Hello my dears,

what would be your theory why the gold price is falling today?

In my opinion, it could be related to the rising oil price, which is causing inflation to rise.

that means:

Uncertainty about Fed monetary policy Market participants are unsure whether the US Federal Reserve will really ease further. Rising or less sharply falling interest rates make gold less attractive.

I was able to make a few reflections while cycling today. And the fresh air put me in a buying mood.

And what does all this have to do with the price of gold?

Maybe because the sun gave me golden thoughts. Like :

How great the K92 numbers were, and on today's sunny day it might be a nice thing to use today's DIP to buy a small tranche.

My dears, what do you think of my purchase?

Maybe riding a road bike in the sun is my 🔮.

K92 Mining owns the high-grade, low-cost Kainantu gold mine in the Eastern Highlands of Papua New Guinea. The mine is located on an approximately 830 km² property in a Tier 1 region and has undergone significant expansions. The Stage 2 expansion (Q3 2020) doubled throughput to 400 ktpa, followed by Stage 2A (Q2 2023) which increased capacity by 25% to 500 ktpa (now capable of >600 ktpa). In December 2022, K92 approved its largest expansions - Stages 3 and 4 to 1.2 mtpa and 1.8 mtpa respectively. The updated Definitive Feasibility Study of October 2024 envisages production of over 300 koz AuEq per annum at a low AISC of US$920/oz for Stage 3. The Stage 4 expansion is targeting over 400 koz AuEq per year. Construction of the Stage 3 process plant is complete and was completed under budget, with first production in October 2025. The official inauguration of the plant shortly thereafter marked a major operational milestone for K92. Drilling continues apace, with up to 12 rigs targeting further growth.

K92 Mining Inc. profit increases for the full year

02.03.2026,

K92 Mining Inc. Gewinn steigt im gesamten Jahr

High-quality and fast-growing gold producer

Potential catalysts

- " Kora & Judd drilling (ongoing)

- " Kora South & Judd South drilling (ongoing)

- " Porphyry exploration (ongoing)

- " Arakompa and Maniape drilling (ongoing)

- " Wera drilling (ongoing)

- " Stage 3 ramp-up and production milestones (ongoing)

WHY INVEST?

- Rapid production growth.

The new, state-of-the-art Stage 3 expansion process plant with a capacity of 1.2 million tpa was completed and the official opening took place on October 16, 2025. The updated DFS Stage 3 expansion provides for a production rate of over 300 koz AuEq per year. The Stage 4 expansion is planned to reach over 400 koz AuEq per year.

- ~830 km² land package in 'elephant country'.

Large number of priority vein and porphyry targets identified and expansion to up to 12 drill rigs on site.

- High-grade, low-cost mine.

2024 grade: 11.5 g/t AuEq (10.7 g/t Au, 0.55% Cu, 15.2 g/t Ag) 2024 AISC: $1,066/oz Au.

- Experienced team with proven track record.

International expertise in mining, exploration and finance.

- Significant resource growth.

+579% in M&I and +1,114% estimated growth from end of 2017 to Q4 2023 with extensive potential for resource growth nearby through strike and depth extensions and nearby priority vein targets.

- Socially responsible mining.

Underground mining with low environmental impact; ~92% of national workforce in PNG. Strong focus on environment, community and corporate responsibility.

Kainantu mine

K92 Mining is focused on the operation and expansion of the Kainantu Gold Mine, located in the Eastern Highlands Province, Papua New Guinea. Since acquiring the project from Barrick Gold in 2014 and restarting in late 2016, K92 has turned Kainantu into a fast-growing producer and mineral resource company. Production has also been low cost, which is testament to the high grade, continuity, solid thickness, geotechnical and metallurgical characteristics of the deposit. The transformation was driven by a series of discoveries in the nearby infrastructure.

Kainantu-Mine: Hochwertige Goldproduktion | K92 Mining Inc.

The Blue Lake Porphyry Project is a significant gold-copper discovery in K92 Mining's highly attractive Kainantu region of Papua New Guinea. Located just 4 km southwest of the high-grade, producing Kainantu Gold Mine, Blue Lake represents a large-scale, well mineralized porphyry system with significant growth potential. The maiden Inferred Resource of 14.6 Moz AuEq makes it one of the most significant porphyry discoveries in Papua New Guinea and one of the largest known mineralized porphyries in the country.

Führendes Wachstum des Goldbergbaus in Papua-Neuguinea | K92 Mining Inc.

K92 is not a diversified multi-commodity producerbut a focused gold gold producer with copper and silver by-products. This makes the company heavily dependent on the gold price, but at the same time they benefit from the additional metal streams to reduce costs.

Metal AuEq (oz) Share

Gold 139.123 93,0 %

Copper 9.853 6,6 %

Silver 1.776 1,2 %

Total 149,515 100 %

K92 is a high-grade gold producer with extremely low costs.

Gold dominates the valuation, copper stabilizes the costs.

The Stage 3 expansion could lift production towards 250-300k oz AuEq - with costs remaining low.

K92 Mining

Region: Papua New Guinea

Mine type: High-grade underground mine

Character: Extremely high grades, low costs, strong growth

Gold grade: 10-15 g/t AuEq (world-class grades, benchmark in the sector)

Cost structure (AISC)

800-1,000 USD/oz (very low, copper byproducts help)

Growth potential

Growth driver: Stage 3 expansion → 250-300k oz

Valuation: Very high

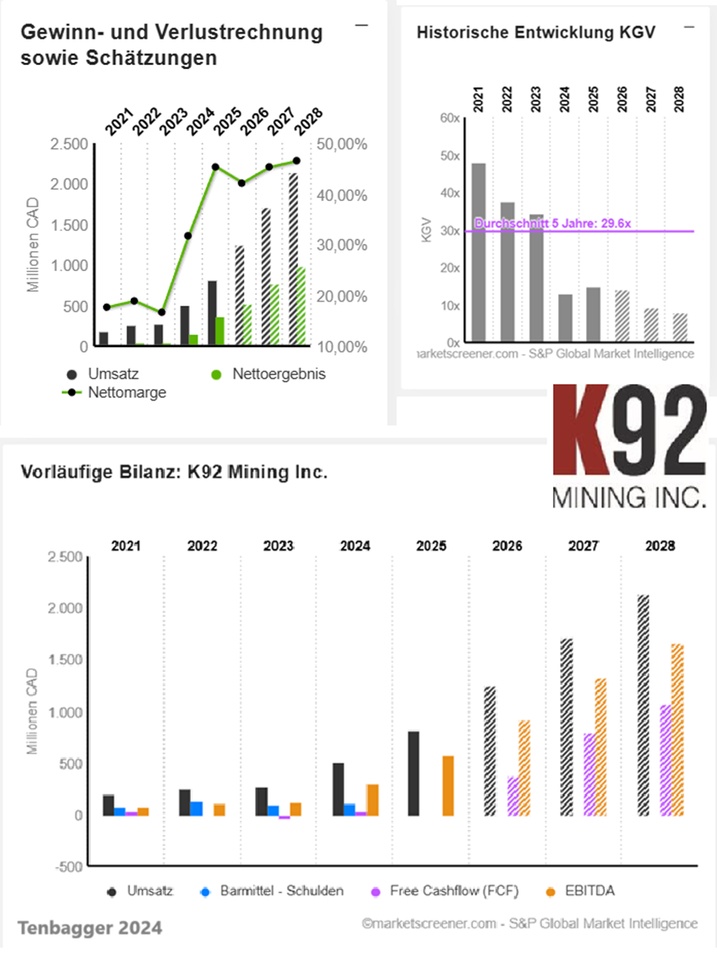

Sales and earnings performance of K92 Mining

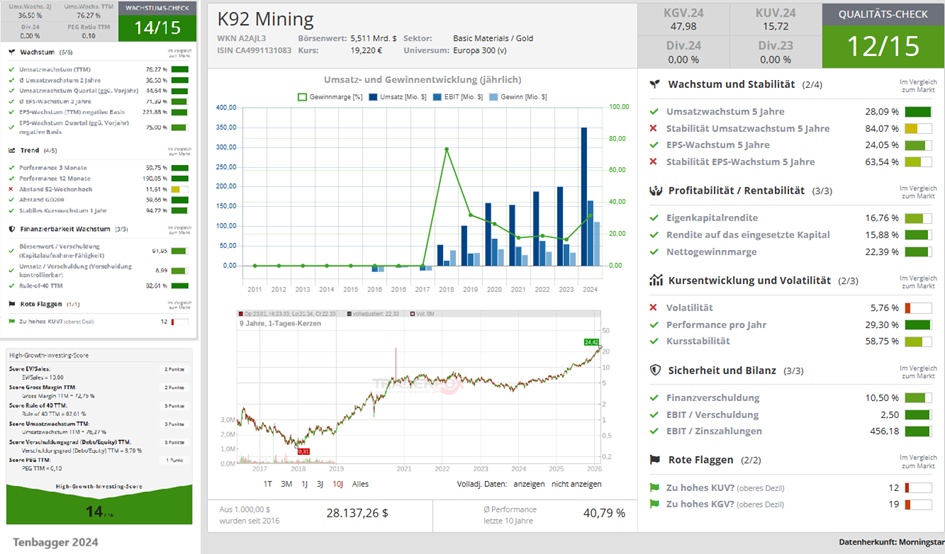

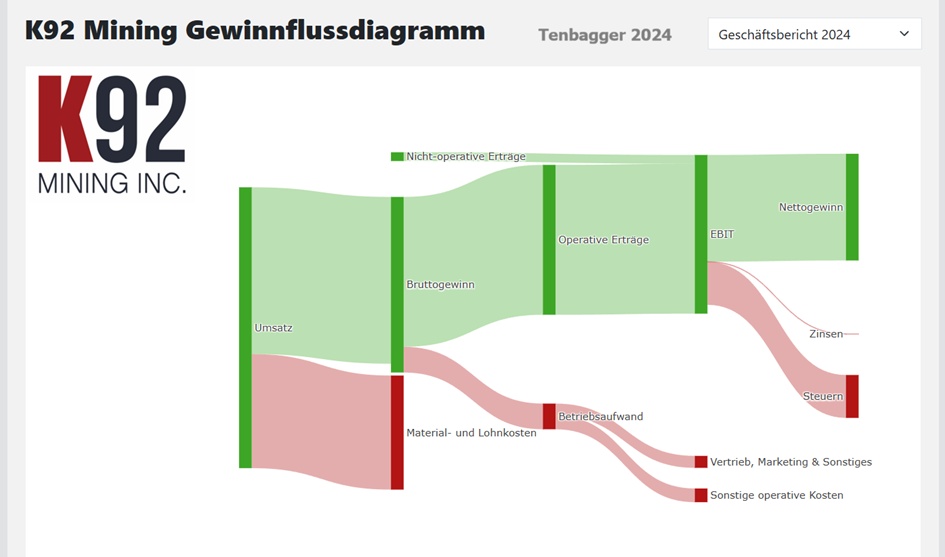

In the last financial year, the revenue of K92 Mining Inc. increased by 75.1% from USD 200.3 million to USD 350.6 million. Profit rose by 235.4% from USD 33.2 million to USD 111.2 million. The net profit margin was thus 31.7% compared to 16.6% in the previous year. On November 10, 2025, K92 Mining Inc. reported its Q3 figures for the quarter ending September 30, 2025. Revenue in the earnings period amounted to USD 177.5 million (+44.6% compared to the same quarter of the previous year) and profit was USD 85.7 million (+84.3% compared to the same quarter of the previous year).

K92 Mining announces operational guidance for 2026 - Significant production growth and exploration program planned

January 26, 2026

Neueste Nachrichten und Updates – Bleiben Sie informiert | K92 Mining Inc.

K92 Mining Announces Strong Fourth Quarter Production Results - Record Annual Production, Multiple Operating Records, Achieved Upper Production Guidance and Completed Commissioning of Phase 3 Expansion Process

January 12, 2026

Neueste Nachrichten und Updates – Bleiben Sie informiert | K92 Mining Inc.

CAD in millions

Estimates

Year Turnover Change

2025 811,7 60,83 %

2026 1.252 54,23 %

2027 1.719 37,29 %

2028 2.138 24,36 %

Year EBIT Change

2025 535,5 115,23 %

2026 929,4 73,54 %

2027 1.468 58 %

2028 1.797 22,4 %

Year Net result Change

2025 368,5 130,14 %

2026 527,8 43,25 %

2027 777,8 47,36 %

2028 992,7 27,63 %

Net debt not available

Year Free cash flow CAPEX

2023 -37,8 138,8

2024 36,1 195,5 %

2026 379,3 232,4

2027 796,7 180,2

2028 1.074 141,5

Year EBIT margin ROE

2024 49,3 % 26,94 %

2025 65,98 %

2026 74,24 % 37,9 %

2027 85,44 % 45,8 %

2028 84,09 % 37,6 %

Year Earnings per share Change

2024 0,6621 248,36 %

2025 1,514 128,61 %

2026 2,328 53,81 %

2027 3,507 50,62 %

2028 4,13 17,79 %

Year P/E ratio PEG

2025 15x 0x

2026 14.2x 0.3x

2027 9.46x 0.2x

2028 8.03x 0.5x

Market value 8,128

Number of shares (in thousands) 245,031

Date of publication 02,03,2026