Adjusted Net Income: $193M-$196M (Prev. $205M-$208M) ❌

Adjusted EPS: $3.27-$3.32 (Prev. $3.47-$3.53) ❌

Adjusted Effective Tax Rate: 19-20% (No Change) ❌

Other Key Metrics:

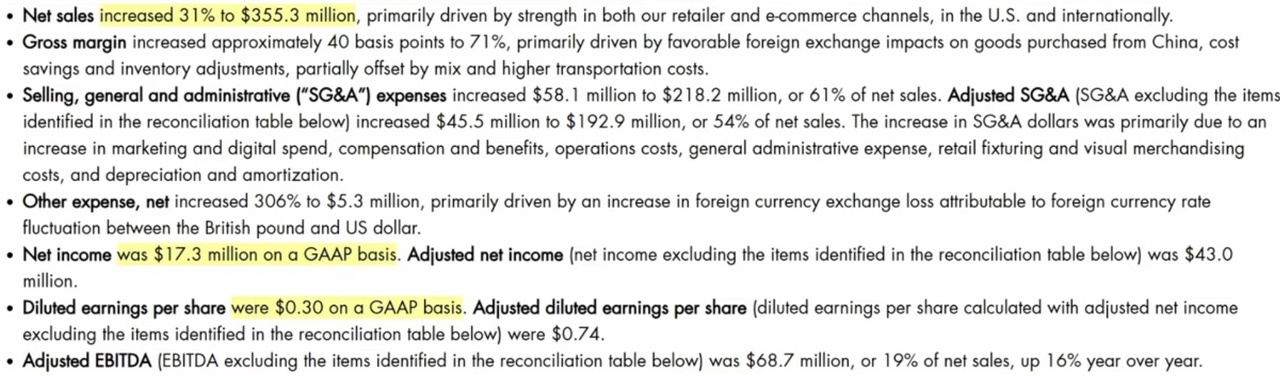

Gross Margin: 71% (Est. 71.15%) ; UP +40 bps YoY

SG&A Expenses: $218.2M (Est. $175.43M) ; UP +36.3% YoY

Adjusted SG&A: $192.9M (54% of net sales)

Net Income: $17.3M (Est. $44M)

Adjusted Net Income: $43M

Adjusted EPS: $0.74

Adjusted EBITDA: $68.7M (Est. $72.57M) ; UP +16% YoY

Comment from the CEO and CFO:

CEO Tarang Amin: "We continue to gain market share, with net revenue growth of 31% and market share gains of 220 basis points in the US. We see significant new territory opportunities in digital, color cosmetics, skincare and international markets."

CFO Mandy Fields: "Given the weaker than expected trends in January, we are taking a cautious approach and lowering our outlook for the 2025 financial year."

@Aktienhauptmeister well, 5% up or down doesn't matter. I didn't want to be annoyed afterwards if I missed the opportunity, doesn't mean it can't fall further, but I think it's already too attractive. If the market falls, we may see even lower prices, but otherwise I think we will slowly move upwards. It's already pretty bombed out. Had to liquidate $GOOG, sell part of $NU and sell $IREN. It hurts too, but I wanted to lower my entry even further. It's not a short-term trade for me. But I hope I can get back into $IREN without it running away from me.

@BamBamInvest Wouldn’t it have been better to wait for IREN with its potential to grow to $15 or even $26? As for NU Holdings, reducing the position seems reasonable, but probably at a slightly higher price and then re-entering on a pullback.

I see that the decision was difficult, and technically, it was the right move since the companies that had shown good growth in the portfolio were reduced or closed.

@wrong_strategy that would certainly have been better 😁, but I was too impatient and didn't really expect such a negative reaction. It's always easier with hindsight. ✌️

@Aktienhauptmeister yes exactly, a partial sell-off would have brought me too little to double. From here, I see more price potential for $ELF over the next 3 years than for $GOOG. Perhaps $GOOG will come back a little more, in which case I might switch.

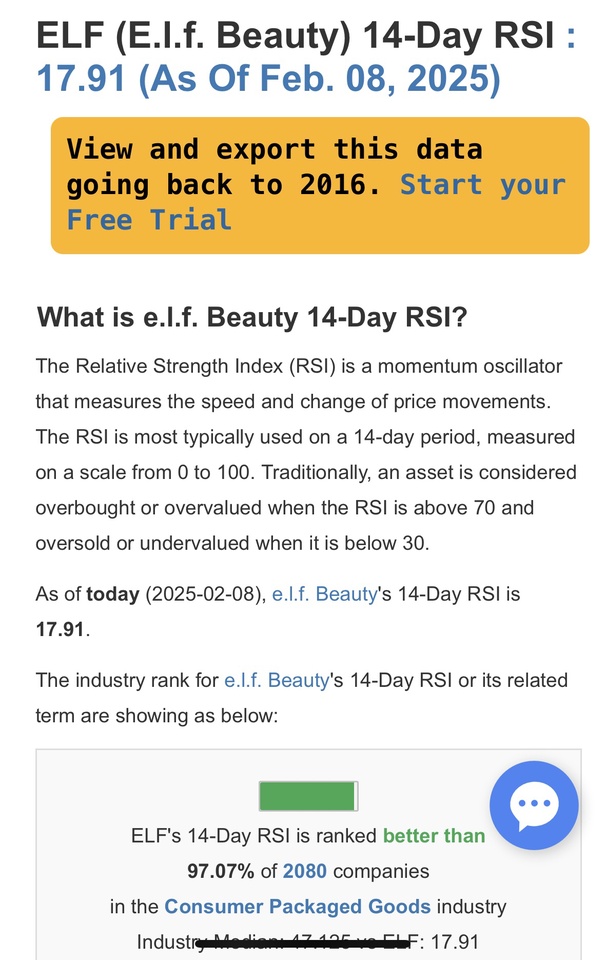

ELF Beauty's price drop and oversold RSI might appear attractive, but several concerns warrant caution. The missed revenue target raises questions about the company's performance and future prospects. The strongly negative volume flow suggests continued selling pressure. While the RSI is low, it's not a reliable indicator on its own; oversold conditions can persist. Furthermore, there's no clear sign of a trend reversal. Before considering a buy, investigate the reasons behind the missed revenue, assess the competitive landscape, and consider the overall market context. Don't be lured by a low price without thorough due diligence.