Hello my dears,

I made a small additional purchase today.

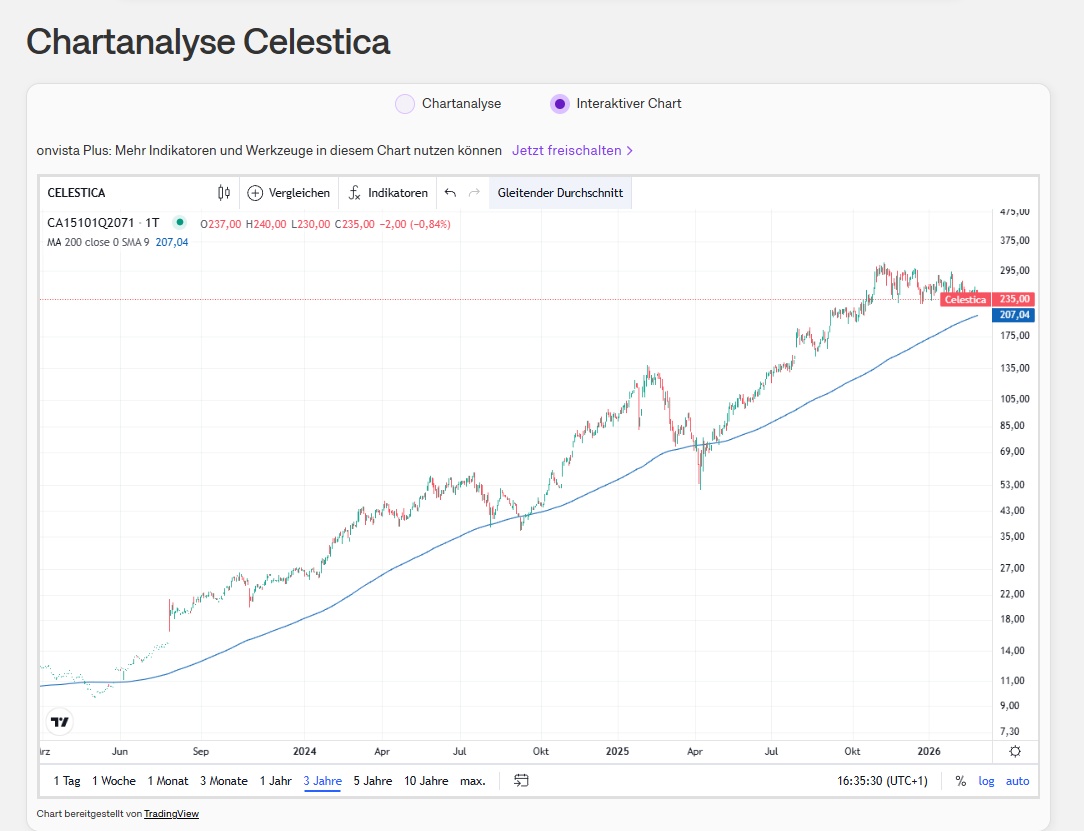

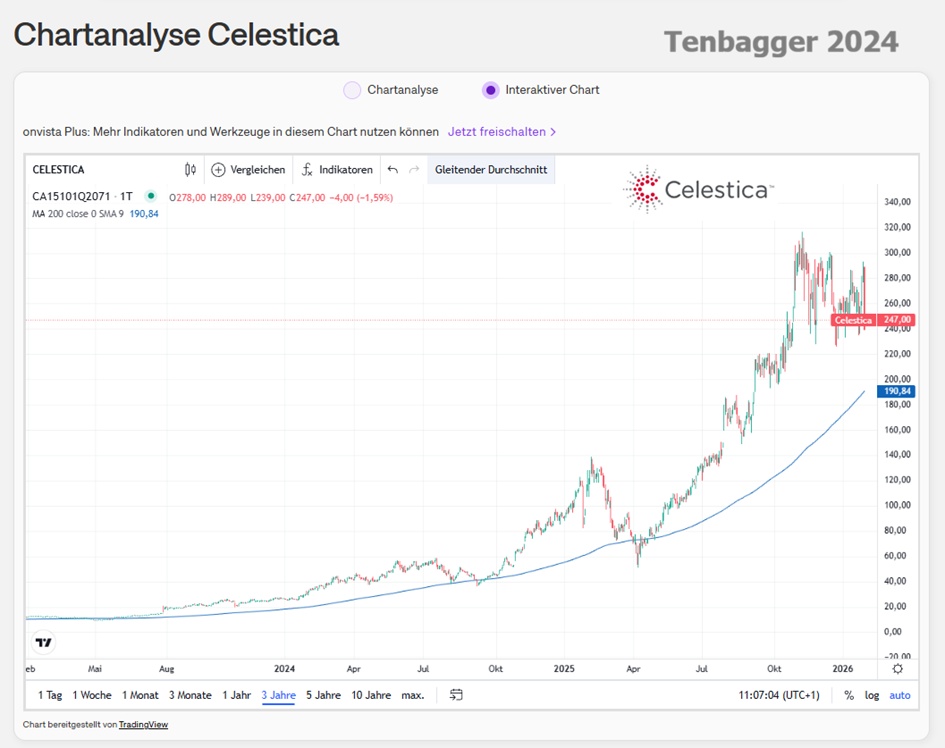

The share is approaching the 200-day line. I think this means that the consolidation should soon be over.

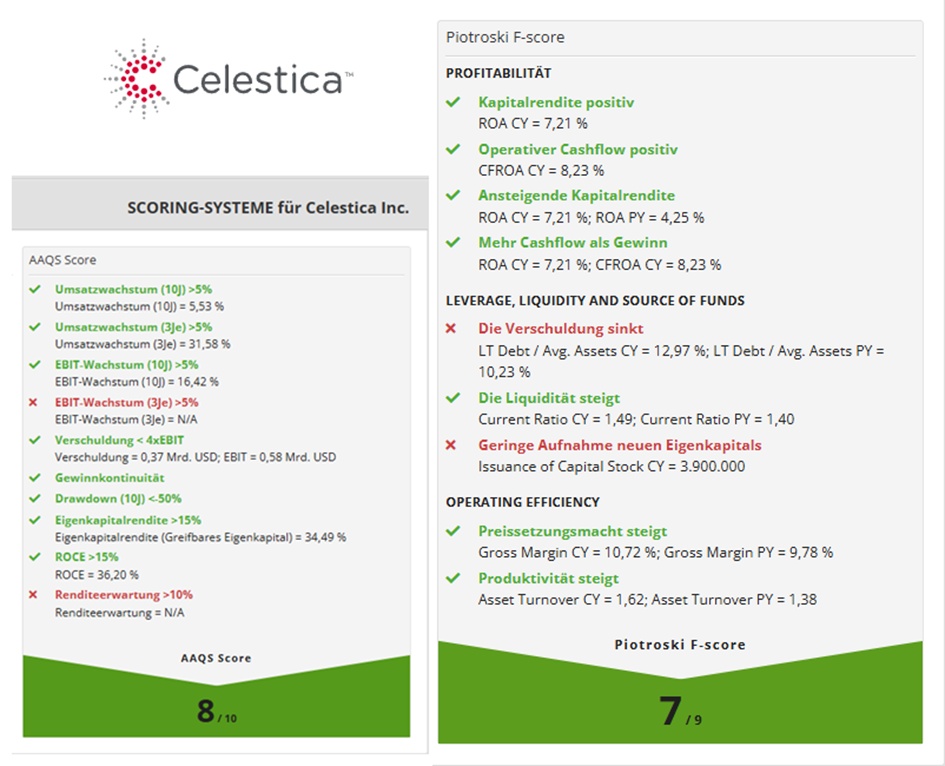

As already described in my analysis, the company's fundamentals look good.

I am therefore very confident.