Die Entdeckung: Ein Spaziergang in Valby

Nachdem wir uns bei $MINEST (+11,64 %) in die stürmischen Tiefen des Nordatlantiks gestürzt haben, brauchten wir dringend wieder festen Boden unter den Füßen.

Was liegt da näher, als sich direkt hier bei uns in Dänemark umzuschauen?

Wir haben gestern das schöne Frühlingswetter für einen Spaziergang durch Valby in Kopenhagen genutzt. Und wenn man dort an den massiven Backsteingebäuden des Hauptquartiers von H. Lundbeck A/S (ISIN: DK0061804770) $HLUN B (+0,41 %) vorbeiläuft, fällt einem auf:

Warum in der Ferne nach spekulativen Renditen suchen, wenn ein globaler Pharma-Spezialist direkt vor der Haustür Geld druckt?

Das ist exakt das Gegenteil von den reinen Biotech-Zockerbuden ohne klaren Weg zur Profitabilität, die bei uns sonst gnadenlos durchs Raster fallen. Lundbeck ist alteingesessene, dänische Pharma-Substanz.

Hier direkt der formelle Disclaimer: Ich bin aktuell in H. Lundbeck nicht investiert. Wir schauen uns das Ding heute rein analytisch, neutral und eiskalt an.

1. Das Geschäftsmodell: Was macht Lundbeck?

Lundbeck baut keine Aspirin und keine Pflaster. Sie sind ein hochspezialisierter Global Player im Bereich der Erkrankungen des zentralen Nervensystems (ZNS). Wir reden hier von Medikamenten gegen Depressionen, Schizophrenie, Alzheimer und Migräne. Ihre Blockbuster heißen Rexulti, Trintellix und ihr neuester Wachstumsmotor Vyepti (eine intravenöse Migräne-Behandlung, die gerade den Markt aufrollt).

2. Marktstellung & Burggraben

Das ZNS-Feld ist der Endgegner der Pharmabranche. Die Gehirnforschung ist unfassbar komplex und die Ausfallraten bei klinischen Studien sind nirgends so hoch wie hier. Das ist ihr Burggraben! Große Pharmakonzerne haben sich oft aus diesem Bereich zurückgezogen, weil es zu teuer und riskant ist. Lundbeck hat über 70 Jahre Erfahrung in dieser Nische und dominiert sie profitabel.

3. Key Figures (Stand: April 2026)

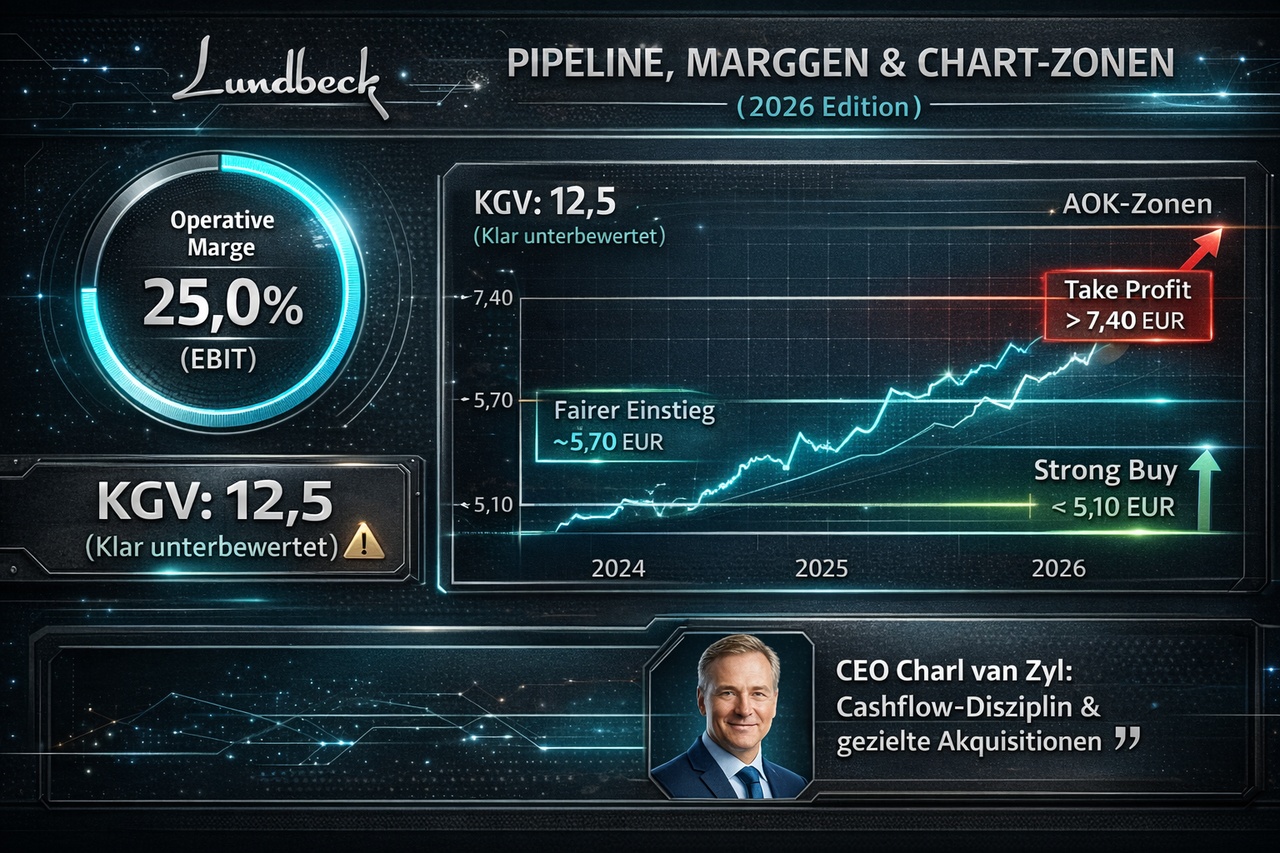

Aktueller Kurs ~5,70 EUR

Marktkapitalisierung ~5,6 Mrd. EUR

Kurs-Gewinn-Verhältnis (KGV)

~12,5 (Extrem günstig!)

Kurs-Cashflow-Verhältnis (KCV)

~8,5

Dividendenrendite

~3,6 %

4. Core Quality Formula (Der Qualitäts-Check)

Score = Umsatzwachstum + Operative Marge

- Umsatzwachstum: ~ +7,5 % (getrieben durch Vyepti und Rexulti).

- Operative Marge (EBIT): Satte 25,0 %.

- Ergebnis: 7,5 + 25,0 = 32,5

- Urteil: Mit 32,5 Punkten zerschmettert Lundbeck unsere 25-Punkte-Hürde. Das ist ein erstklassiges, qualitatives Wachstum und beweist, dass die Margen im Spezial-Pharma-Bereich gigantisch sind.

5. Cashflow Quality Formula (Die Cash-Maschine)

FCF = Operativer Cashflow - CapEx

- Free Cashflow: Lundbeck $HLUN B (+0,41 %) wandelt fast den gesamten Gewinn in harten Cash um, da die Fabriken stehen und der CapEx (im Vergleich zu Schwerindustrie oder Netzbetreibern) moderat ist.

- FCF-Yield: Liegt aktuell bei fantastischen ~8,2 %.

- Urteil: Über 8 % bedeutet "Sehr attraktiv". Lundbeck ist eine absolute Cash-Maschine und hat null Probleme mit "Bilanz-Kosmetik".

6. Dividend Filter (Income-Core)

- Rendite:

~3,6 % (Check! Liegt über unserer 3,5 % Mindestanforderung).- Nachhaltigkeit: Die Payout-Ratio liegt historisch bei entspannten 30 % bis 40 %. Der Cashflow deckt die Dividende doppelt und dreifach. Keine Pseudo-Dividende auf Pump.

7. Zukunftsaussichten & Strategie

Der Elefant im Raum bei Pharma ist immer der „Patentklippen-Effekt“ (Loss of Exclusivity). Trintellix verliert Ende der 2020er Jahre seinen Patentschutz. Deshalb fokussiert sich Lundbeck jetzt massiv auf die Skalierung von Vyepti und strategische Übernahmen im Bereich der Neuropeptide, um die Pipeline für 2030+ zu füllen.

8. Wettbewerb & Ersetzbarkeit

Konkurrenz gibt es von Giganten wie AbbVie oder Biogen, aber Lundbeck ist als "Pure Play" agiler. Du kannst Lundbeck in deinem Depot höchstens durch einen breiten Pharma-ETF ersetzen, verlierst dann aber die geballte ZNS-Fokus-Marge und die günstige Bewertung.

9. Chart-Analyse (Die aktuelle Lage)

Die Aktie hat eine harte Zeit hinter sich, weil der Markt Pharma-Werte mit bevorstehenden Patentabläufen oft wie heiße Kartoffeln fallen lässt. Der Chart hat um die 4,70 EUR einen massiven Beton-Boden gebildet und zieht jetzt wieder in Richtung 6,00 EUR an. Der Abwärtstrend ist gebrochen.

10. Bargain Hunter's List (Einstiegszonen)

- Strong Buy (Bunker-Preis): < 5,10 EUR

- Fairer Einstieg: 5,35 – 5,75 EUR (Aktuelles Niveau)

- Teuer: > 7,40 EUR (Hier preist der Markt dann eine fehlerfreie Pipeline ein).

11. Was sagt der CEO? (Die neuesten News)

CEO Charl van Zyl hat das Ruder fest in der Hand. Seine Kernaussage in den letzten Calls: Fokus auf Profitabilität und "gezielte Business-Development-Deals". Anstatt Milliarden für riskante Riesen-Übernahmen zu verbrennen, kauft er clevere kleine Biotech-Assets ein, um die hauseigene Pipeline zu stärken. Er liefert exakt das, was Value-Investoren hören wollen: Cashflow-Disziplin.

12. Analysten-Konsens: Wie sehen die Profis den Titel?

Der Markt hasst Unsicherheit, und Pharma ist Unsicherheit. Deshalb liegt das durchschnittliche Analysten-Kursziel "nur" bei ca. 6,45 EUR (also einem moderaten Upside). Die Meinungen gehen auseinander: Die Value-Häuser lieben den Cashflow und das niedrige KGV von 12. Die Wachstums-Fanatiker meckern über die Patentabläufe ab 2028. Ein klassisches "Hold / Cautious Buy"-Rating am Markt.

Mein Fazit & Zukunftsfähigkeit

Lundbeck $HLUN B (+1,48 %) ist kein Tenbagger, und das wollen wir hier auch gar nicht. Wenn man sich in Dänemark umschaut, stürzen sich alle blind auf Novo Nordisk bei einem KGV von 40. Aber für den smarten AOK-Investor bietet Lundbeck bei einem KGV von 12,5, einer Marge von 25 % und über 8 % FCF-Rendite ein absurdes Maß an Sicherheit. Das ist ein massiver Qualitäts-Compounder für die Ecke des Depots, in der das Licht ausbleibt und das Geld still und heimlich arbeitet.