The market doesn't like Sanofi $SAN (+0,19 %) right now. Between the fears of the Dupixent patent cliff, weak pipeline results, margin drops from their R&D pivot, and political fears in the US healthcare sector, the stock has taken a serious beating.

But when we ran Sanofi through our algorithm in this week's batch, the cold math told a very different story.

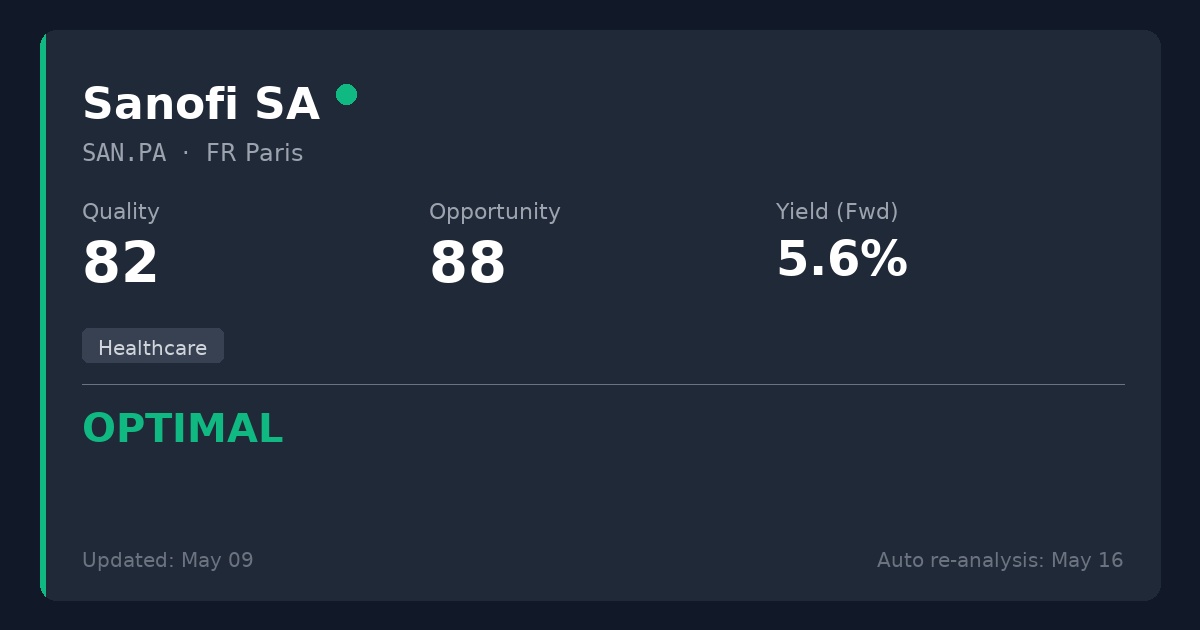

Quadrant: 🟢 OPTIMAL

Quality Score: 82.0/100

Opportunity Score: 88.0/100

Why the engine is flagging this as a deep discount:

* The 99% payout ratio on basic screeners is a lie. This is just accounting noise. The actual cash flow payout ratio (FCF) is a very conservative 44.4%. The 5.6% dividend is strictly protected.

* The balance sheet is a fortress. Net Debt to EBITDA is just 1.33x, well below our 3.0x danger limit. They have the financial flexibility to execute their R&D pivot.

* It trades at an exceptional P/E of 8.69x.

The algorithm's verdict: The market is pricing Sanofi as if its entire pipeline will fail. Now that the Opella consumer health sale is closed and Sanofi is a pure-play biopharma, there is obvious execution risk. But their core cash generation remains completely intact. Top business at a great price.