$CRCL (+0,14 %)

$KSPI (+0,8 %)

$MNDY (+6,11 %)

$CEG (+0,48 %)

$ABX (+0,61 %)

$HIMS (-13,12 %)

$RGTI (-2,31 %)

$BAYN (-0,31 %)

$NCH2 (-2,01 %)

$IOS (+2,52 %)

$MUV2 (+0,65 %)

$BNP (+1,02 %)

$ENR (+0,17 %)

$TKA (+2 %)

$SE (+0,91 %)

$ONON (+1,23 %)

$QBTS (-3,5 %)

$UA (+3,02 %)

$OKLO

$SIE (+1,26 %)

$ALV (+0,57 %)

$BABA (-1,1 %)

$S92 (-2,7 %)

$DTE (+1,54 %)

$700 (+0,42 %)

$NBIS (-8,19 %)

$CSCO (+1,68 %)

$ONDS (-0,86 %)

$KLAR (-0,97 %)

$FIG (+5,17 %)

$NU (-0,6 %)

IOS

IONOS Group

Action

Action

ISIN: DE000A3E00M1

Ticker: IOS

DE000A3E00M1

IOS

Price

Discussion sur IOS

Postes

272Mo·

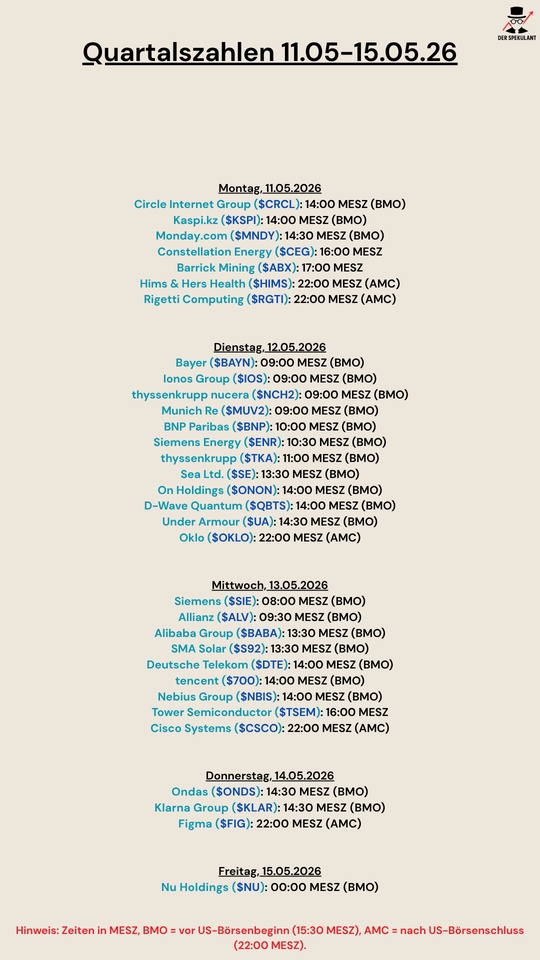

Quarterly figures 11.05-15.05.26

1212

3 CommentairesSebbster@Sebbster

2Mo

•

66

•Afficher la réponse

6Mo·

Share buybacks

I am currently in a buying frenzy and am thinking about which shares I could add to my portfolio.

I have already added 2x $NFLX (+2,5 %) and $NOVO B (+1,42 %)

Further considerations would be:

My current portfolio is geared more towards dividend stocks, but I wouldn't mind buying a few more stocks that are currently doing well:

$ADBE (+5,61 %) , $NOW (+5,56 %) , $IOS (+2,52 %) and $RACE (+0,68 %) .

What are your thoughts on certain stocks.

Have a nice evening :)

1717

8 Commentaires

6Mo

•

55

•

8Mo·

IONOS: Underestimated European cloud champion?

IONOS is developing into the European antithesis of the American cloud giants and impresses with growth and digital sovereignty.

Europe's digital pioneer

IONOS is a German digitalization provider that primarily targets small and medium-sized enterprises (SMEs), the self-employed and organizations. As a reliable partner, the company accompanies its customers from Einstieg to the internet through to a complete cloud infrastructure.

The business model is based on two clearly defined pillars: Web Presence & Productivity and Cloud Solutions.

In the area of Web Presence & Productivity, IONOS offers all the tools required for a professional online presence. This includes domain registration, email and office solutions, web hosting and an AI-based website builder. E-commerce functions, server systems and additional services such as security and optimization tools are also part of the Portfolio.

At the same time, IONOS is driving forward its cloud business. The cloud solutions include public and private clouds, bare-metal servers and fully managed IT infrastructures (managed services). IONOS focuses on high scalability, strong performance and maximum control.

Six million reasons

A key feature of the company is its technological independence: IONOS operates its own infrastructure with over 100,000 servers in around 31 data centers, nine of which it owns. The company also attaches great importance to digital sovereignty: its cloud offerings are 100% GDPR-compliant and hosted in European data centers.

IONOS occupies a special position in the industry: As the European market leader in web hosting with strong cloud momentum, it combines infrastructure expertise with regulatory security. This combination makes the company attractive for customers who value Datenschutztransparency and performance and want to use local providers.

The company has won over more than 6 million customers with this offering.

Convincing figures

IONOS is amazingly successful. In the past three financial years, sales have increased from EUR 1.29 billion to EUR 1.56 billion.

At the same time, profitability has improved.

The operating margin climbed from around 17% to almost 22%. Earnings increased disproportionately from EUR 0.53 to EUR 1.22 per share.

The share price has performed well since Börsengang 2023, making Ionos one of the few success stories among the newcomers to the stock market in recent years.

Is the current correction an opportunity?

The positive development continued in the first nine months. The number of customers increased from 6.32 to 6.53 million.

Sales improved by 6.2% to 980.2 million euros. The adjusted EBITDA The adjusted net profit increased by 20.8% to 368.5 million euros and earnings by 40.6% to 1.35 euros per share.

Net debt was reduced from EUR 855 million to EUR 741 million over the course of the year.

The forecast for the current financial year was confirmed. IONOS is forecasting sales growth of 8% (equivalent to around EUR 1.35 billion), increasing profitability and a 17% rise in EBITDA to EUR 480 million.

In addition, the AdTech business is to be sold. In the first nine months, the division generated EBITDA of EUR 32 million.

It is therefore a division with comparatively low profitability.

Outlook and valuation

"The AdTech business faces exciting challenges and at the same time has great potential. In order to leverage this, we need increasing management attention, which we cannot provide optimally in the long term. In future, we want to concentrate fully on our core business," says Achim Weiß, CEO IONOS Group SE.

According to consensus estimates, earnings are expected to increase by 40% to EUR 1.70 per share this year.

As earnings of EUR 1.35 per share were achieved in the first nine months, this is plausible. There is even a very high probability that expectations will be exceeded.

IONOS therefore has a P/E ratio of 15.6, which is low in relation to the growth rates and the characteristics of the business.

Assuming that the valuation remains at the current level, this results in a 12-month target price of EUR 31.98

Ionos share: Chart from 19.11.2025, price: EUR 26.50 - symbol: IOS | Source: TWS

Ionos has returned to the starting point of the last rally and appears to be attracting interest. If it now manages to rise above EUR 27, the bulls could take control again.

Possible Kursziele are 30 and 32 euros. The next hard Widerstand lies at 36 euros.

However, if the share falls below EUR 25, an extension of the correction towards EUR 23.25 or EUR 21.00 - 21.75 must be expected.

66

9 Commentaires

I like Ionos very much. But I'm glad I didn't get in after the crash. But maybe it's worth getting a foot in the door now.

But I also find $YSN interesting, I think there's a lot of catching up to do here in Germany too

But I also find $YSN interesting, I think there's a lot of catching up to do here in Germany too

•

33

•

8Mo·

IONOS Group: Strong growth and clear realignment in the third quarter of 2025

The IONOS Group SE $IOS (+2,52 %) has had a strong year and impresses with solid figures and a clear strategic direction in its latest quarterly report. In the first nine months of 2025, the company increased its customer base by around 210,000 to 6.53 million. Sales grew by 6.2% to 980.2 million euros, while adjusted EBITDA increased by 20.8% to 368.5 million euros. The 40.6% increase in adjusted earnings per share (EPS) to EUR 1.35 is particularly impressive - a clear sign of increasing profitability.

An important milestone is the decision to sell the AdTech business around Sedo GmbH. This business has increasingly developed into a marketplace for domain trading and traffic monetization but, according to management, no longer fits in with the core business. In future, IONOS intends to focus entirely on the high-growth segments "Web Presence & Productivity" and "Cloud Solutions" - precisely the areas that form the foundation for modern, digital companies.

CEO Achim Weiß emphasized that although the AdTech business has great potential, it requires specialized management, which IONOS cannot guarantee in the long term. The future clearly lies in the cloud and AI sector. With "IONOS Momentum", the company is bundling its existing AI products and planning new applications that will make artificial intelligence easily accessible for entrepreneurs - a step that will further strengthen its competitiveness.

IONOS confirms its forecast for the full year 2025: revenue is expected to increase by around 8%, with an adjusted EBITDA margin of around 35% (after 32.9% in the previous year). EBITDA in the core business is expected to grow by 17% to around EUR 480 million.

I personally find this development particularly exciting, as I will soon be starting my own business and already use IONOS for my own domain, email and website. IONOS offers a simple and reliable solution for founders and small companies in particular to have a professional online presence.

66

4 Commentaires

It's a shame that the share price isn't playing ball. I was also invested this year, but was stopped out again.

•

22

•8Mo·

Quarterly figures 10.11-14.11.25

$MNDY (+6,11 %)

$TSN (+0,82 %)

$OXY (-1,52 %)

$WULF (-4,43 %)

$PLUG (-3,13 %)

$RKLB (-7,39 %)

$CRWV (-8,66 %)

$9984 (-3,94 %)

$IOS (+2,52 %)

$MUV2 (+0,65 %)

$SE (+0,91 %)

$NBIS (-8,19 %)

$RGTI (-2,31 %)

$$BYND (-1,3 %)

$OKLO

$IFX (-2,43 %)

$EOAN (-0,17 %)

$TME (+0,78 %)

$VBK (-3,76 %)

$HDD (-0,95 %)

$ONON (+1,23 %)

$JMIA (+1,54 %)

$MRX (+7,28 %)

$HTG (+4,39 %)

$DTE (+1,54 %)

$R3NK (+0,13 %)

$HLAG (+1,61 %)

$JD (+0,76 %)

$700 (+0,42 %)

$DIS (+2,36 %)

$ENEL (+0,93 %)

$AMAT (-5,15 %)

$NU (-0,6 %)

$ALV (+0,57 %)

$SREN (+1,96 %)

$BAVA (-0,85 %)

1111

3 Commentaires

I'm looking forward to Plug Power on Monday and Allianz on Friday.

•

22

•

8Mo·

Deutsche Telekom invests more than one billion euros in AI factory

Deutsche Telekom $DTE (+1,54 %) wants to enter the construction and operation of data centers for artificial intelligence (AI) on a large scale. Group CEO Timotheus Höttges announced in Berlin the launch of a joint project with the US chip company Nvidia $NVDA (+0,45 %) in which a so-called AI factory is to be built in Munich at a cost of over one billion euros.

"Without AI, you can forget about industry," said Höttges. "Without AI, you can forget about Germany as a business location." The Deutsche Telekom CEO pointed out that only five percent of high-performance AI chips are currently used in Europe, compared to 70 percent in the USA.

Höttges emphasized that the data in the Munich AI cloud should remain entirely in Germany. Only employees from Germany and Europe would be used to handle the data. And the technology comes from Germany and the USA. This means that there are no longer any excuses for German and European companies not to use AI on a large scale.

》Great day for Germany and Europe《

Federal Digital Minister Karsten Wildberger (CDU) spoke of "a great day for Germany and for Europe". "We are celebrating an investment with a signal effect: more than one billion euros for an AI factory with the most modern chips in the world." But this is more than just an AI factory for industry. "It is a signal of new beginnings. A further step on Germany's path to resolutely exploiting the opportunities offered by artificial intelligence."

In Berlin, Nvidia CEO Jensen Huang recalled that the concept of Industry 4.0 was developed in Germany. "Germany had this vision of connecting the digital world with the physical world.

With AI, we can now bring a super version of Industry 4.0 to life. And this is a new era, namely industrial AI." Nvidia is the world's leading provider of high-performance chips that are essential for training and using AI.

Deutsche Telekom is already a provider of conventional cloud services and operates over 180 data centers worldwide. At the same time, the Group cooperates with large platforms such as Google Cloud, Amazon AWS $AMZN (-0,55 %) or Microsoft Azure in the cloud business.

However, Deutsche Telekom's economic success is driven by its core business with telco services in Europe and the business success of its US subsidiary T-Mobile $TMUS (+5,33 %) business success.

》Part of a larger AI strategy《

The AI data center in Munich's Tucherpark is just the start of a larger-scale AI strategy at Deutsche Telekom. The Group hopes to be considered for a major European Union funding program for so-called AI Gigafactories.

The EU defines a gigafactory as a data center with 100,000 or more special AI chips (GPUs) - the facility in Munich will only run with 10,000 GPUs.

In order not to lose touch with the future topic of AI and at the same time remain independent of US companies such as Open AI, Google $GOOGL (+0,42 %)Microsoft $MSFT (+0,87 %) and Meta $META (-0,73 %) Brussels is planning to promote the construction of four to five such large data centers.

The interested parties from Germany were unable to agree on a uniform application. Therefore, in addition to Telekom, the Schwarz Group, which is behind Lidl and Kaufland, the cloud provider Ionos $IOS (+2,52 %) and other consortia.

Federal Research Minister Dorothee Bär (CSU) emphasized the importance of this initiative. At least one AI Gigafactory must come to Germany.

With the Bavarian AI factory, Deutsche Telekom is primarily targeting users in industry.

The first customers include Agile Robots $AGL (+0 %)a leading German high-tech company that specializes in AI-controlled automation solutions and intelligent robotics.

In addition to Nvidia, other cooperation partners include Europe's largest software company SAP $SAP (+6,92 %)Deutsche Bank $DBK (+1,73 %) and the AI provider Perplexity.

1717

9Mo·

Allocation by Irish sale

The idea of further diversifying my portfolio had solidified somewhat in recent weeks. $IREN (-6,06 %) I left it at my self-imposed partial sell target of EUR 55 and started to build up the first positions on Friday. I am sticking to my target of investing around EUR 5k in each position. $IREN (-6,06 %) remains in the portfolio with 500 shares and will (probably) not be touched in the near future. $DEFI (+0,86 %) Now also full with 5,500 shares.

19k liquidity left and will still be invested in top-ups + new shares.

Individual shares are now:

$DSFIR (+1 %) possibly increase

$MUM (+0,86 %) possibly increase

$FSLR (-1,16 %) Increase if necessary

$NICE Increase if necessary

Does anyone else have an idea for a share, possibly also from the German-speaking region? The Asian region would also be very interesting, although I am looking a little at $1810 (+0 %) look at.

vg and have a nice WE

Micha

77

5 Commentaires

•

11

•

10Mo·

After the Oracle rally: you need to know these cloud favorites

Hello dear Getquin Community,

After $ORCL (-2 %) Oracle caused quite a stir after the last quarterly figures and the market reacted extremely positively with a 40 percent increase in the share price, so much so that CEO Larry Ellison briefly became the richest person in the world overnight, I wanted to unravel the magic and find out exactly which division caused this tremor.

The answer is Cloud Infrastructure, or OCI for short. In this area, the demand for data centers for artificial intelligence has exploded, which has brought Oracle long-term orders worth 455 billion US dollars. However, it is not only Oracle that is benefiting, but also other hyperscalers, regional challengers and, above all, the so-called shovel manufacturers that provide the basic infrastructure.

I have taken the trouble to look for potential competitors and up-and-coming challengers so that you have a complete overview of this sector. I have divided the whole thing into the following segments: 🌍 Big players (hyperscalers), 💡 Hidden champions (selection by region), ⚒️ Shovel manufacturers (infrastructure suppliers) and, as always, my favorite.

If I have overlooked any important aspects or a classification was not entirely precise, I look forward to your comments and exciting additions. Together we can understand this topic even better and learn from each other.

Feel free to leave a 👍. I wish you every success with your investments 🚀

🌍 Big Player (Hyperscaler)

Amazon Web Services - $AMZN (-0,55 %) (USA, Nasdaq) → World market leader with >30 % market share, huge data centers & own AI chips (Trainium, Inferentia)

Microsoft Azure - $MSFT (+0,87 %) (USA, Nasdaq) → second largest provider, strong AI focus through OpenAI partnership

Google Cloud - $GOOGL (+0,42 %) (USA, Nasdaq) → third largest provider, specialized in AI workloads & big data

Oracle Cloud Infrastructure (OCI) - $ORCL (-2 %) (USA, NYSE) → Number 4 worldwide, currently fastest growth (+70-80 %), RPO USD 455 bn

Alibaba Cloud - $BABA (-1,1 %) , $9988 (-1,24 %) (China, NYSE/HKEX) → Market leader in Asia, complete cloud suite from IaaS to AI

Favorite: Oracle - $ORCL (-2 %)

Oracle impresses with its cloud infrastructure OCI, which recently collected orders worth 455 billion US dollars. The moat lies in the close integration of the database business and cloud services as well as the multi-cloud partnerships with Microsoft and Google. The compounder property is the result of long-term contracts and economies of scale in data center construction.

Alternative favorite: Alibaba Cloud - $BABA (-1,1 %) , $9988 (-1,24 %)

Alibaba is number one in Asia and number four worldwide. The moat lies in the close integration with Alibaba's e-commerce and fintech ecosystem. The compounder property stems from the enormous growth in emerging markets and the increasing demand for cloud services in China. While the stock is valued significantly cheaper than Oracle, there are geopolitical and regulatory risks.

💡 Hidden champions (selection by region)

🇪🇺 Europe

OVHcloud - $OVH (+2,39 %) PA (France) → largest European cloud provider, GDPR- and Gaia-X-focused

Scaleway - private (France, part of the Iliad Group) → Developer and AI cloud platform

T-Systems - part of $DTE (+1,54 %) DE (Deutsche Telekom, Germany) → Hybrid & Sovereign Cloud for Public Sector

IONOS - $IOS (+2,52 %) DE (Germany, Xetra)

Largest European web hosting and SME cloud provider. Burggraben: strong brand and high customer loyalty in the SME sector.

Aruba Cloud - private (Italy) → regionally strong in SMEs & hosting

Outscale - private (France, subsidiary of Dassault $DSY.PA) → Industrial Cloud & Simulation

Favorite: OVHcloud - $OVH (+2,39 %)

Burggraben: strong position as a GDPR-compliant sovereign cloud with Gaia-X. Compounder: increasing trust from authorities and companies ensures growing recurring revenues.

🇨🇳 China

Baidu AI Cloud - part of $BIDU (-0,95 %) , $9888 (-1 %) (Nasdaq, China/USA) → AI workloads, autonomous driving, language models

JD Cloud - part of $JD (+0,76 %) , $9618 (+0,79 %) (Nasdaq, China/USA) → Cloud for e-commerce & retail

Kingsoft Cloud - $KC (-0,89 %) , $3896 (-1,32 %) (Nasdaq, China/USA) → Gaming, streaming and app cloud

China Telecom Cloud - part of $728 HK (HKEX) → Infrastructure cloud, state-supported

China Mobile Cloud - part of $941 HK (HKEX) → 5G edge cloud with telecom backbone

Favorite: Kingsoft Cloud - $KC (-0,89 %) , $3896 (-1,32 %)

Moat: Specializing in gaming, streaming and mobile apps with deep integrations into ecosystems. Compounder: benefits from China's growing online consumption and strong embedding in the Tencent environment.

🇯🇵 Japan

NTT Communications - part of $9432 (+1,25 %) T (Tokyo) → Enterprise cloud with global network

NEC Cloud - $6701 (+2,43 %) T (Tokyo) → Government & security solutions

Fujitsu Cloud K5 - $6702 (+2,77 %) T (Tokyo) → Hybrid cloud for large companies

Rakuten Symphony Cloud - part of $4755 (+0,06 %) T (Tokyo) → 5G & telecom cloud

IIJ Cloud - $3774 (+1,38 %) T (Tokyo) → Cloud pioneer for enterprise IT

Favorite: NTT - $9432 (+1,25 %)

Moat: global telecom backbone and huge enterprise customer base. Compounder: expansion of data centers in Asia and Europe with stable recurring revenues.

🇮🇳 India

Reliance Jio Cloud - part of $RELIANCE NS (NSE India) → Telecom Cloud, partnership with Azure

Tata Communications IZO - $TATACOMM NS (NSE India) → Hybrid cloud & global backbone

Infosys Cobalt - $INFY (NYSE/NSE India) → Cloud migration platform & consulting

HCLTech Cloud - $HCLTECH NS (NSE India) → AI-powered hybrid cloud

Wipro Cloud Studio - $WIPRO NS (NSE India) → MultiCloud service provider

Favorite: Tata Communications - $TATACOMM

Moat: global fiber optic network and deep networking in hybrid cloud. Compounder: growing international expansion and increasing demand for multi-cloud solutions.

🌏 Asia / Oceania

Naver Cloud - part of $035420 KQ (Korea KOSDAQ) → AI & gaming cloud

Samsung SDS Cloud - $018260 , $SMSN (-5,92 %) KQ (Korea KOSDAQ) → Enterprise & IoT Cloud

KT Cloud - part of $030200 KQ (Korea KOSDAQ) → Telecom & Edge Cloud with 5G

Telstra Cloud - $TLS (-0,13 %) AX (Australia) → Telecom Cloud, Asia-Pacific focus

Macquarie Telecom Cloud - $MAQ AX (Australia) → Public Sector & Compliance

Favorite: Naver Cloud - $035420

Moat: strong integration of AI and gaming in Korea. Compounder: rapid scaling due to growing demand for AI and ML applications.

🌍 Latin America

UOL Diveo (Compasso UOL) - private (Brazil) → Cloud + Managed Services

Tivit Cloud - private (Brazil) → MultiCloud for industry & banks

Locaweb Cloud - $LWSA3 SA (Brazil) → SME Hosting & Cloud

Claro Cloud - part of $AMX (+1,32 %) (Mexico, NYSE/HKEX) → Telecom Cloud in Latin America

DesireCloud - private (Chile/Peru) → Local provider for companies

Favorite: Locaweb - $LWSA3

moat: Market leader for SME cloud and hosting in Brazil. Compounder: enormous scalability through the digitalization of small and medium-sized enterprises throughout Latin America.

🇨🇦 Canada

OVHcloud Canada - part of $OVH (+2,39 %) PA (France) → Data centers for North America

SherWeb - private (Quebec) → Cloud and MSP services for SMEs

HostPapa - private (Canada) → SME cloud solutions

Canadian Web Hosting - private (Canada) → Cloud & hosting with a focus on data protection

Beanfield Cloud - private (Toronto) → Cloud combined with fiber optic infrastructure

Favorite: SherWeb - private

Moat: close ties to SMEs via managed services. Compounder: fast-growing cloud ecosystem for small businesses in North America, high customer loyalty.

⚒️ Blade manufacturers (infrastructure suppliers)

🖥️ Semiconductors & Chips

Nvidia - $NVDA (+0,45 %) (USA, Nasdaq) → GPUs for AI training & cloud

AMD - $AMD (-3,77 %) (USA, Nasdaq) → CPUs/GPUs for Data Center

Intel - $INTC (-12,38 %) (USA, Nasdaq) → Server CPUs & AI accelerators (Gaudi)

TSMC - $TSM (-2,26 %) (Taiwan, NYSE/TWSE) → largest chip manufacturer, produces for NVIDIA/AMD

Samsung Electronics - $SMSN (-5,92 %) KQ (Korea) → Memory, foundry, GPUs/CPUs

Favorite: Nvidia - $NVDA (+0,45 %)

Moat: near monopoly in high-end GPUs for AI. Compounder: Ecosystem and network effects through CUDA and developer community.

📦 Data center hardware & servers

Supermicro - $SMCI (-1,78 %) (USA, Nasdaq) → GPU clusters & AI servers

Dell Technologies - $DELL (+1,16 %) (USA, NYSE) → Enterprise Servers & Storage

Hewlett Packard Enterprise - $HPE (+0,78 %) (USA, NYSE) → Hybrid Cloud & Edge

Inspur - private (China) → AI & Cloud Server

Lenovo - $LNVGY (-0,46 %) (China/ADR) → HPC and AI servers

Favorite: Supermicro - $SMCI (-1,78 %)

Moat: Specialization in GPU clusters and AI servers. Compounder: benefits from every expansion of the hyperscalers, extremely high scalability.

⚡ Memory & network chips

Micron - $MU (-6,31 %) (USA, Nasdaq) → DRAM & HBM memory

SK Hynix - $HY9H (-8 %) KQ (Korea) → Memory chips, HBM for NVIDIA

Broadcom - $AVGO (-2,25 %) (USA, Nasdaq) → Network Chips & Switches

Marvell - $MRVL (-6,67 %) (USA, Nasdaq) → Network & 5G chips

ASE Technology - $ASX (-5,76 %) (Taiwan, NYSE) → Packaging for high-end chips

Favorite: Broadcom - $AVGO (-2,25 %)

Moat: deep roots in network infrastructure of hyperscalers. Compounder: benefits from rising demand for switches and custom chips for the cloud.

🏭 Data centers / colocation

Equinix - $EQIX (+6,44 %) (USA, Nasdaq) → largest colocation provider worldwide

Digital Realty - $DLR (+10,87 %) (USA, NYSE) → Data centers worldwide, strong in Europe/USA

China Telecom DC - part of $728 HK (HKEX) → Data center infrastructure in China

NTT Data Centers - part of $9432 (+1,25 %) T (Tokyo) → Data centers in Asia/Europe

NEXTDC - $NXT (-3,5 %) AX (Australia) → Growing data centers in the APAC region

Favorite: Equinix - $EQIX (+6,44 %)

Moat: global networking and extremely high switching costs for customers. Compounder: continuous expansion and cross-selling potential through platform structure.

🔋 Energy & cooling

Schneider Electric - $SU (+0,22 %) PA (France, Euronext) → Power & Cooling for Data Center

ABB - $ABBN (-0,15 %) (Switzerland, SIX/NYSE ADR) → Energy & Automation

Siemens Energy - $ENR (+0,17 %) (Germany, Xetra) → Power Grids & Data Center Technology

Vertiv - $VRT (-2,54 %) (USA, NYSE) → Cooling, Racks & UPSs

Eaton - $ETN (-1,69 %) (Ireland/USA, NYSE) → Power Management

Favorite: Schneider Electric - $SU (+0,22 %)

Burggraben: market-leading energy and cooling systems for data centers. Compounder: long-term growth due to increasing demand for efficient data centers.

🌐 Network & Connectivity

Cisco - $CSCO (+1,68 %) (USA, Nasdaq) → Router & Network Hardware

Arista Networks - $ANET (-1,84 %) (USA, NYSE) → High-speed switches for hyperscalers

Juniper Networks - Acquisition by $HPE (+0,78 %) Hewlett Packard HP (USA, NYSE) → Routing & Network Security

Ciena - $CIEN (-4,25 %) (USA, NYSE) → Fiber Optics & Optical Networks

Nokia - $NOK (-5,81 %) (Finland, NYSE/Helsinki) → 5G & Core Networks

Favorite: Arista Networks - $ANET (-1,84 %)

Moat: technological leadership in high-speed switches in hyperscaler data centers. Compounder: enormous growth opportunities due to exponential data traffic in AI workloads.

✨ Takeaway

The Oracle quake shows: Cloud & AI are the growth drivers of the coming years. While hyperscalers are in the spotlight, hidden champions are growing in their niches in the background and blade manufacturers are making money from every expansion of the infrastructure.

👉 Question for you: Do you prefer to focus on hyperscalers in your strategy? hyperscalersthe hidden champions or directly on the shovel manufacturers?

I look forward to your opinions!

Source: own analysis

Image - Image credit: Getty Images

6767

22 CommentairesSo many interesting suggestions 👍🏼

•

77

•

10Mo·

Implementation of my portfolio reallocation 📈 (give me feedback) 💶😁

Hello everyone,

Since a lot has happened in the last few days and weeks, I would like to give you an insight into how far my portfolio has changed in terms of growth and returns. First of all, the FTSE All World has been thrown out completely, as have the stable value stocks such as Airbus and Telekom. My "new" portfolio has so far included the following:

Position (weighting in the portfolio in %) Return to date in %

$BTC (+0,02 %) (13%)

Return to date +-0

$IREN (-6,06 %) (11,2%)

Return so far approx. +30

$RKLB (-7,39 %) (9,46%)

Yield yesterday still at +15% today at just under +4% 🤪

$PNG (-2,81 %) (9,4%)

Yield so far +15%

$TTR1 (+0,52 %) (8,67%)

Yield to date +-0

$IOS (+2,52 %) (8,55%)

Return so far approx +5%

$ASTS (-4,55 %) (8,54%)

Return to date approx +5%

$ZAL (+0,59 %) (7,35%)

Return so far approx +11%

$IPX (-3,2 %) (7,27%)

Return so far -5%

Warrants (only for those who are interested)

(sorted by weighting)

Long on Hensoldt MM2TXJ (+16%)

Long on silver MK81Z6 (+84%)

Short on Puma DU1SAE (+6%)

Inline OS on Zalando UG71Z8 (+93%)

Inline OS on Thyssenkrupp UG81HF (+80%)

Inline OS on Telekom (since today) PJ711H (-1%)

Discount Tut on Palantir VK38YE (-34%)

In addition, I now have a savings plan with 200 euros per month on Bitcoin $SOFI (-0,44 %) Tech, as well as 100 euros each on $VSAT (-2,46 %) and $BNTX (-2,38 %) (for the next pandemic, cancer therapy, and because of the thick cash cushion).

I think I've covered the areas of data centers and digitalization, as well as space and outer space. What I'm still missing is a convincing stock in the critical commodities sector (I have Iperionx, but I'm still looking for a candidate that convinces me)...

I'm up about 8% for the week and see this as a very small confirmation of the transformation in the portfolio, even though I know that these stocks are naturally more susceptible to a bear market xD

I'm not sure whether I'll be able to keep up the savings rates because I have to take my driver's license exams soon and I'm still doing my A-levels. And as I only work on a part-time basis, I don't have that much money available yet. My deposit is currently around 9900 euros and my short-term goal is to have enough money by the end of 2026 or early 2027 to buy my dream car, a Golf 7. 🙈

Please let me know what you think and whether you would do the same as me...

And if anyone else has a stock that would fit into my portfolio strategy, I would of course also be delighted...

HG Small investors ✌️🤝

1212

9 Commentaires

In my view, there are a few promising stocks among them. However, the valuations of the stocks you have chosen are very close to astronomical in my view.

Personally, I wouldn't touch stocks like Zalando with pliers. In the case of $ASTS, I honestly don't have the imagination to justify the valuation, they almost exclusively offer mobile satellites (most of which don't belong to AST itself) and it currently looks like they are steadily losing market share rather than gaining it. I don't have the research background for $VSAT. Edit: Why did you choose both AST and ViaSat? After brief research, both have the same focus, namely mobile communications on the move🤔.

In the area of mining/HPC/colocation, my choice no longer fell on $IREN after quite intensive research, as the valuation is currently too high for me in relation to a possible big deal.

In the area of critical raw materials, the question is what kind of exposure you are looking for suchst🤷🏼♂️. Titanium is currently in the portfolio, okay. Rare earths in general? Lithium in particular? Something completely different? In my view, you're being rather vague at the moment.

And the stocks you have chosen are not "more susceptible" to a bear market, but will then probably be completely slaughtered😅🫣. In my view, the valuations are far too inflated for that.

Personally, I wouldn't touch stocks like Zalando with pliers. In the case of $ASTS, I honestly don't have the imagination to justify the valuation, they almost exclusively offer mobile satellites (most of which don't belong to AST itself) and it currently looks like they are steadily losing market share rather than gaining it. I don't have the research background for $VSAT. Edit: Why did you choose both AST and ViaSat? After brief research, both have the same focus, namely mobile communications on the move🤔.

In the area of mining/HPC/colocation, my choice no longer fell on $IREN after quite intensive research, as the valuation is currently too high for me in relation to a possible big deal.

In the area of critical raw materials, the question is what kind of exposure you are looking for suchst🤷🏼♂️. Titanium is currently in the portfolio, okay. Rare earths in general? Lithium in particular? Something completely different? In my view, you're being rather vague at the moment.

And the stocks you have chosen are not "more susceptible" to a bear market, but will then probably be completely slaughtered😅🫣. In my view, the valuations are far too inflated for that.

•

1111

•10Mo·

Adjustment of the investment strategy

Good morning to all Getquiners,

Today I would like to share with you my train of thought and the associated changes in my portfolio...

What my portfolio looked like:

Predominance of quality stocks like Siemens, Airbus, Telekom etc.

Small part in the FTSE World

With a small weighting in warrants and Bitcoin

Now that I have studied the stock market in depth, I have decided at my age (not 20) to invest more in faster-growing and smaller companies and more in Bitcoin in order to increase the return to 20%+...

My portfolio in the future, partly already today (currently in the process xD):

Predominantly riskier stocks with higher growth rates such as $RKLB (-7,39 %) , $IOS (+2,52 %) ...

Increase of the $BTC (+0,02 %) Bitcoin position to approx. 30% of the portfolio...

Approx. 15% of the portfolio in warrants...

If you have a few more stocks that fit into my new investment strategy, I would appreciate your suggestions freuen✌️:

I currently have on the WL

$TTR1 (+0,52 %) , $VSAT (-2,46 %) , $ENR (+0,17 %) , $VWS (-1,31 %) , $GEN (+3,13 %) , ($GOOGL (+0,42 %) )

Target:

20%+ p.a. & save for a future house purchase

Anyone who enjoys it can also see my portfolio with the current weightings and realize that I have already implemented some things 😁 The OS are not always up to date because I always have to enter them manually...

Could you let me know what you think of this approach?

HG Kleinanleger 😊

55

9 Commentaires

10Mo

20%pa is ambitious, but achievable.

You have presented a current selection from your asset universe. Of course, this is not enough to achieve your goal. You need defined entry and exit criteria.

The central question remains: what is your strategy?

Value, momentum, mean reversion, short/medium-term trading...? What do the backtests say?

Without answers to these questions, the goal remains a pipe dream. 🤷

You have presented a current selection from your asset universe. Of course, this is not enough to achieve your goal. You need defined entry and exit criteria.

The central question remains: what is your strategy?

Value, momentum, mean reversion, short/medium-term trading...? What do the backtests say?

Without answers to these questions, the goal remains a pipe dream. 🤷

•

77

•Titres populaires

Meilleurs créateurs cette semaine

Données en temps réel par LSX · Données financières de FactSet