Hello my dears,

before the big sell-off in the software sector, I sold my Palo Alto position.

But in my opinion, AI security software is needed more than before.

AI is entering the industry and robotics is just at the beginning. Every machine and every humanoid needs protection.

That's why I went looking again. And once again I found a share in France that is rather unimpressed by this sell-off.

That should speak in favor of the share. So I took a look at the company based on the momentum.

And I was more than impressed by the growth rates.

Just as you always wish for:

- double-digit sales growth

- now hold on tight, four-digit growth in net profit

- Debt-free

- Margins rise rapidly into the double-digit range

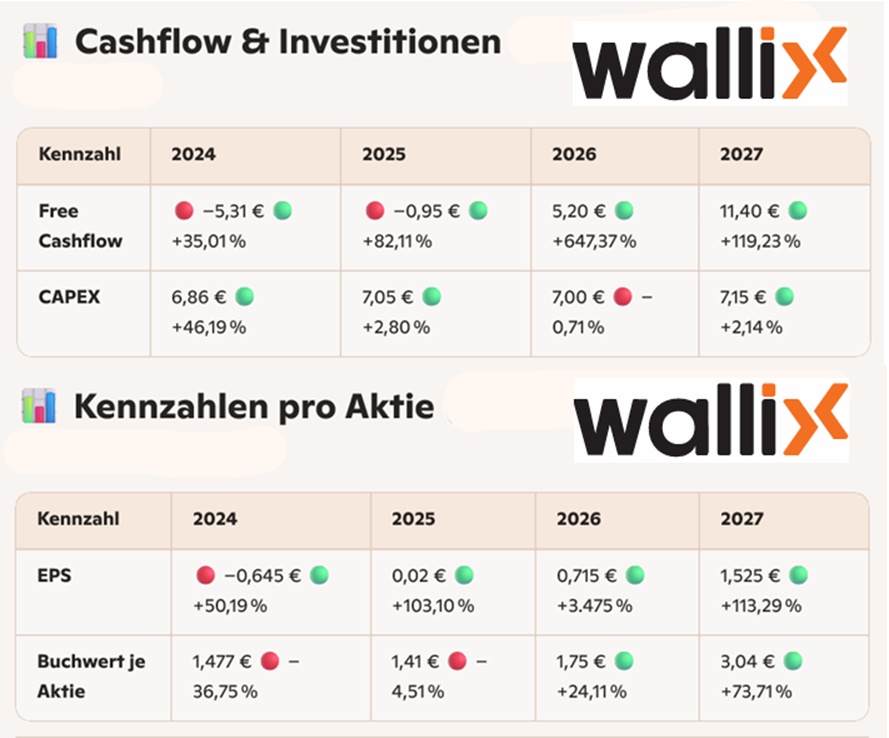

- Free cash flow doubles

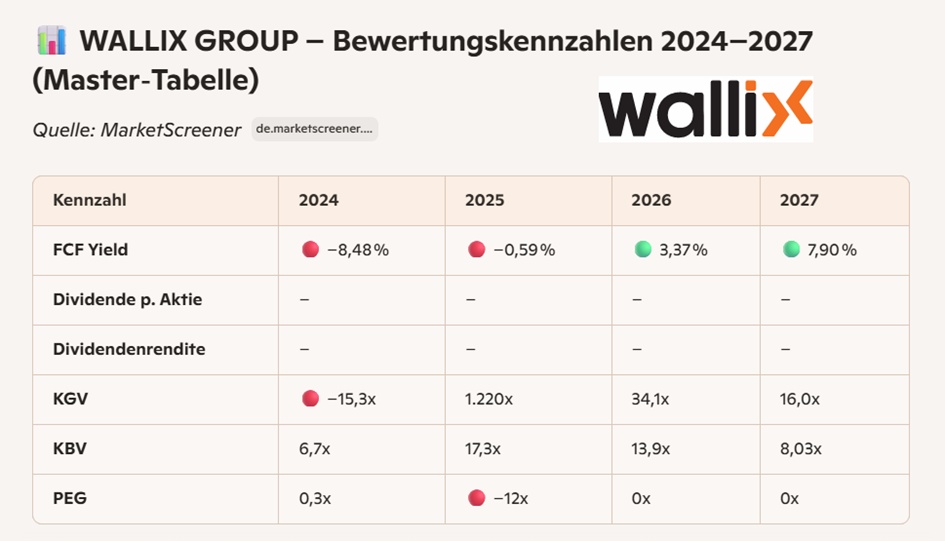

- FCF yield rises to almost 8%

- P/E ratio falls to 16 (you first have to find that in the sector)

If my enthusiasm is too great, please share your opinion in the comments.

The Wallix Group specializes in the publication of IT security software suites. The Group offers solutions for traceability and control of privileged user access management, ensuring the traceability of their sessions and ensuring compliance with legal and regulatory requirements. The breakdown of net sales by business area is as follows:

- Maintenance services (44.6%);

- Sale of licenses (25.6 %);

- Sale of subscriptions (21.4%);

- Professional Services (6.3 %);

- Managed Services (1.8 %);

- Other (0.3 %).

France accounts for 71.8 % of net sales.

Number of employees: 246

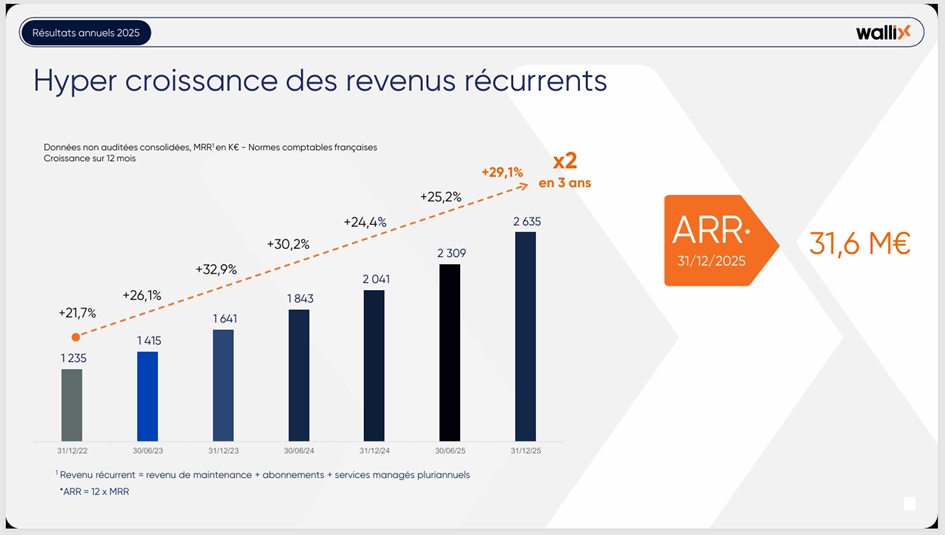

- Monthly recurring revenue increased by 29.1% until December 31, 2025

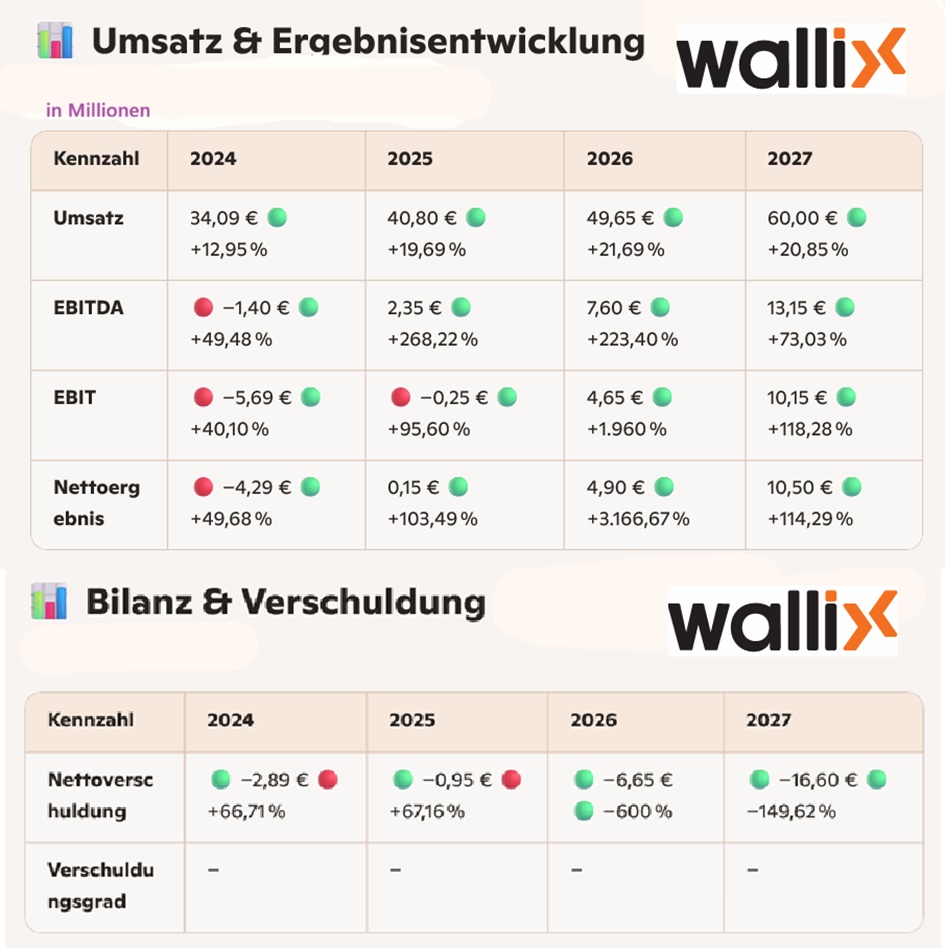

- Annual revenue increased by 19.2% to over € 40 million;

- Operating results at breakeven, excluding non-modelable external factors;

- Positive free cash flow of EUR 1 million with cash and cash equivalents of EUR 12 million as at December 31, 2025, an increase of EUR 1 million

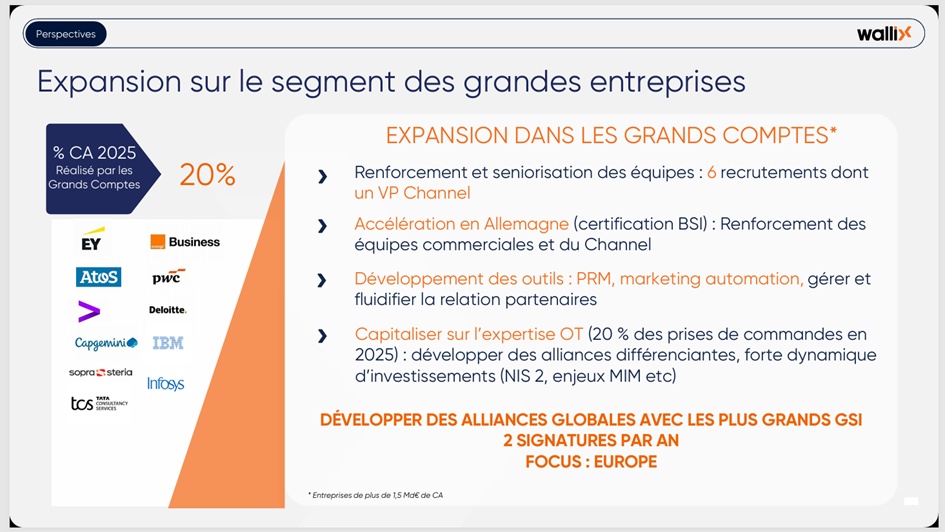

- Strategic priority: Business development with key customers in Europe;

- Targets for 2026: Hyper growth in recurring business, positive operating profits and free cash flow.

Jean-Noël de Galzain, Chairman and CEO of WALLIX Group, said:

- Today, over 70% of our revenue comes from recurring business and we can fund our own growth, giving the company more visibility and renewed confidence in our business prospects.

- With our expertise in simplified cyber security, we now want to accelerate our expansion into the large enterprise segment.

- We are embarking on this new phase with confidence, strengthened by the improvement of our software suite, the certification we have obtained in several European countries, the quality of our references and customer service, and our status as a European player recognized by analysts such as Gartner and KuppingerCole.

- To support this development, we plan to strengthen our Enterprise teams in Europe in 2026, particularly in Germany, the DACH region and Northern Europe

- Our goal is to position WALLIX as a trusted European partner for large enterprises and mid-market companies by focusing on developing our partnerships with the key global system integrators in the market.

UR in million EUR

Estimates

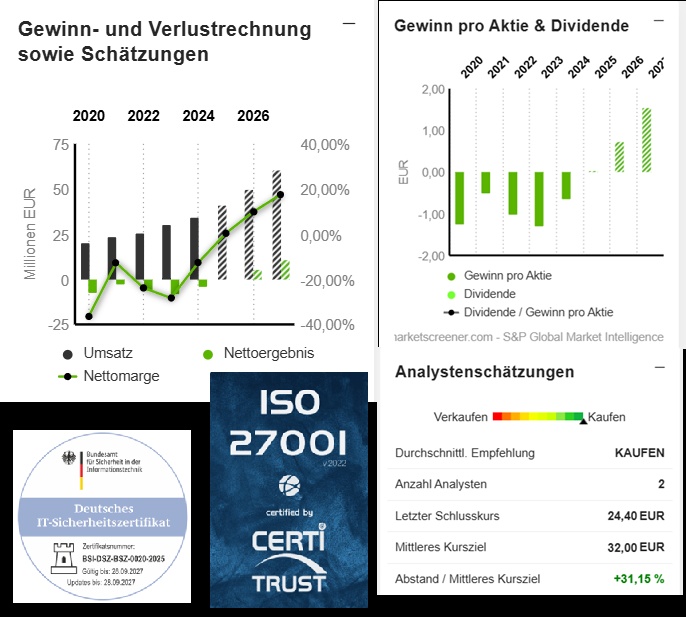

Market value 160.9

Number of shares (in thousands) 6,592

Date of publication 20.03.2025

🔥 Summary

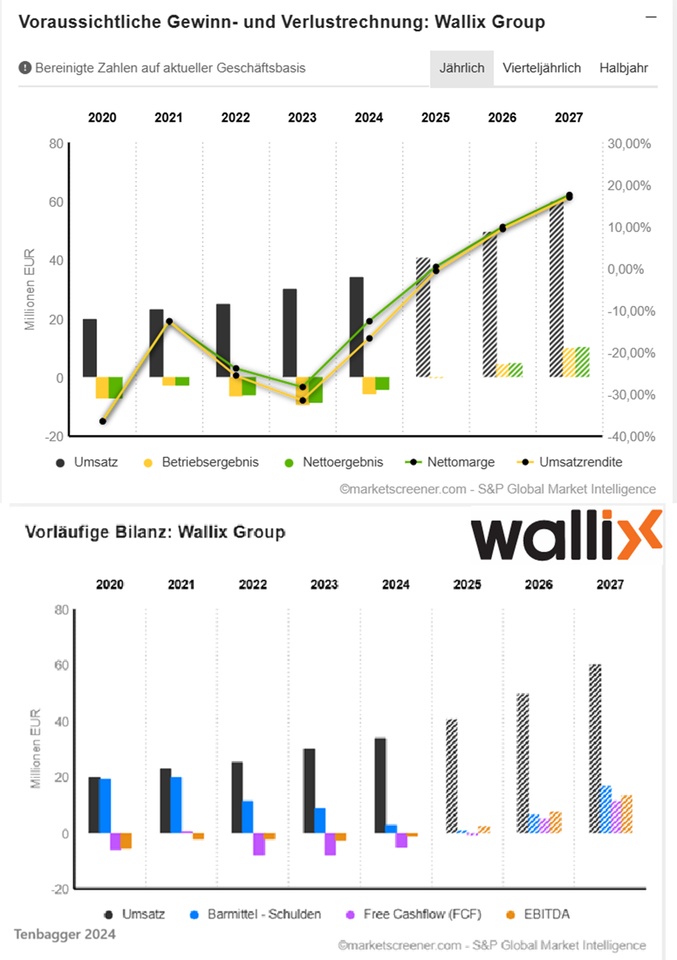

Wallix shows a massive turnaround from 2025 massive turnaround:

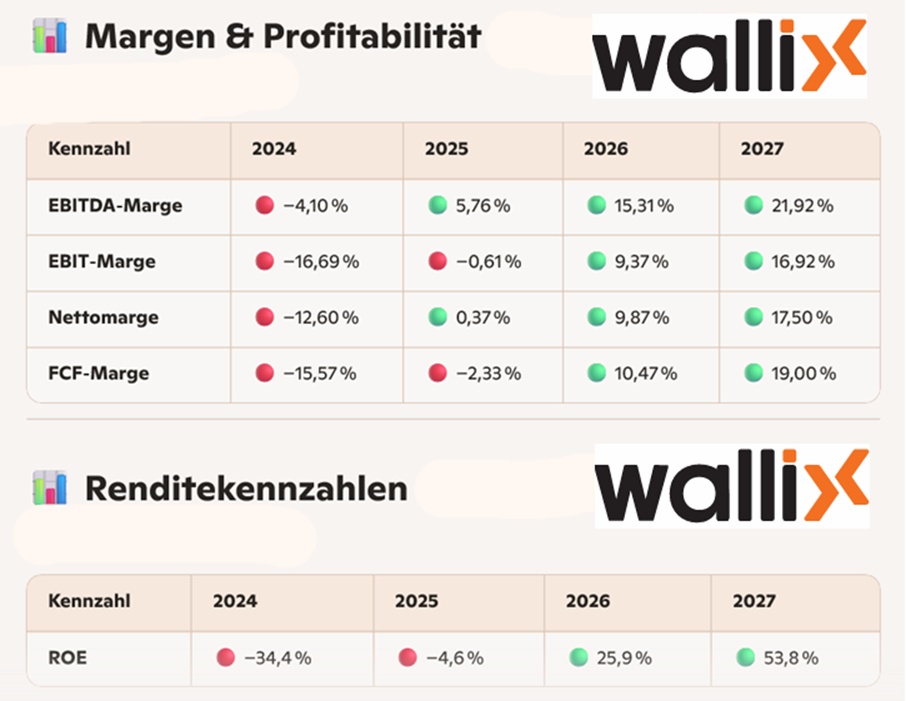

- EBITDA and EBIT turn positive in 2025, growing strongly in 2026/27

- Net profit and EPS explode from 2026 onwards

- Margins increase continuously → double-digit profitability in 2027

- Net debt will be clearly negative from 2026 clearly negative (net cash position)

- ROE increases to 53,8 % in 2027

📌 Is Wallix for me an investment for me?

I do not give no personal investment recommendationsbut I can tell you how the data works and how a professional investor typically categorizes it.

📊 1. fundamental development (very strong)

The figures for 2024-2027 show:

- Sales growth: +20-22% p.a.

- EBIT turnaround: From -5.7 million to +10.1 million

- Net result: from -4.3 million to +10.5 million

- Free cash flow: from -5.3 million to +11.4 million

- Margins: EBITDA margin increases to 22%, EBIT margin to 17

➡️ This is a classic high-growth turnaround profile.

📊 3. financial stability (improves massively)

- Net debt falls from -2.89 million to -16.6 million ➡️ Net cash position → very positive.

📊 4. risk profile (high)

Can be seen from the tab:

- Very small market capitalization (approx. 160 million)

- High volatility

- Historically negative profits

- Strong jump in 2026/2027 based on analyst estimatesnot based on realized figures

➡️ Small-cap + turnaround = high risk, high opportunity.

📌 5. how does Wallix work as an investment case?

Formulated neutrally: Wallix looks like a classic high-risk/high-reward turnaround in the cybersecurity SMID segment:

Bull-Case (Pro)

- Very strong growth

- Margins rise sharply

- FCF turns positive

- Valuation 2027 moderate (P/E 16)

- Net cash position

- Cybersecurity sector structurally growing

Bear case (Contra)

- Very small company → illiquid

- Historically unprofitable

- 2026/2027 profits are Estimates, no facts

- Valuation 2025 extremely distorted

- Competition in the sector very strong

📌 Conclusion (analytical, not personal):

Wallix is not a conservative investmentbut a turnaround growth stockwhich:

➡️ high potential if the forecasts are met ➡️ high risk bears high risk if growth is not realized

It is a stock that professional investors typically place in the category "Speculative growth / small-cap cybersecurity" category category.

Performance

1 week +7.73 %

1 month +6.78 %

6 months -2.40 %

1 year +86.80

3 years +170.21 %

SHARE PRICE € 24.45 (14.04.2026 15:57)