keep margins firm. Operating days rise to 6,950, up 300 year-on-year—efficiency drives returns.

Market Moods

China’s Q1 export growth (6.9% to CNY6.13 trillion) and ASEAN trade surge bolster cement and grain flows, but U.S. port fee threats (exempting vessels under 55,000 dwt) shift focus to Japanese-built ships (70% of Pacific Basin’s fleet). Colombia’s coal export swings (4.2 million tonnes in February, up 54.7% month-on-month) disrupt planning—handysize leans on diversified cargoes to weather volatility.

Influencing Factors

Tufton’s Q1 earnings dip to $8 million (from $11.76 million), with a -10.4% NAV return, reflecting rate softness. Yet, the fund eyes tariff-driven rerouting as a boon—handysize’s agility suits reconfigured trades. Rio Tinto’s bauxite boom (15 million tonnes, up 12%) lifts capesize and handysize tonne-miles—handysize holds firm, banking on niche strength.

🌐 What’s Moving It: Trade and Turmoil

Cargo and Supply

Iron ore falters—Rio Tinto’s $RIO (-2,98 %)

$RIO (-3,36 %)

$RIO (-3,09 %) 9% shipment drop and Vale’s $VALE (-3,04 %)

$VALE3 (-2,76 %) 4% output decline shrink capesize cargoes, with China’s Q1 arrivals down 9%. Colombia’s coal cuts (10 million tonnes lost) hit capesize and panamax, though Brazil’s 8% March export rise and China’s equipment trade (up 10.8%) offer lift. Weather (Australian cyclones, Brazilian rains) and blockades (Colombia) disrupt flows—cargo volatility shapes the market’s pulse.

Global Forces

U.S.-China tariffs and U.S. port fees ($18-$33 per net tonne by 2028) spark uncertainty, though exemptions (small vessels, ballast arrivals) soften the blow. U.S. sanctions on Iranian oil and Chinese refiners tighten bunker markets, while Houthi strikes in Yemen add geopolitical heat. Bulkers benefit from rerouting—Tufton sees them outpacing containers—yet trade war fears cloud the horizon.

🌐 Market and Stocks: Value Amid Volatility

Stock Swings

Dry bulk stocks reel under tariff pressures. Tufton’s $SHIP Q1 profit falls to $8 million from $11.76 million, with a -10.4% NAV return as asset values slide. Pacific Basin’s $2343 (-3,4 %) shares trade at a “big discount” to NAV, prompting a $40 million buyback. Secondhand prices drop—capesize down 11%, panamax 12%, supramax and handysize 9% from Q3 2024—yet Q1 rates defy the gloom, hinting at undervaluation.

Investor Perspectives

Analysts view the sell-off as overdone. Firms with lean balance sheets (25% debt-to-asset ratios) trade at trough levels despite firm rates and high newbuild costs. Pacific Basin’s fleet renewal and margin gains (up 61%) position it for resilience, while Tufton bets on rerouting to lift yields. Veson’s Park predicts a 2026 price rebound if trade stabilizes—investors weigh near-term pain against long-term promise.

Sector Outlook

U.S. tariff pauses and scaled-back port fees lift sentiment, but Chinese tariffs threaten consumer costs. Aging fleets (15% over 20 years) and low orderbooks (down 26% in Q1) signal future tightness—2026 looms as a turning point. Stocks lag fundamentals, ripe for a rebound if tariffs ease—bulkers stand poised, undervalued in the storm.

🌐 Outlook: Choppy Yet Hopeful

Fluid Futures

Capesize lingers at $15,000-$18,000 daily—tariffs bite, fundamentals nudge recovery. Panamax at $11,000-$12,000—coal cuts sting, stabilization looms. Supramax holds $12,000-$13,000—coverage shields—resilient. Handysize at $10,000-$11,000—agility endures—steady. AI and rerouting offer upside—2026 glimmers if trade steadies.

Your Call

Will capesize rebound or handysize hold the edge? Drop your take—let’s navigate the seas! 🚢