Hello, everyone,

After I $5803 (-4,56 %) introduced Fujikura as a player in the fiber optics sector,

I didn’t want to keep another company from this sector from you.

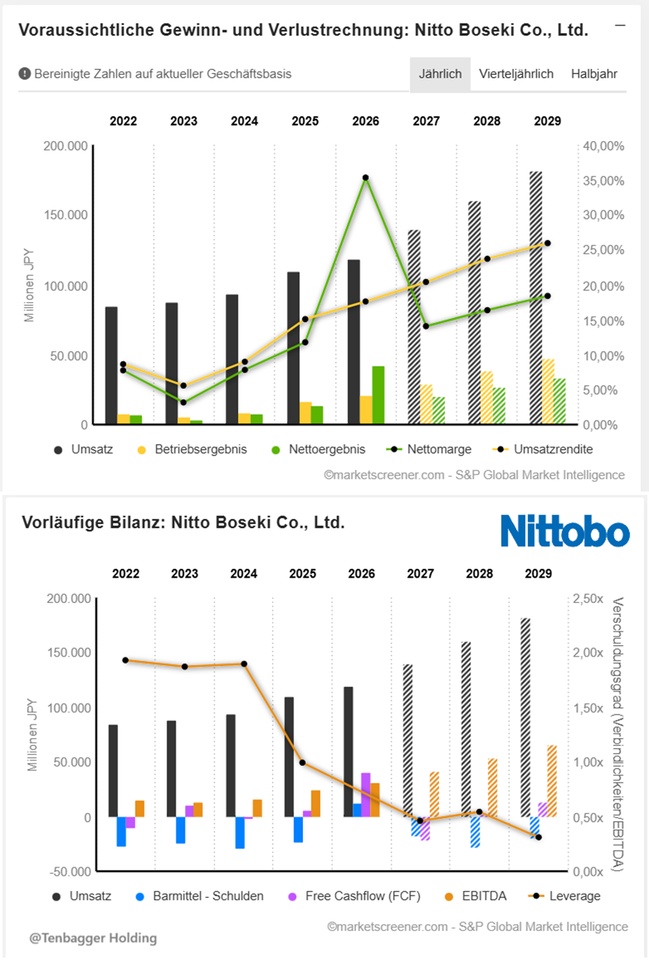

2026 is an exceptional year, with a 225% increase in net income.

Starting next year, Capex spending will rise to over 100% and will be directed toward expansion and new technologies.

This will bring net income back to a normal level.

My friends, could the stock enter a downtrend for the time being due to this decline and normalization?

Or do you still see the company as an exciting investment because of new technology and expansion?

Nitto Boseki Co., Ltd.. operates primarily in the business areas of electronic materials, medical products, composites, materials and chemicals, insulation materials, and other business areas. The company operates in six business segments. The Electronic Materials segment develops, manufactures, and sells glass fiber products for electronic materials. The Medical segment develops, manufactures, and distributes reagents for in vitro diagnostics. The Composites segment develops, manufactures, and distributes glass fiber products for plastic reinforcement materials. The “Materials and Chemicals” segment develops, manufactures, and markets glass fiber products for industrial materials, chemical products, interlinings, functional materials, and dishcloths. The “Insulation Materials” segment develops, manufactures, and distributes glass wool products for insulation, heat storage, and sound absorption. The “Other” segment designs industrial machinery and equipment.

Number of employees: 2,793

Founding dates:

February 1898 — Koriyama Kenshi Boseki Co., Ltd. (Koriyama)

April 1918 — Fukushima Seiren Seishi Co., Ltd. (Fukushima)

April 1923 — NITTO BOSEKI CO., LTD.

Business Activities

Electronic Materials:

- • Product development, manufacturing, and sales of glass fiber yarn and fabrics for electronic materials.

- • Glass fibers used in electronic applications have properties such as electrical insulation and heat resistance, and glass fabric is made from glass fiber yarn (thread). Applications include electrically insulating base materials for printed circuit boards.

- • Specialty glass is developed with unique compositions and is characterized by a low dielectric constant and low dielectric loss factor—properties required for broadband communication—as well as low thermal expansion. These properties make Nitto Boseki’s glass fibers a key material for high-frequency components in data centers and base stations, for infrastructure equipment such as servers, and for personal computers, smartphones, and other edge devices, as well as for vehicles. Their outstanding quality has earned high recognition worldwide.

Medical:

- NITTOBO MEDICAL CO., LTD., a wholly owned subsidiary of Nittobo, operates in the medical sector and focuses on in vitro diagnostic reagents.

- • In-vitro diagnostic reagents are used for testing samples such as blood and urine to diagnose diseases, both during doctor’s visits and during health screenings.

- • By managing a global value chain that spans from the production of raw materials in the U.S. to the commercialization of the final product, the Group ensures a stable supply of high-quality in vitro diagnostic reagents. Thanks to these supply capabilities, the Group has achieved the top market share in many categories, such as inflammatory biomarkers.

Composite Materials:

- Product development, manufacturing, and sales of glass fibers for plastic reinforcement materials and other composite materials

- • Glass fiber for composite materials leverages the properties of dimensional stability and processability and has established itself as a reinforcing material for plastics in a wide range of applications, including various automotive components, household appliances, and home furnishings.

- • By using different cross-sections—such as oval shapes instead of conventional round shapes—the proprietary high-performance glass with a unique cross-section developed by Nitto Boseki not only improves the impact resistance of the molded product but also prevents its deformation and offers additional outstanding properties. These characteristics have led to its use in the casings of smartphones, personal computers, tablets, and other devices.

Materials Solution:

- • Its industrial-use glass fiber business covers a wide range of applications, from membranes for large buildings to vibration-damping materials for automobiles. It has been adopted by the automotive and aerospace industries, where there is a need for improved fuel efficiency and reduced weight, and contributes to solving global environmental problems.

- • The Chemicals business is dedicated to the development and sale of highly innovative functional polymers and inorganic/organic nanocomposite materials (SSG).

- • In the textile sector, we will expand the use of the unique adhesive technology they have developed for adhesive interlinings and other applications from clothing to home products and industrial materials, providing functional materials.

Insulation Materials:

- • Nitto Boseki is engaged in the product development, manufacturing, and distribution of glass wool insulation materials that achieve a high level of thermal insulation performance.

- • Since all types of buildings must reduce their energy consumption to prevent global warming, glass wool is primarily used as an insulation material in residential buildings.

- • In addition to its energy-saving properties, well-insulated housing is also gaining attention from a health perspective, and NB is promoting the development of high-performance glass wool to meet the demand for improved insulation performance. Glass wool is also frequently used in ships and vehicles.

- • The glass wool manufacturing process helps reduce resource consumption by using recycled glass; more than 80% of the glass raw materials come from household glass bottles and other sources.

[News] Nittobo reportedly plans to launch Next-Gen T-Glass in 2028; customers may include NVIDIA, Apple, and others

Nittobo Group Financial Results for FY2025 (From April 2025 to March 2026)

2025/11/12Versuchserfolg: Recycelte Flachglasfaser aus Abfall-Solarpaneelabdeckungsglas (270KB)

2026/05/08Neue Materialtechnologie bietet eine Hochleistungsaufnahme von Kohlendioxid (916KB)

Revenue Breakdown by Business Segment:

2026 (JPY)

Electronic Materials Business 61.42 billion

Insulation Materials Business 15.16 billion

Composite Materials Business 14.46 billion

Medical Business 13.94 billion

Materials and Chemicals Business 11.73 billion

Unallocated Adjustment -20.6 billion

Other 22.13 billion

Geographic Revenue Breakdown:

2026 (JPY)

Japan 65.02 billion

Taiwan 17.56 billion

South Korea 14.16 billion

Other (Excl. Asia) 8.71 billion

Europe 7.26 billion

North America 5.08 billion

Others 442 million

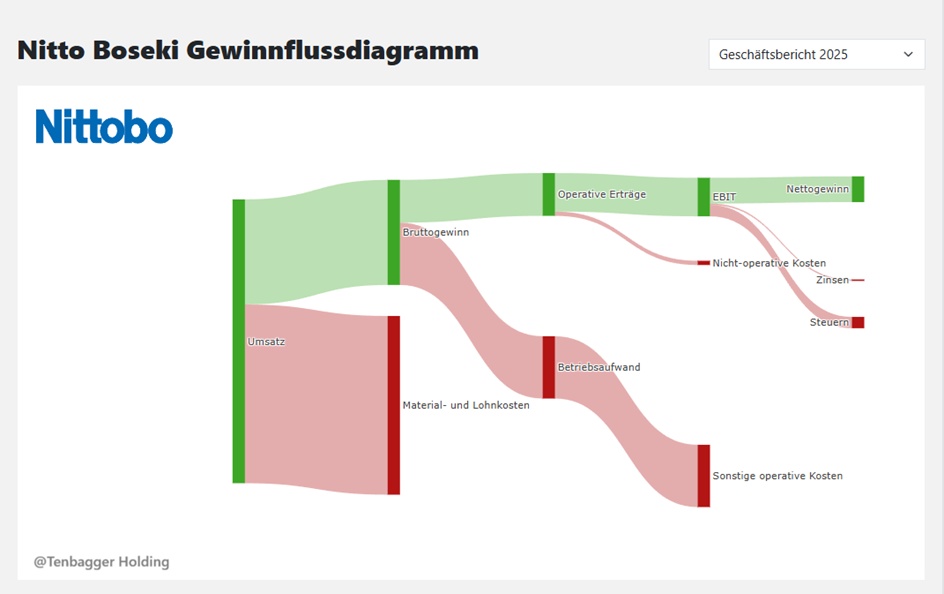

Juan’s Conclusion (short, clear, nerdily precise)

Bro, Nitto Boseki is delivering—but with a fair amount of volatility in tow.

Revenue & EBIT are rising steadily every year, really nice scaling, and the margins are rising like clockwork. That’s textbook operating leverage.

2026 is an outlier on the upside for profit, after which everything returns to normal. FCF is all over the place—first it skyrockets, then it crashes, then it skyrockets again. Typical for companies with large CAPEX cycles.

The Net debt fluctuates back and forth, but the trend heading toward 2029 is clear: The balance sheet becomes more stable, and the debt-to-equity ratio falls to 0.31×, which is really solid.

ROE is rising steadily, which shows that management is using capital more efficiently.

Bottom line: Nitto Boseki is a structural growth stock with margin expansion, but you have to take the FCF volatility . 2029 looks really strong—that’s when the company will be in the “sweet spot” between growth and profitability.

Quick Take (Juan-Style)

Bro, the company is set to go on a monster investment cycle. CAPEX is going through the roof because Nitto Boseki is massively expanding its production capacity. Years like this are always toxic for profits: Depreciation rises, operating costs rise, cash flow plummets—and net income returns to normal after the outlier year of 2026.

Starting in 2028/2029, however, it’s already clear: Margins are rising again, ROE is increasing, and the debt-to-equity ratio is falling. The investments are beginning to pay off.

Nittobo is deliberately pursuing a multi-year investment peakthat aligns perfectly with its “Big VISION 2030.”

Quick summary (Juan-style)

Bro, Nittobo is ramping up CAPEX because they’re pushing through their “Big VISION 2030.” New plants, new capacity, new technologies—that costs a lot of money at first. That’s why profits are falling in the short term. But starting in 2028/2029, you’ll already see: Margins are rising, ROE is rising, and the debt-to-equity ratio is falling. The investments are starting to pay off.

Market Value 719,001

Number of Shares (in thousands) 182,026

Date of Publication 05/12/2026

Juan’s Conclusion (short & to the point)

Bro, Nitto Boseki’s valuation is a total rollercoaster.

FCF yield swings wildly back and forth —first strong, then negative, then positive again. This shows that the market doesn’t consistently trust the cash flow because the CAPEX waves disrupt the model in the short term.

The P/E ratio is completely overvalued in 2027 (37×), but it normalizes back to a much more comfortable level by 2029. This is typical for companies that have had an outlier year and then return to normal operations.

The P/B ratio rises sharply, indicating that the market values the balance sheet quality more highly—despite the volatility.

The PEG is negative in 2027, which is always a warning sign: growth and valuation are diverging. Things look healthy again starting in 2028/2029.

Dividends per share are rising steadily every year, which is a strong sign of management discipline and a commitment to cash returns.

In short: Valuation is volatile, dividends are stable, and 2029 is clearly more attractive than 2027. The market is pricing in the investment cycles—and will reward the company as soon as margins pick up again.

Performance

1 week -2.78%

1 month -19.23%

6 months +89.19%

1 year +201.72%

3 years +639.44%

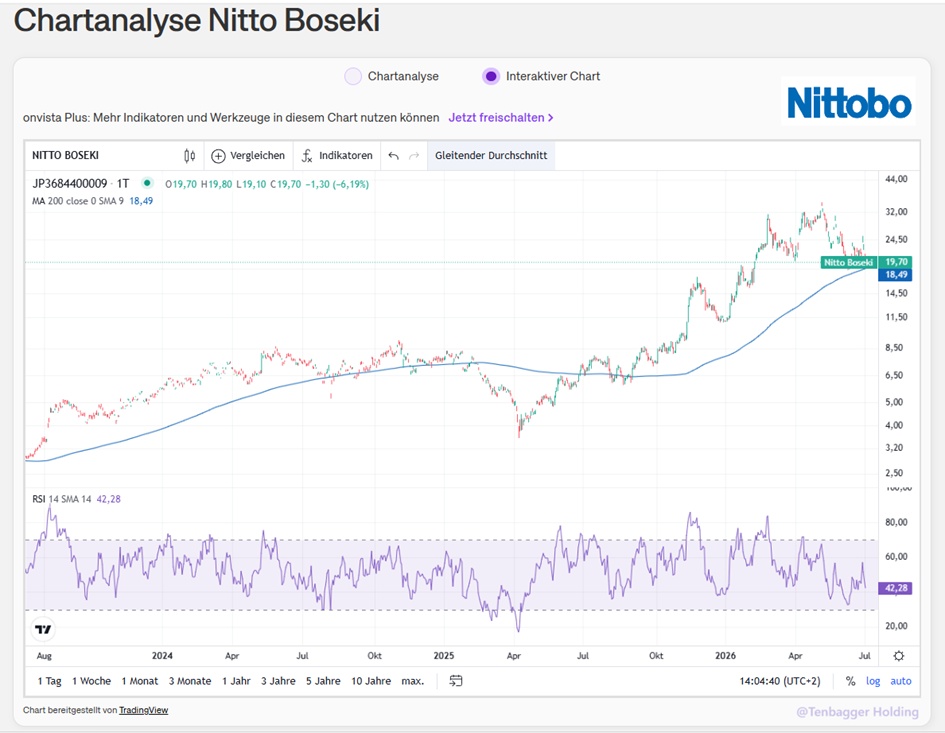

July 2, 2026, 5:32:29 PM •

gettex (EUR)

19.70 EUR