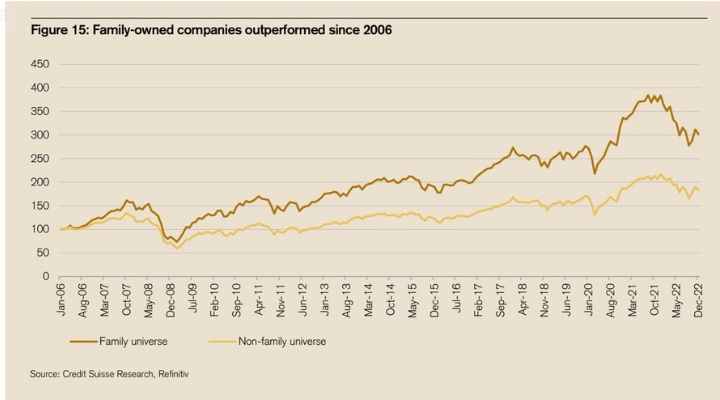

Take a look at the attached chart. There’s a popular macro theory that buying family-controlled businesses is a cheat code to beat the market over decades (+250% vs +50%).

The logic is sound: families think long-term and ignore the quarterly earnings rat race.

But does a great family business automatically make a great dividend stock today?

I ran 5 of the biggest Canadian family empires (Desmarais, Weston, Thomson, etc.) through the DividendQuad engine to separate the business quality from the current entry point.

The math is brutal:

🟢 $QBR.B (-0,25 %)

(Péladeau) - OPTIMAL

Quality: 85 | Opportunity: 75

The only one flashing green. Strong quality and valuation, but the dividend yield is just 2.45% (a bit low for strict income targets).

🟣 $TRI (+0,38 %)

(Thomson) - WATCH

Quality: 85 | Opportunity: 20

An incredible data monopoly. However, at a 37x P/E, you are paying pure AI hype prices right now. Zero margin of safety.

🟣 $POW (+0,22 %)

(Desmarais) - WATCH

Quality: 75 | Opportunity: 35

A solid financial holding company, but the algorithm flags this as a terrible entry point valuation-wise.

🟡$FFH (-0,44 %)

(Watsa / Fairfax - CAUTION

The "Canadian Berkshire". Prem Watsa is a genius for total return, but it is useless for a dividend income portfolio at a 0.6% yield.

🔴$L (+0,49 %)

(Weston/Loblaw) - BELOW THRESHOLD

Quality: 40 | Opportunity: 25

Trading at 29x P/E with a 0.9% yield, plus the system penalizes its history of dividend cuts (related to the historical bread pricing scandal). The math says to stay away.

The Takeaway

Great families build great businesses. But as a dividend investor, if you overpay for quality or ignore yield requirements, you are subsidizing their wealth instead of building your own. Always run the numbers objectively.

Does anyone hold these in their portfolio? How much weight do you give to "family control" when buying a stock?