$MC (+0,78 %)

$MBG (-1,09 %)

$ULVR (-2,04 %)

$PYPL (-0,54 %)

$NBIS (-2,65 %)

$SPGI (+0,17 %)

$UPS (+0,13 %)

$KO (+0,1 %)

$GLW (-0,07 %)

$BA (-1,75 %)

$KER (-2,14 %)

$ENPH (+0,43 %)

$NXPI (-7,11 %)

$STX (-1,6 %)

$BE (-3,13 %)

$V (+0,06 %)

$MDLZ (-1,1 %)

$000660

$P911 (-3,4 %)

$BN (-1,3 %)

$RMS (-0,74 %)

$BAS (-1,34 %)

$AG1 (+2,01 %)

$LMND (+0,47 %)

$SOFI (-1,1 %)

$NDX1 (-1,22 %)

$TER (-1,58 %)

$GD (-0,7 %)

$APH (+0,48 %)

$AIR (-0,78 %)

$SBUX (-0,79 %)

$CMG (-3,14 %)

$META (+2,62 %)

$FTNT (+5 %)

$QCOM (-2,98 %)

$LRCX (-3,35 %)

$HOOD (-0,69 %)

$ARM (-2,83 %)

$MSFT (+3,6 %)

$CVNA (+1,35 %)

$005930

$SU (+1,8 %)

$INGA (+0,96 %)

$OR (-1,76 %)

$BMW (-1,74 %)

$BATS (-1,11 %)

$MA (+0,34 %)

$ADS (+0,95 %)

$SHEL (+1,52 %)

$RACE (-0,2 %)

$RDDT (-14,39 %)

$TEM (-0,29 %)

$COIN (-4,94 %)

$AAPL (-2,89 %)

$AMZN (+6,74 %)

$CCO (-2,68 %)

$LIN (-6,28 %)

$ABBV (-2,62 %)

$PUM (-2,66 %)

$HAG (-4,38 %)

$XOM (-0,25 %)

$CVX (+2,08 %)

Samsung Electronics

Price

Debate sobre 005930

Puestos

49Quarterly Results: July 27–July 31, 26

My next purchase?!

First, I’d like to officially @Tenbagger2024 officially welcome back from the sidelines! 🫡 It’s great to have you back!

I hope you were able to enjoy your time off, recharge your batteries 🪫, and return with new energy 🔋 and your usual strength 💪. The community has definitely missed a familiar name—without your insights and analyses, things here were almost a little too quiet. 🙇♂️

And what can I say: Your comeback came even faster than that of the German national soccer team after their latest setbacks—so the bar wasn’t set too high. 😂⚽

With that in mind: Welcome back, my friend! I’m excited to see which companies you’ll pull out of your sleeve this time and which candidates will once again be scrutinized mercilessly. 💀

————————————————————————-

While the market focuses its attention on the usual suspects, there are always companies that fly largely under the radar. One such candidate has been on my watchlist for quite some time and is now on the verge of making the leap into my portfolio.

Today, I’d like to show you why I consider this company (another stock from Japan) to be an extremely exciting investment candidate.

Today’s focus is on Hoya Corp $7741 (+1,46 %)

HOYA Corp.: The Invisible Monopoly of the Optics & Chip World

While the stock market is fixated on $ASML (-1 %) ASML’s EUV lithography machines or the mass production of wafers by $2330 , a Japanese heavyweight has established itself in the shadow of the tech giants—one without which not a single sub-3nm processor can be manufactured in the age of AI and semiconductors: HOYA Corporation. $7741 (+1,46 %)

HOYA $7741 (+1,46 %) does not manufacture finished microchips or hospital diagnostic devices. HOYA $7741 (+1,46 %) supplies the physically perfect, high-precision materials upon which all global progress in the chip industry and medical technology is built.

The difference from ordinary suppliers is enormous: HOYA $7741 (+1,46 %) combines the explosive, high-margin growth of the AI and semiconductor sectors with the crisis resilience of a global medical technology monopoly.

1. The Business Model: The Highly Profitable Dual Engine ⚙️👁️

HOYA $7741 (+1,46 %) scales through a perfectly balanced two-pillar model that hedges the cyclical dynamics of the tech world with defensive healthcare cash flows:

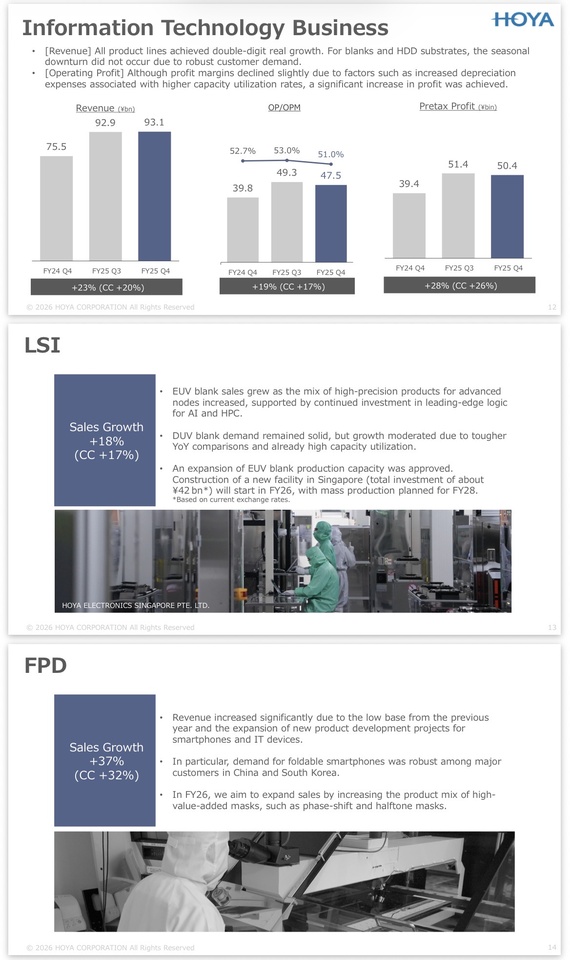

① Information Technology (IT) Segment (~46–48% of revenue):

- EUV Photomask Blanks: High-purity quartz glass blanks that serve as photomasks for the most advanced chip manufacturers (sub-3nm, high-NA EUV). HOYA $7741 (+1,46 %) holds a virtual global monopoly in this sector (>80% market share).

- HDD Glass Substrates: Ultra-flat glass substrates for high-capacity hard disk drives in data centers. Glass enables higher storage densities than aluminum—essential for the data deluge generated by AI hyperscalers.

- Operating Margin: A staggering ~54.1%! This segment is a true money-making machine that benefits directly from the AI and semiconductor boom.

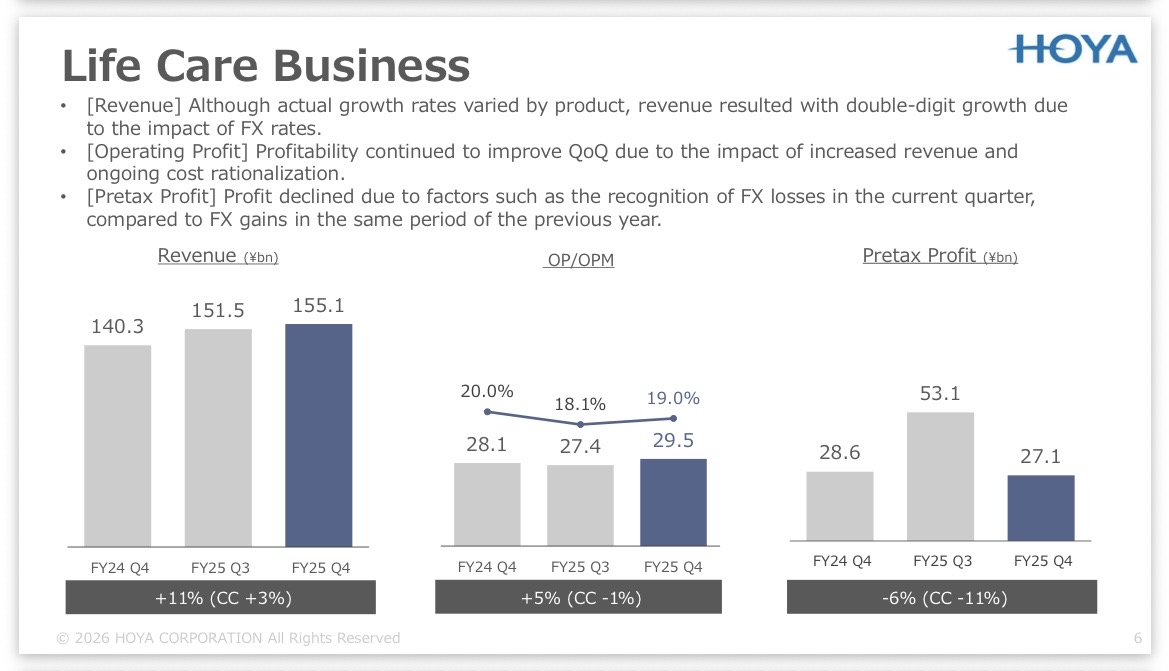

② Life Care Segment (~52–54% of revenue):

- Products: Optometry (eyeglass lenses, contact lenses) and MedTech (PENTAX endoscopes, intraocular lenses for cataracts).

- Operating Margin: Extremely solid ~18.1%.

- Competitive advantage: Provides a crisis-resistant, non-cyclical foundation. Even if the semiconductor industry stagnates, people will still undergo eye surgeries and purchase vision aids.

2. The Technology: Why Sub-3nm & AI Data Centers Would Fail Without HOYA

HOYA’s unique physical selling point $7741 (+1,46 %) lies in its its mastery of glass and materials science at the nanometer scale. Two key drivers make HOYA $7741 (+1,46 %) indispensable:

- EUV lithography & high-NA EUV: When exposing state-of-the-art chips with extreme ultraviolet (EUV) light, the photomask must be free of any molecular deviations. A tiny defect on the mask can ruin millions of chips. HOYA’s blank materials offer a defect density close to zero. Without HOYA, $7741 (+1,46 %) , there would be no yield for $AAPL (-2,89 %) Apple Silicon, $NVDA (+2,15 %) Nvidia GPUs, or $AMD (-2,55 %) AMD processors.

- HDD glass substrates for AI data centers: Cloud storage space is growing exponentially. Conventional aluminum platters in hard drives bend under extremely high rotational speeds and multiple layers. HOYA’s specialty glass is stiffer, flatter, and enables significantly higher storage capacities per hard drive.

The Validation Moat: Just as with tooling suppliers, the approval of a new mask blank or glass substrate at TSMC $2330 , Samsung $005930 or Intel $INTC (-2,75 %) is a multi-year qualification process. The switching costs for chip manufacturers are immense.

3. Geographic Distribution: Global Players with Little Home Bias 🌍

HOYA $7741 (+1,46 %) is listed in Tokyo, but generates just under 85–88% of its revenue abroad. This provides protection against Japan’s domestic demographic trends and yields massive currency advantages when the yen is weak:

REGION :

🇹🇼🇰🇷🇨🇳ASIA/China

Revenue share: ~35%–38%

Key drivers: semiconductor foundries (TSMC, $2330 Samsung $005930 ) IT packaging hubs

🇪🇺Europe

~28%–30%

Strong life care medtech business (eyewear & endoscopes)

🇺🇸North America

~20%–22%

Data center hyperscalers & U.S. chip design (EUV/HDDS)

🇯🇵Japan

~12%–14%

Medtech sales & optical R&D/manufacturing sites

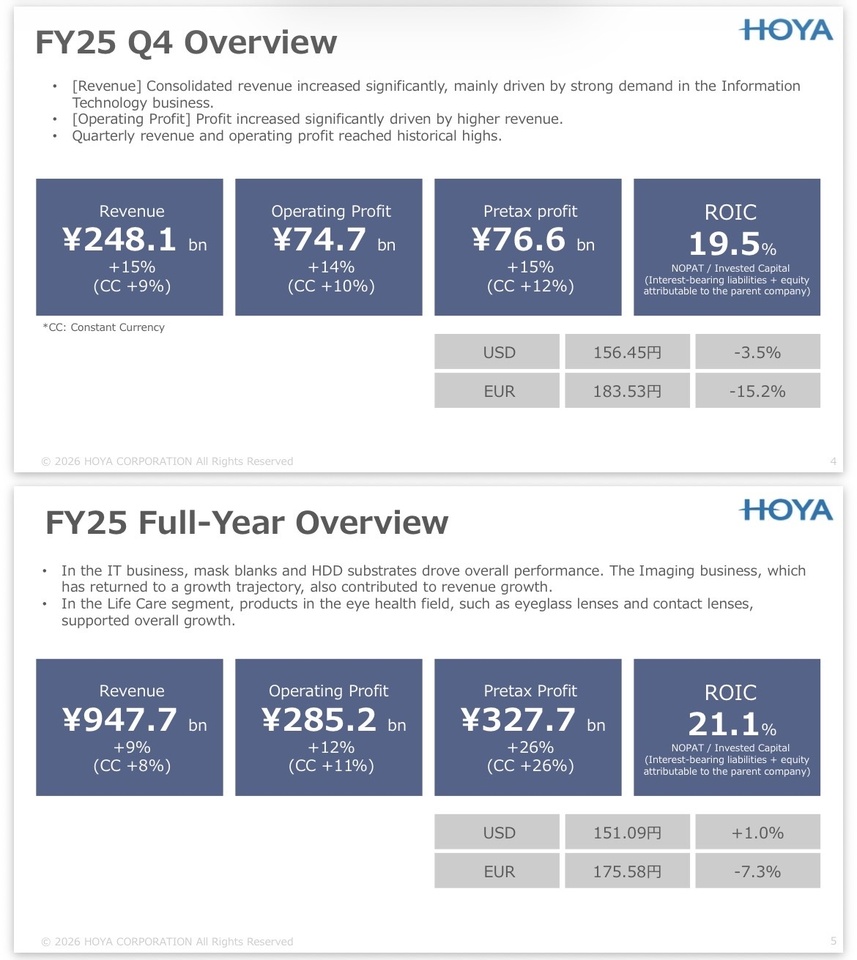

4. Key Financial Metrics (Fundamental Analysis & Financial DNA) 📊

- Market Capitalization: ~6.8 to 7.2 trillion JPY (approx. 42–45 billion EUR) – A true global tech/medtech mega-cap on the Tokyo Stock Exchange.

- Revenue Growth (Segment Dynamics):

- IT segment:

+36% YoY (strongly driven by EUV blanks and AI-driven HDD demand). - Life Care Segment:

+9% YoY (stable, non-cyclical anchor). - Consolidated EBIT margin:

~35–38% – Due to the IT division’s high profit contribution (54.1% margin), the overall performance is on par with the software sector. - Return on Invested Capital (ROIC):

>22% – Indicates excellent opportunities for reinvestment and high capital efficiency. - Free Cash Flow Margin:

>22% – HOYA $7741 (+1,46 %) consistently converts operating profits into true FCF. - Balance Sheet Strength: Net debt/EBITDA is negative (net cash). HOYA $7741 (+1,46 %) has an extremely large cash reserve and faces absolutely no refinancing risk.

5. Why is this stock exciting? 🚀

The undisputed “hockey stick” segment (EUV boom): As the chip industry switches to high-NA EUV machines from ASML, the demand for even more precise mask blanks is rising dramatically. HOYA $7741 (+1,46 %) benefits from every technological leap in the semiconductor industry.

Defensive safety net: If the semiconductor market enters a cyclical correction, the defensive MedTech segment (Life Care) cushions the valuation and ensures rock-solid cash flows.

At the heart of the AI infrastructure hub: HOYA $7741 (+1,46 %) benefits twice when it comes to AI: once through the production of logic chips (EUV) and once through the storage of massive amounts of AI data (HDD glass substrates).

6. Risks ⚠️

- Geopolitics in East Asia: Since the majority of the IT business is handled by foundries in Taiwan 🇹🇼 and South Korea 🇰🇷, there is a significant concentration risk in the event of a China-Taiwan conflict.

- U.S. Export Restrictions: Tighter U.S. sanctions against the Chinese chip industry could dampen shipments of high-end substrates and blanks.

- Exchange rate sensitivity (JPY): As a highly export-oriented company (85–88% of revenue from overseas), a sudden appreciation of the yen leads to foreign exchange losses on the balance sheet.

🎯 EARNINGS PREP: What to watch for in the next earnings report?

The upcoming quarterly results (Q1 of fiscal year 2027) from HOYA Corp. are just around the corner:

📅 Date:

Thursday, July 30, 2026 (or July 31, depending on the time zone)

⏱ Time: HOYA typically publishes $7741 (+1,46 %) releases its results around 1:30 p.m. JST (approx. 6:30 a.m. German time).

📊 Reporting Period: Just-ended first quarter (3 months ending June 30, 2026).

💡 Analyst expectations (consensus)

Revenue: ~$1.55 to $1.57 billion (driven largely by continued demand in the IT/EUV segment).

Earnings per Share (EPS): ~$1.15

For the upcoming earnings update, the key metrics will primarily focus on the IT division and margin trends. The following points should be on your radar:

1.🎭 EUV & High-NA Blank Volume: Will the strong year-over-year growth in the IT segment (+36%) be confirmed? Pay attention to statements regarding the ramp-up of high-NA EUV photomasks at TSMC and Intel.

2.🏭 HDD Glass Substrate Demand (Hyperscaler Capex): Will call-off volumes for glass substrates continue to rise due to AI data center expansion? This is the second major driver in the IT sector.

3. 🤖Margin Stability in the IT Segment: Can the operating margin in the IT sector hold at the extremely high level of >54% , or will R&D costs for the next sub-2nm generations put pressure on profitability in the short term?

4.🩺 Life Care Stability Check: Will the MedTech segment maintain its steady currency-adjusted growth of ~8–9% YoY with an operating margin of just under ~18%? (Any deviation would indicate weaknesses in the end-consumer market for eyeglass lenses).

5. 💴Yen Effect (FX Tailwinds/Headwinds): To what extent does the exchange rate distort the reported JPY figures compared to organic growth abroad (85–88% of revenue generated overseas)?

My Personal Conclusion & Reaper Rating 🧐

I find that Hoya Corp. $7741 (+1,46 %) has been incredibly exciting for quite some time now. To me, the company is the textbook example of a perfect hybrid model: On the one hand, it has a virtually irreplaceable monopoly business that supplies an essential key component for the world’s most advanced semiconductors. On the other hand, the strong, defensive medtech business, with its crisis-proof margins, provides stability that excellently cushions the cyclical fluctuations of the semiconductor sector.

It’s precisely this combination that makes Hoya $7741 (+1,46 %) so extraordinary to me. The company combines enormous structural growth with a defensive quality that is extremely rare to find in this form.

Of course, Hoya $7741 (+1,46 %) still highly valued, no question about it. However, the stock has already pulled back a bit from its ATH, thereby reducing part of its ambitious valuation. For me, this currently presents an exciting opportunity to gradually build a position in a company that’s been on my watchlist for a long time 👀🙇♂️

💀Jack’s Verdict:

Jack’s Take: “If you’re looking for the perfect CRV on the stock market, sooner or later you’ll end up at HOYA. While the masses, in search of the next hype, are chasing after every shovel seller, HOYA holds the monopoly on the specialty glass from which the shovels are forged in the first place.

With the AI and high-NA EUV boom in full swing, the IT division is raking in profits thanks to >54% margin , it’s printing money like a printing press. If the semiconductor cycle stutters briefly, HOYA remains completely unfazed and continues to sell millions of eyeglass lenses, endoscopes, and cataract lenses. You’re not buying a highly speculative tech bet here, but a highly profitable, net-debt-free fortress with a built-in airbag.”

- REAPER RATING: 🟢 BUY (Quality Compounder)

- REAPER SCORE:

8/10 · Anchor 7–9 (Monopoly-like dual compounder)

@Get_Rich_or_Die_Tryin

@Tenbagger2024

@Raketentoni

@PikaPika0105

@Stocktective

@schlimmschlimm

@Multibagger

@Dividendenopi

@Simpson and, of course, all the others ✌️

+ 5

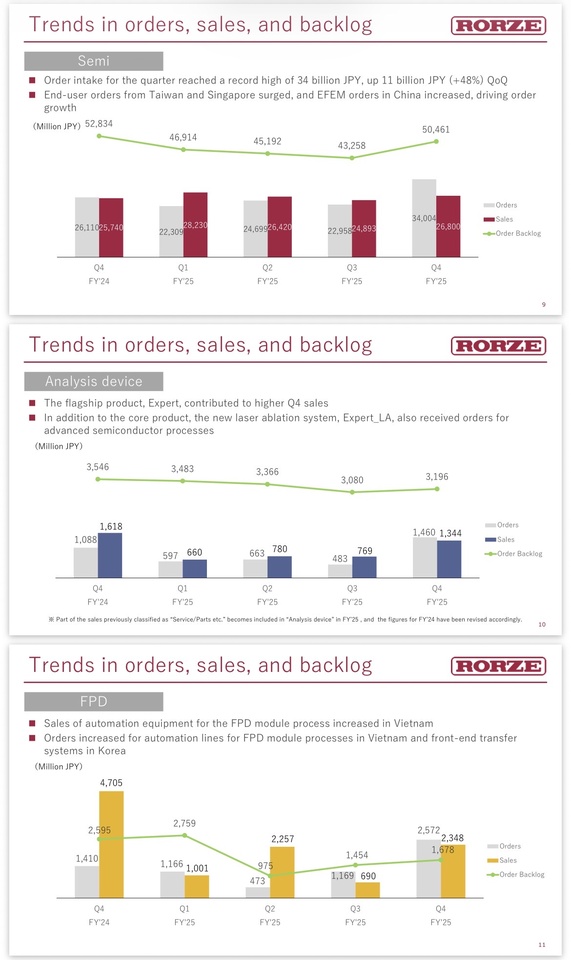

Company Profile: Rorze Corp

Hello, community,

I hope you’ve all managed to “cool off” and get through the heat over the last few days/weeks 🥵

Today, I’d like to introduce you to another company from Japan.

Today’s focus is on Rorze Corp $6323

🦾 Rorze Corp: The Indispensable Robotic Hand of the Chip Boom

Rorze Corp isn’t a traditional semiconductor developer that designs complex circuits or builds machines that etch patterns onto silicon. It is the ultimate mechanical bottleneck in global chip production. While ASML $ASML (-1 %) builds the lithography giants, Rorze masters the delicate world of contamination-free transport. Rorze builds the high-precision handling robots that must move wafers in ultra-high vacuum and under extreme cleanroom conditions—a task where the slightest error can cost billions.

1. The Business Model: The “Toll Booth” in the Cleanroom 🎢

Rorze $6323 serves as an exclusive and mission-critical supplier to the world’s most valuable factories (TSMC $2330 , Intel $INTC (-2,75 %) , Samsung $005930 ) as well as for the leading (Applied Materials $AMAT (+0,2 %) , Lam Research $LRCX (-3,35 %) ).

The mechanism: When state-of-the-art semiconductors (3 nm and below) are produced, not a single speck of dust is allowed to touch the wafer. Rorze $6323 makes its money by developing and selling atmospheric and vacuum robotic systems that transfer the wafers back and forth between individual manufacturing steps in a contactless and sterile manner.

The ingenious part: Rorze $6323 has made itself indispensable. The major chip manufacturers physically cannot operate their multi-billion-dollar factories without integrating Rorze’s automation systems. Every new chip factory worldwide—whether in Arizona, Taiwan, or Dresden—means a large automatic order for Rorze.

Recurring Cash Flows: In addition to the pure sale of outrageously expensive robotic systems, there’s a high-margin service and spare parts business. Since the robots operate continuously under extreme conditions, maintenance is a reliable cash cow.

2. Key Figures (as of July 2026) 📊

Market capitalization: approx. 850 billion JPY (approx. 5.4 billion USD).

Stock price: Currently approx. 4,940 JPY (The stock is currently surging sharply after more than doubling from ~2,400 JPY since the beginning of the year).

P/E Ratio: approx. 42–45. Due to the recent surge in the order book and the market’s revaluation, the stock is no longer a bargain, but it does reflect its massive growth potential.

Return on Equity (ROE): Outstanding ~25–28%. For a capital-intensive mechanical engineering company, this level of efficiency is absolutely staggering.

Debt: Extremely solid balance sheet. High net cash reserves protect the operating business from interest rate risks.

3. Why is this stock exciting? 🚀

✅1. An explosive surge in orders wipes out the “profit warning”: In April 2026, Rorze $6323 reportedly posted a slight decline in earnings for the past fiscal year—triggered by one-time costs related to a U.S. lawsuit and high upfront investments in its subsidiary Nanoverse. The market, however, looked deeper and saw record order intake in the fourth quarter and a forecast of 46% profit growth for the coming year. The stock subsequently shot up to the daily limit.

✅2. The Advanced Packaging Lever: Due to the AI boom, memory chips (HBM) must be stacked in extremely complex configurations. Rorzes’ U.S. subsidiary Nanoverse is developing next-gen equipment specifically for this purpose. Rorze is evolving from a mere “wafer pusher” into a key player in physical AI infrastructure.

✅3. Geopolitical tailwind: The U.S. 🇺🇸, Europe 🇪🇺, and 🇯🇵 are subsidizing the construction of local semiconductor factories with hundreds of billions. Who equips these factories is irrelevant—Rorze’s robots are needed in nearly every one of them. They win, no matter which chip manufacturer comes out on top.

✅4. A unique competitive moat through cleanroom validation: Chip manufacturers are extremely risk-averse. Once a Rorze robot is certified and validated for a TSMC production line, it’s never replaced—out of fear of production downtime. The barriers to switching are astronomical.

✅5. Index knighthood: Rorze $6323 was recently included in the prestigious JPX Prime 150 Index . This continuously attracts fresh institutional ETF and fund money to the stock.

5. Risks ⚠️

❗️Extreme dependence on the semiconductor cycle: If the tech world were to slip into a deep recession and the tech giants were to freeze their new factory construction (Capex), Rorze—as a cyclical equipment supplier—would feel the impact with a time lag, but it would hit hard.

❗️The competition never sleeps: Players such as Daifuku $6383 (+1,89 %) or Brooks Automation are also making inroads into the field of factory automation. Rorze must absolutely maintain its technological lead in the vacuum sector.

❗️Investment Rating: With a P/E ratio above 40, the potential for an earnings surge over the next 12–24 months is already largely priced in. Setbacks in the volatile semiconductor market are possible at any time.

6. Personal Conclusion & Reaper Bonus 🧐

Rorze Corp $6323 is the ultimate “shovel stock” for the global semiconductor and AI frenzy. They don’t build chips; they make production possible in the first place. Following the explosion in order volume in the summer of 2026, the market has finally realized what a gem has been lying dormant here in the Japanese small/mid-cap sector. It’s on my watch list 👀

💀Jack’s Verdict:

"If ASML builds the priceless high-tech camera for a Hollywood blockbuster, Rorze supplies the indispensable tripod: Without its vacuum robots, the entire chip production process would be thrown off balance. The market has underestimated this unassuming monopolist for years, which is why the stock is now delivering its well-deserved payoff at 4,940 JPY. Don’t be put off by the seemingly high P/E ratio of 42—as soon as the latest record orders are fully reflected in the income statement and the projected profit growth of nearly 50 percent kicks in, the valuation will shrink rapidly. Those who missed the entry point should lie in wait for the next collective semiconductor hiccup, pick up shares on the pullback, and let the robots in the cleanroom work for them."

Reaper Rating: 🔥 BUY ON DIPS (Fundamentals are extremely strong, but the chart has become overheated after the stock doubled in price).

Reaper Score:

8/10 (Quality anchor 8–9. The fundamental monopoly position deserves a 9, but the current valuation pushes the score down slightly to a well-deserved 8)

I’m curious to hear your thoughts🙇♂️

@Get_Rich_Or_Die_Tryin @Tenbagger2024

@PikaPika0105

@Raketentoni

@Multibagger

@schlimmschlimm

@Stocktective

@Dividendenopi and, of course, everyone else ✌️

+ 4

Lawsuit in the U.S.: Samsung, SK Hynix, and Micron Sued Over DRAM Prices

$HY9H (-1,13 %)

$MU (-7,98 %)

$SMSD (-0,19 %)

$005930

High memory prices for end customers have led to the first lawsuit in the U.S. On June 25, 2026, a class-action lawsuit was filed against the three industry giants—Samsung, SK Hynix, and Micron—who must now respond to the charges in a U.S. federal court in California.

Allegations: Artificial Shortages and Price Fixing

The central allegation in the lawsuit is that memory manufacturers are restricting the supply of memory for the consumer market while continuing to serve customers in the AI sector. Specifically, the complaint alleges that the memory manufacturers simultaneously reduced or even discontinued production of, for example, DDR3 and DDR4, favoring HBM and thereby limiting the availability of conventional memory, while prices rose at the same time. In doing so, they “exacerbated this so-called RAMpocalypse by fixing memory supply and prices,” the complaint further alleges.

The allegations date back to 2022. At that time, demand for DRAM was extremely low; in response, the defendants are alleged to have begun jointly coordinating and adjusting availability and prices. As a result, prices rose by about 700 percent within four years.

However, the indictment argues that in a competitive market, at least one of the three industry giants would normally have significantly increased production if prices were rising sharply—but that did not happen. Not a single one of the three manufacturers took advantage of the others’ withdrawal to win over customers; instead, all three withdrew in unison, the indictment further states.

The lawsuit consists of 17 plaintiffs, some of whom are private individuals and others small businesses, who are now represented by several law firms.

Entry into the Market Virtually Impossible for New Companies

The complaint also points out that there have been legal proceedings against the three manufacturers in the past. In some cases, judgments were even handed down; for example, Samsung and SK Hynix were ordered to pay millions, while Micron acted as a key witness and escaped punishment. The central issue at the time was price-fixing in the so-called DRAM cartel; back then, in addition to Samsung and SK Hynix, Infineon, NEC, Hitachi, Mitsubishi, Toshiba, Elpida, and Nanya were also required to pay fines, as the collusion dated back to 1998.

A thorn in the side back then—and even more so today—is that virtually no other manufacturer can succeed in entering this market. The costs are far too high, and the entire process takes a very long time, from manufacturing to customer qualification. In addition, the technologies are based on know-how built up over decades, and U.S. sanctions further complicate entry for Chinese companies, the complaint argues. The bottom line is that it is anything but easy for a new manufacturer to gain a foothold here, the complaint concludes.

The complaint seeks to “remedy the ongoing effects of the defendants’ unlawful and anticompetitive conduct,” in addition to damages, litigation costs, and attorneys’ fees. According to the current schedule, the first hearings and dates for testimony on the matter are expected to take place in September of this year.

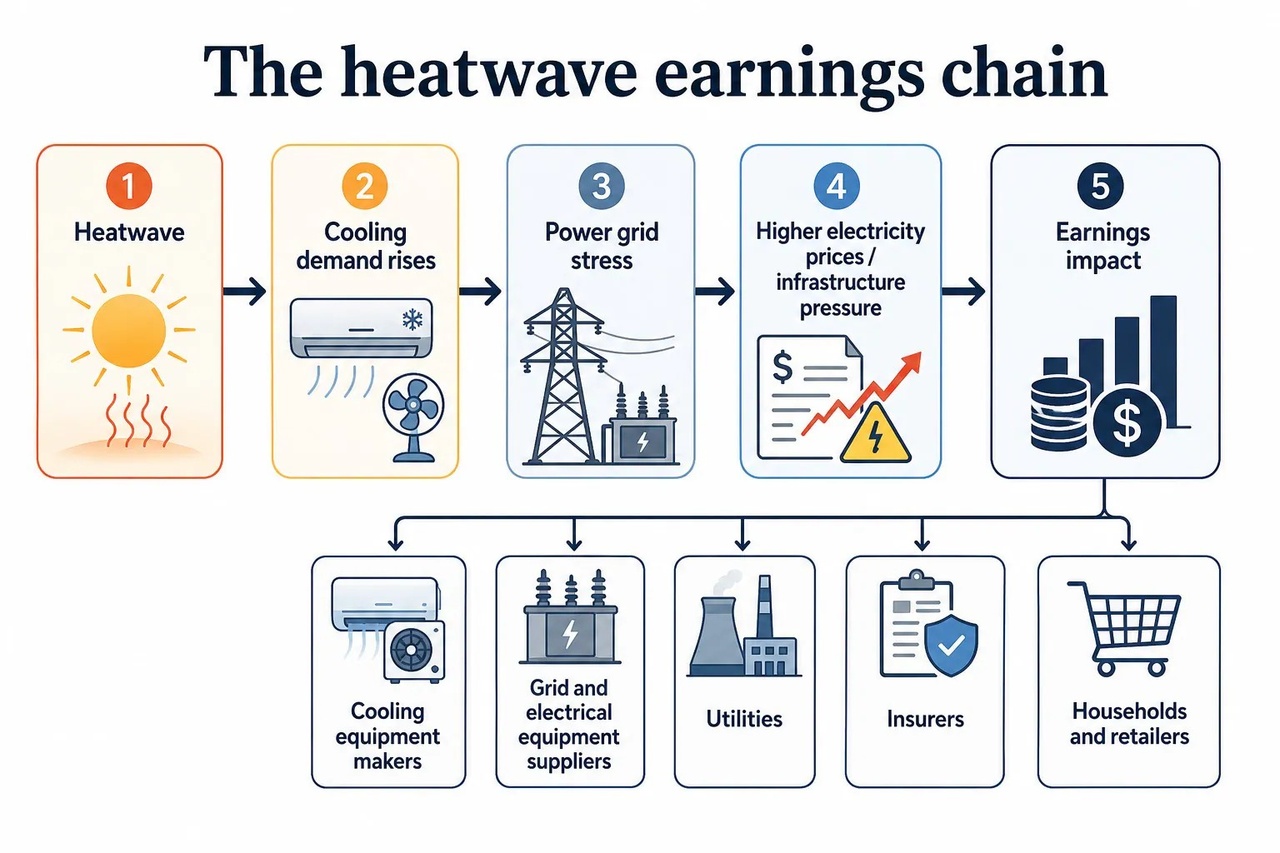

Too hot to ignore: Europe’s summer becomes a market signal

About an hour ago, I read a great article on my broker’s website here in Denmark (Saxo Bank), which I don’t want to keep from you, since I think it addresses an issue that many people may not be aware of.

Key Takeaways

- Europe’s heat wave is driving up demand for cooling and putting power grids to the test.

- The winners could include appliance manufacturers, grid equipment suppliers, and select utility companies.

- The risks lie in electricity prices, insurance claims, and the financial strain on households.

In late June 2026, Western Europe faced record-breaking heat, with countries such as France, Spain, Italy, and the United Kingdom under strain. Schools closed, traffic slowed, power systems were overloaded, and consumers rushed out to buy fans and air conditioners. Out on the streets, it’s simply unbearable. In the markets, this creates a simple chain of events: heat increases the need for cooling, cooling increases electricity consumption, electricity demand strains the grids, and grid strain alters earnings expectations.

For investors, it’s not about trading the thermometer. That’s a very small desk with a very hot seat. The point is to understand how extreme weather can translate from the weather map into revenue, costs, margins, and insurance losses.

The first winner is the power outlet The most obvious heat wave trade starts with cooling. Daikin $6367 (-1,84 %) , Samsung Electronics $005930 and LG Electronics $066570 are clear examples. Daikin is a Japanese specialist in heating, ventilation, and air conditioning (HVAC). Samsung and LG are South Korean electronics conglomerates with large divisions dedicated to home appliances. When European households realize that a south-facing apartment can turn into a small oven, demand for cooling products rises rapidly.

That doesn’t mean every summer heat wave will lead to a sustained profit boom. Portable air conditioners are often low-margin products. Supply chains can become overburdened. End-consumer demand may wane when the weather changes. But the overall trend is hard to ignore. In the past, Europe has had a lower penetration rate of air conditioning compared to many warmer regions. As hot summers become more frequent, cooling could shift from a luxury purchase to a basic comfort product.

This also explains the building perspective. Legrand $LR (+1,23 %) manufactures electrical and digital building infrastructure. Assa Abloy $ASSA B (+0,89 %) manufactures locks, doors, and access systems. Kingspan produces insulation and building materials.

These companies are not purely “heat wave plays.” They are tied to the deeper question: How can buildings become more livable, efficient, and resilient?

A good building needs more than just a larger air conditioning system. It needs better insulation, smarter wiring, efficient controls, shading, doors, ventilation, and energy management. Otherwise, Europe risks solving the heat problem by creating an electricity bill problem. Very elegant—much like fixing a leaky roof by simply buying more buckets.

The grid is becoming a bottleneck

The second part of the story is electricity. Schneider Electric $SU (+1,8 %) and Siemens Energy $ENR (+2,03 %) are right at the center of this pressure point. Schneider Electric sells equipment for energy management, automation, and energy efficiency. Siemens Energy supplies grid technology, turbines, and energy infrastructure. When power grids are confronted with higher peak loads, more renewable energy, increasing electrification, and higher cooling demand, the value of grid investments is easier to justify.

For utilities, the picture is more mixed. E.ON $EOAN (-0,94 %) and National Grid $NG. (+0,25 %) are primarily grid operators. They earn their revenue mainly through the ownership and operation of regulated electricity and gas infrastructure. Heat waves can increase investment needs, as the grids must cope with higher peak loads, localized strains, and more complex power flows. For regulated utilities, the long-term opportunity lies in the fact that investments in resilient grids can support future asset growth. Those boring power lines suddenly take center stage.

RWE $RWE (+1,26 %) , Enel $ENEL (-1,37 %) and Iberdrola $IBE (+0,98 %) have greater exposure to power generation. They own power plants and renewable energy facilities. High electricity prices can bolster the revenues of some generators, especially when supply is tight.

But heat can also be harmful. Nuclear power plants may have to curtail their output if river water becomes too warm for cooling. Low wind speeds can reduce renewable production. Droughts can impact hydropower. Gas-fired power plants can become the marginal source, meaning they dictate the price when demand is high and cheaper supply is insufficient.

So heat waves don’t simply mean “utilities win.” The details are crucial. Grid operators could benefit from the investment cycle. Generators could benefit from higher prices during certain hours, but face operational risks during others. Retail utilities could run into trouble if customers are hit with high bills and political pressure mounts. The weather may be hot, but the analysis must remain cool.

Insurance Companies Will Foot the Bill Later

The third level involves insurance companies. Munich Re $MUV2 (-0,31 %) and Swiss Re $SREN (+0,16 %) are reinsurers. Reinsurers insure insurers—which sounds like financial plumbing, because that’s exactly what it is. They help spread major risks (storms, wildfires, floods) across the system.

Heat waves can affect insurers in various ways. They can increase risks in the areas of health, agriculture, and business interruption. They can heighten the risk of wildfires. They can also expose weaknesses in infrastructure. For reinsurers, this can mean higher claims payouts in some years, but in the long run, it also leads to higher prices as risks become more visible and insurance buyers accept higher premiums.

That’s the strange logic of insurance: Bad weather hurts in the short term, but it supports better pricing later on. The umbrella industry doesn’t like storms, but storms remind everyone why umbrellas cost money.

Risks to Keep an Eye On

- Investors might overreact to a hot summer.

- Political risks: High electricity prices can trigger government intervention (excess profit taxes).

- Cost risks: Grid expansions, cooling equipment, insulation, and insurance all cost money. Customers might push back if household budgets are already stretched thin.

The Bottom Line Under the Sun

The “heat wave trade” isn’t about guessing next week’s temperature. It’s about recognizing where resilience translates into revenue, where strain leads to costs, and where the old European assumption of mild summers is no longer a reliable forecast. In the markets, just as in homes in July, heat is rarely dispelled simply by ignoring it.

Source: Saxo Bank / Saxo Trader – Ruben Dalfovo, Investment Strategist

and, of course, everyone else :)

I definitely know that I’ll be investing in an air conditioner for next season 😵💫🔥🔥. I took a look yesterday, but right now the units I need are basically all sold out or won’t be available for a long time. With this heat, I can barely think straight.

There are some interesting stocks in your portfolio, but right now I’m only invested in $MUV2 —and quite heavily there.

I got my fingers badly burned with the utilities (electricity) a very long time ago. Back then, I thought electricity would always be needed—and in increasing amounts. Then came the politically mandated phase-out of nuclear and coal power, and I ended up taking a big hit. My E.ON $EOAN and RWE $RWE investments completely tanked back then; only CEZ $CEZ, which was based abroad, fared better.

For my new foray into the utilities sector, I’m now focusing on water and building a position in Veolia $VIE. I expect this to be a good investment in the medium and long term—especially because water and wastewater networks, including supply lines and treatment plants, etc., exist only once in each locality. Therefore, I don’t really see the kind of competition here that exists among electricity providers.

Semiconductor and memory shares 1-month performance 📈

Which ones are you invested in?

+107% Intel $INTC (-2,75 %)

+92% Credo Techn. $CRDO

+91% Astera Labs $ALAB (-2,19 %)

+73% MediaTek $2454

+72% AMD $AMD (-2,55 %)

+72% Seagate $STX (-1,6 %)

+71% SanDisk $SNDK (-8,73 %)

+67% KIOXIA $285A (-9,34 %)

+66% ON Semiconductor $ON (-3,33 %)

+61% STMicroelectronics $STM (-0,66 %)

+55% Marvell $MRVL (+0,01 %)

+51% NXP $NXPI (-7,11 %)

+49% Siltronic $WAF (+3,63 %)

+47% GLOBALFOUNDRIES $GFS (-0,85 %)

+47% SK Hynix $000660

+47% Micron $MU (-7,98 %)

+46% Infineon $IFX (+3,74 %)

+45% Western Digital $WDC (-0,89 %)

+43% Texas Instruments $TXN (-1,43 %)

+42% Arm Holdings $ARM (-2,83 %)

+41% QUALCOMM $QCOM (-2,98 %)

+41% Monolithic Power $MPWR (-4,22 %)

+40% Aixtron $AIXA (+2,63 %)

+40% Microchip Techn. $MCHP (-1,97 %)

+34% Broadcom $AVGO (+0,03 %)

+30% Skyworks $SWKS (+2,41 %)

+25% Samsung Electronics $005930

+24% Analog Devices $ADI (-0,06 %)

+18% TSMC $TSM (-0,21 %)

+16% Lam Research $LRCX (-3,35 %)

+14% KLA $KLAC (-0,3 %)

+13% NVIDIA $NVDA (+2,15 %)

+10% Applied Materials $AMAT (+0,2 %)

+9% ASML $ASML (-1 %)

I have AMD. Which one do you have?

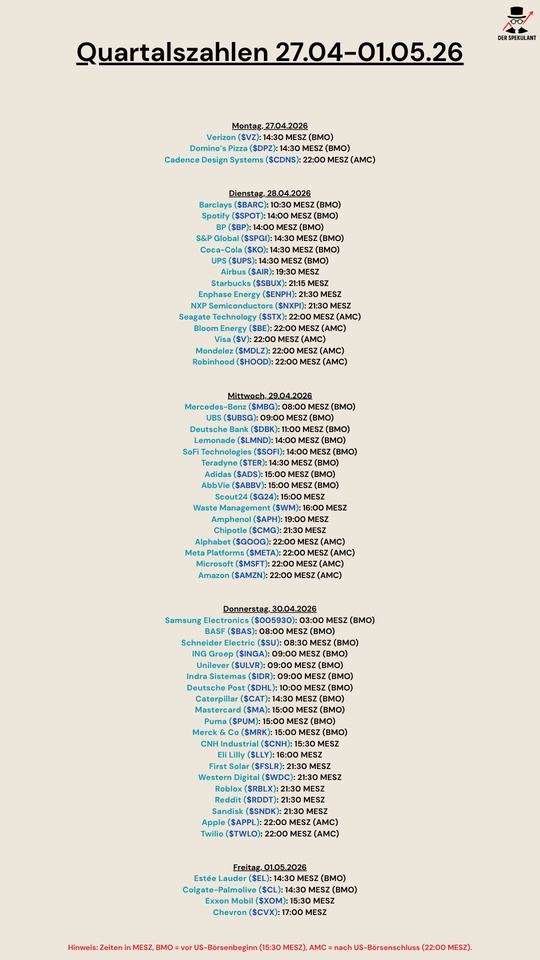

Quarterly figures 27.04-01.05.26

$VZ (-0,1 %)

$DPZ (-1,31 %)

$CDNS (+2,14 %)

$BARC (-0,73 %)

$SPOT (-4,04 %)

$BP. (+1,96 %)

$SPGI (+0,17 %)

$KO (+0,1 %)

$UPS (+0,13 %)

$AIR (-0,78 %)

$SBUX (-0,79 %)

$ENPH (+0,43 %)

$NXPI (-7,11 %)

$STX (-1,6 %)

$BE (-3,13 %)

$V (+0,06 %)

$MDLZ (-1,1 %)

$HOOD (-0,69 %)

$MBG (-1,09 %)

$UBSG (-1,19 %)

$DBK (-0,5 %)

$LMND (+0,47 %)

$SOFI (-1,1 %)

$TER (-1,58 %)

$ADS (+0,95 %)

$ABBV (-2,62 %)

$G24 (-3,32 %)

$WM (-0,03 %)

$APH (+0,48 %)

$CMG (-3,14 %)

$GOOG (+6,42 %)

$META (+2,62 %)

$MSFT (+3,6 %)

$AMZN (+6,74 %)

$005930

$BAS (-1,34 %)

$SU (+1,8 %)

$INGA (+0,96 %)

$ULVR (-2,04 %)

$IDR (+0,37 %)

$DHL (+0,56 %)

$CAT (-0,31 %)

$MA (+0,34 %)

$PUM (-2,66 %)

$MRK (+0,04 %)

$CNHI (-1,22 %)

$LLY (-0,1 %)

$FSLR (-0,49 %)

$WDC (-0,89 %)

$RBLX (-17,16 %)

$RDDT (-14,39 %)

$SNDK (-8,73 %)

$AAPL (-2,89 %)

$TWLO (+3,59 %)

$EL (-0,38 %)

$CL (-0,05 %)

$XOM (-0,25 %)

$CVX (+2,08 %)

Mercedes could hurt...

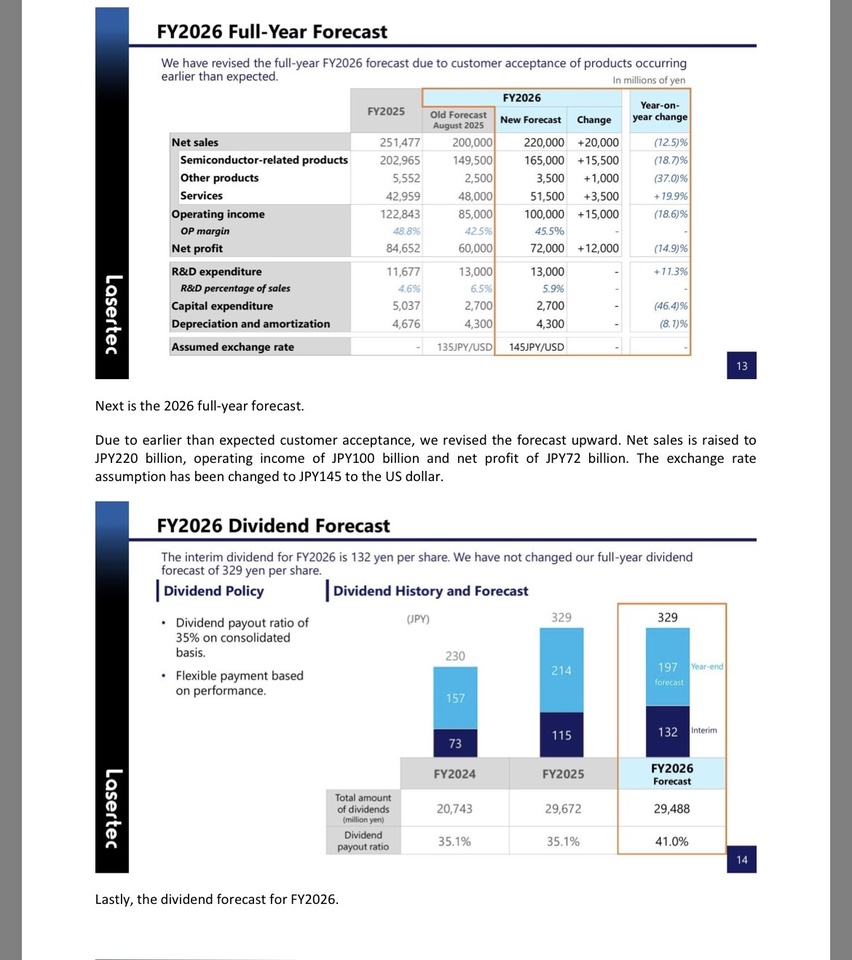

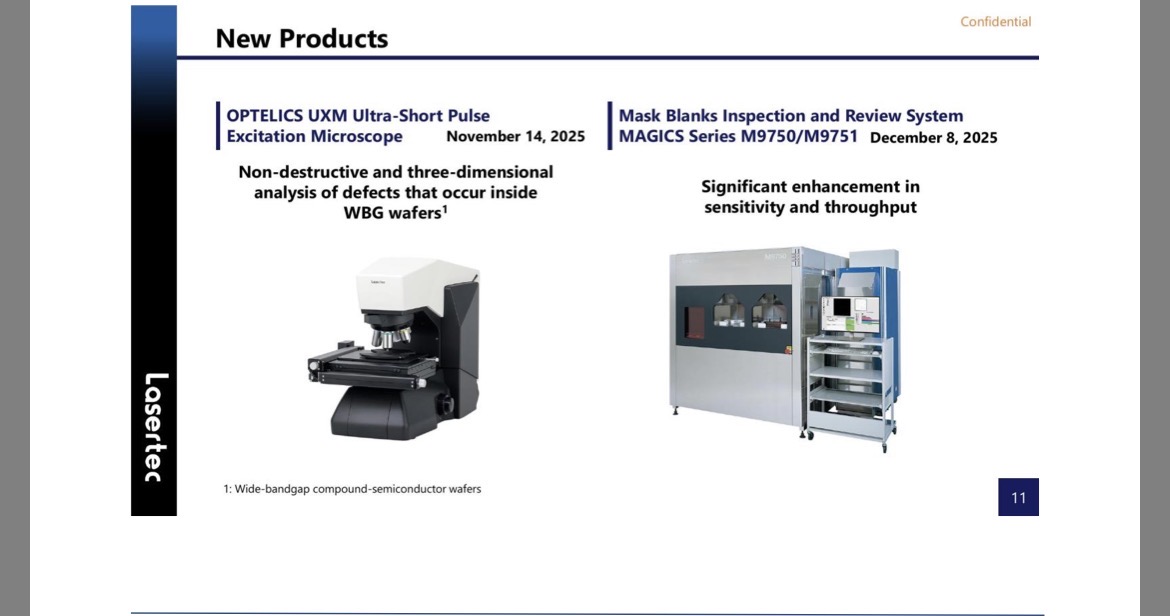

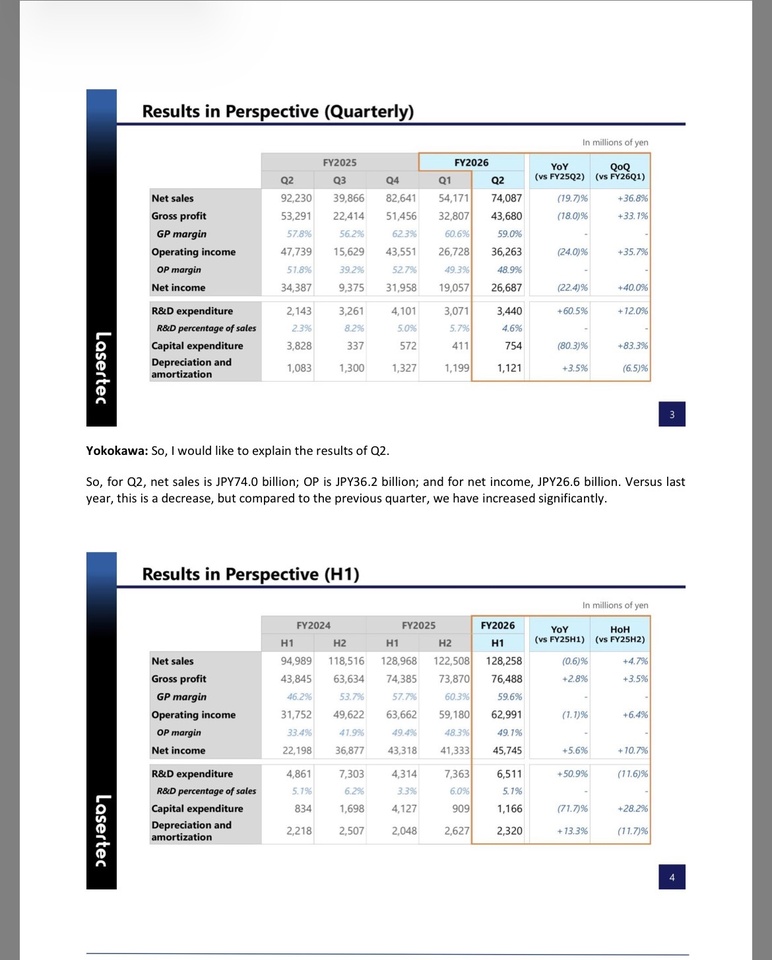

Company presentation: Lasertec Corp

While Juan von lieben @Tenbagger2024 left Japan on his way to Norway, I stayed in Japan and would like to introduce you to another company from my watchlist in the semiconductor sector.

Today we are talking about Lasertec Corp $6920 (-0,74 %)

Lasertec Corp $6920 (-0,74 %) 👀The eye of the semiconductor revolution

Lasertec $6920 (-0,74 %) is no ordinary chip supplier. It is the only company in the world capable of testing the extremely complex masks for EUV (Extreme Ultraviolet) lithography. Without Lasertec $6920 (-0,74 %) there would be no iPhones, no high-performance AI servers and no progress in 2nm chips.

1. the business model: "The Monopoly Gatekeeper" 🔬

Lasertec $6920 (-0,74 %) operates in a technological stratosphere in which there is hardly any competition.

- The EUV lever: ASML $ASML (-1 %) builds the exposure machines. But before a mask (the "negative" of the chip) goes into the machine, it has to be checked for atomic defects. Lasertec $6920 (-0,74 %) has a market share of almost 100% for certain market share of almost 100 %💯

- Actinic Inspection: Lasertec uses the same EUV wavelength for inspection as the exposure machine itself. This "Actinic" technology is extremely difficult to copy and forms the ultimate technological moat.

- Service revenues: As the machines are highly complex, Lasertec generates massive revenues through maintenance and software updates over the entire life cycle (10-15 years).

Deep Dive: Lasertec - The physical frontier of semiconductor manufacturing

1. the technological "miracle": Actinic EUV Inspection

To understand why Lasertec $6920 (-0,74 %) has a monopoly, you have to look at EUV lithography lithography. At wavelengths of 13.5 nanometers (EUV), light behaves extremely difficult: it is absorbed by almost all materials, even air. This is why the entire process takes place in a vacuum.

- The problem: Conventional inspection devices use deep ultraviolet light (DUV). However, DUV does not "see" certain defects on an EUV mask because the mask behaves differently under EUV light (phase jumps, reflections).

- The Lasertec solution (ABICS series): Lasertec $6920 (-0,74 %) was the first and so far only company to develop a light source that uses EUV light for inspection (hence "Actinic" - under real working conditions). They shoot EUV photons at the mask and analyze the reflected image.

- The moat: Mastering this light source and the optics that direct EUV beams without significant losses is a feat of physics. Competitors rely on electron beam technology (e-beam), which is precise but 10 to 100 times slower. slower than the light process from Lasertec $6920 (-0,74 %)

2. the growth pillar: AI chips & sub-2nm era

- Next generation (GAA): The transition to new transistor structures (Gate-All-Around) requires even more precise masks. Lasertec has already completed the systems for 2nm production (planned from the end of 2025/2026).

- Semiconductor sovereignty: As the USA, Japan and Europe are building their own chip factories (fabs), each new location must order Lasertec machines. The company benefits from the global subsidy race.

2b. The "GAA cycle" (Gate-All-Around) - the next share price driver

We are currently in the transition from FinFET transistors to GAA transistors (for 2nm and below).

- Complexity explosion: With GAA structures, the chip designs are so delicate that the masks are even more susceptible to the smallest impurities.

- Higher inspection rate: It used to be enough to randomly inspect a mask. With 2nm AI chips, the mask must be after each exposure cycle (reticle cleaning) in order not to jeopardize the yield. This massively increases the number of Lasertec machines required per factory.

3 The "hidden" risks (bear-case deepening)

- Concentration risk: As only three companies (TSMC $2330 Samsung $005930 Intel $INTC (-2,75 %) ) operate real high-end EUV fabs, Lasertec is extremely dependent on the investment decisions of these three giants.

- Politics: Japan has tightened export restrictions on high-end chip equipment to China. Lasertec is losing part of the market as a result, but is compensating for this with the boom in the USA and Japan itself.

3. the hard facts (key figures 2025/26) 📊

- Market capitalization: approx. 2.8 - 3.1 trillion. JPY (approx. 19-21 billion USD).

- Profitability: An operating margin of over 35 % and a return on equity (ROE) of often over 45 %. These are figures that are normally only achieved by software companies.

- Cash position: Lasertec $6920 (-0,74 %) is virtually debt-free and finances all of its research from current cash flow.

Lasertec $6920 (-0,74 %) has experienced explosive profit growth in recent years, driven by the roll-out of High-NA EUV technology.

- Turnover (forecast 2026): approx. 240 - 250 billion JPY (A massive jump from approx. JPY 153 bn in 2023).

- Operating margin: This is constant at 35 % to 40 %. By way of comparison, a traditional mechanical engineering company such as DMG Mori is often at 8-10 %. Lasertec $6920 (-0,74 %) plays in a league of its own.

- Net profit: Expected for 2026 approx. JPY 66 - 70 billion.

- R&D ratio (R&D): Lasertec invests approx. 10-12% of the turnover directly into research. This is its protective shield against the competition.

2. the strength of the balance sheet

The company has an extremely "clean" and conservative financial position:

- Equity ratio: Is a phenomenal ~50 % to 60 %.

- Net cash position: Lasertec $6920 (-0,74 %) has no significant bank debt. On the contrary: they are sitting on high cash balances, which they are using to finance the pre-production of the extremely expensive EUV mask testing devices.

- Stocks (inventories): An important indicator at Lasertec! Inventories are often very high (currently around JPY 100+ billion). This is positive: These are machines already in progress, for which customers (TSMC $2330 /Intel $INTC (-2,75 %) ) have already been received.

3. profitability - the "magic numbers"

- ROE (return on equity): Mostly over 45 %. This means that Lasertec $6920 (-0,74 %) works extremely efficiently with the shareholders' money.

- ROIC (return on invested capital): Is often over 30 %. This shows that every yen coin invested in the development of new machines yields an extremely high return.

The "moat" in the balance sheet: order backlog

At Lasertec $6920 (-0,74 %) looks less at past sales and more at the order backlog. order backlog:

- This is currently at a record level (well over JPY 400 billion).

- Significance: Lasertec $6920 (-0,74 %) is effectively booked for the next 2 years is effectively booked out. Even if the global economy weakens slightly tomorrow, the chip giants will have to reduce their orders in order not to be left behind in the technological race.

4. why is the share exciting? (Bull case) 🚀

1. Irreplaceability: There is no "switching" to a competitor product. Anyone who builds state-of-the-art chips must buy from Lasertec.

2. AI growth: As AI chips become larger and more complex, the susceptibility of masks to errors increases - and with it the need for Lasertec test equipment.

3. Efficiency: The company has an extremely lean organization. A small workforce generates billions in turnover.

⚠️ RISKO (Bear-Case)

"The perfection trap

- Valuation risk (P/E ratio 50+): The market is pricing in a "perpetual monopoly". If growth falls from 30 % to 15 %, there is a risk of a massive contraction in the multiple - the share price could correct due to the valuation alone, even if profits continue to rise.

- Concentration risk: Over 70% of sales are attributable to just three customers (TSMC $2330 Intel $INTC (-2,75 %) , Samsung $005930 ) If Intel $INTC (-2,75 %) postpones its 2nm roadmap, Lasertec will immediately feel the impact on its books.

- Technological attack: US giant KLA Corp $KLAC (-0,3 %) is working flat out on competing e-beam technologies. As soon as the monopoly becomes a duopoly, margins shrink.

- Geopolitics & currency: Export restrictions to China and a possible appreciation of the yen (JPY) are unpredictable "black swans" for the Japanese export pearl.

🛡️ EARNINGS-PREP: LASERTEC $6920 (-0,74 %)

Timing: Thursday, 04/30/2026 (JST) - Q3 results.

This is the moment of truth. Lasertec $6920 (-0,74 %) raised its guidance in January and the share price has risen like a rocket since then (~€242 / JPY45,000). Now the company has to deliver to justify the valuation of P/E 51.

1. date & consensus (what the market expects)

- Date: April 30, 2026

- Revenue (consensus): ~ JPY46.07bn (+15.6% YoY)

- EPS (consensus): ~JPY175.76 (+69% YoY)

- FY 2026 Guidance (Revised): Revenue JPY 220 bn | Op. profit JPY 100 bn.

2. CORE METRICS

- Order backlog (order backlog): This is the most important figure. The backlog recently stood at ~297bn JPY. As sales are expected to decline as planned in FY26 (-12.5% YoY), the order intake show that the recovery for 2027 is already rolling.

- High-NA EUV Adoption: Watch for comments on Intel's and TSMC's high-NA plans. Lasertec is the sole bucket-wheel excavator here. Delays at chipmakers = poison for Lasertec.

- MATRICS X712 series: The new system was launched in March 2026. Initial comments on customer feedback are critical for momentum.

5th evaluation & conclusion (April 2026)

- P/E ratio (P/E ratio): Currently approx. 51x.

- History: This is moderate compared to previous years (where the P/E ratio was often 60x to 80x) moderate.

- Verdict: The balance sheet is "bulletproof". The risk at Lasertec is not bankruptcy or over-indebtedness, but merely the market's high expectations for future growth.

💀REAPER-BONUS :

🛡️ LASERTEC CORP (6920.T) - SUMMARY

Status: World monopolist for EUV mask inspection (sub-3nm chip production).

1. DNA & QUALITY (The foundation)

- Moat: 🟢 ELITE. Lasertec has a 100% monopoly on inspection systems for EUV masks. Without them, the assembly lines at TSMC, Intel and Samsung for high-end chips (AI chips, iPhone CPUs) stand still.

- Margins: Operating margins of almost 50% and an ROIC of over 40%. This is absolutely world class and shows the enormous pricing power.

- Balance sheet:

Net cash. The company has no debt and is sitting on massive cash reserves. Interest rate risks? Zero.

2. the valuation fallacy (the price)

- Current price:

~242 € (~45,000 JPY).

- P/E ratio (fwd): ~51x. The market is pricing in perfection. Historically, the P/E ratio is at the upper limit.

- Growth expectation: The share price implies sustained FCF growth of over 22% p.a. for the next 10 years. That is ambitious, even for a monopolist.

3 CATALYST-WATCH (The next spark)

- Date:

30.04.2026 (Q3 Earnings).

- Whisper: Expectations are extremely high (AI hype). An "in-line" (expectations fulfilled) could already lead to profit-taking here, as the share price has run massively in the run-up.

⚖️ REAPER RATE

RATING: WATCH

Lasertec $6920 (-0,74 %) is qualitatively a 10/10but in terms of rating a 3/10.

- Dust-off limit: 205 €. This is the fundamental bottom (fair value), where the risk/reward profile becomes attractive again.

Jack's conclusion: "A monopoly protects you from competition, but not from an inflated valuation. Buying at €242 is betting that there won't be a single delay in global chip production. I'll stay on the sidelines and wait for the setback."

In this sense, have a nice weekend

@Tenbagger2024

@Get_Rich_or_Die_Tryin

yours Aktienhauptmeister✌️

+ 5

Barely visible, but indispensable: NAND memory

$285A (-9,34 %)

$MU (-7,98 %)

$WDC (-0,89 %)

$005930

The amount of data is growing rapidly and so is the demand for NAND memory. Kioxia supplies it.

From Toshiba heir to global memory player

Kioxia is a highly specialized provider of memory technology. The company emerged from Toshiba's former memory division and is now one of the global key players in the NAND flash market.

NAND flash memory is indispensable today because it stores large amounts of data quickly, energy-efficiently, permanently and without mechanical parts in a space-saving manner. This is precisely what makes it the standard solution in smartphones, laptops, data centers and industrial applications.

The business model is clearly structured: Kioxia does not sell end devices, but rather versatile components.

The product portfolio can be divided into two main areas. Firstly, pure memory chips, such as SLC, MLC, TLC or QLC NAND. These differ in terms of how many bits are stored per memory cell, and therefore in terms of cost, speed and service life. SLC stands for high reliability and is used in industrial or automotive applications, for example, where data integrity is crucial.

Secondly, ready-made memory solutions such as SSDs or embedded memory (eMMC, UFS), which are integrated directly into end devices.

The company's own 3D flash architecture BiCS FLASH is particularly relevant in terms of technology. Here, memory cells are stacked vertically, which massively increases capacity and reduces costs at the same time.

This is particularly relevant for data centers.

Oligopoly with AI booster

Furthermore, the NAND flash market is a global oligopoly. The reason for this lies in the extreme barriers to entry. Setting up modern semiconductor production costs tens of billions. At the same time, the development of memory technology requires decades of experience, in-depth process expertise and close integration of research and production. New competitors have virtually no chance of overcoming these hurdles in the short term.

Added to this are economies of scale. Memory chips are a mass business with strong price competition. Those who do not produce in huge volumes have no chance in competition. This leads to a natural concentration on a few global players.

In this environment, Kioxia is part of a small leading group. Its biggest competitor is Samsung Electronics. Followed by SK Hynixwhich has gained significant weight through the acquisition of Intel's NAND business, and Micron Technology. Western Digital also plays an important role and is closely linked to Kioxia through joint production structures.

All of these companies are currently recording significant increases in profits, driven primarily by the enormous demand for AI hardware.

This has paid off

The Börsengang of Kioxia has therefore proved to be a stroke of luck and has paid off for shareholders. But this could be just the beginning of a success story.

Growth momentum has increased significantly in the first nine months of the current financial year (3/2026). Sales increased by 80% to 1,360 billion yen, which led to a 72% increase in profit to 252 million yen.

This corresponds to a turnover of 7.31 billion euros and a profit of 1.35 billion euros.

Kioxia is expected to present its figures for the final quarter on May 15. It is currently expected that profit will increase by 80% to 932 yen per share. Kioxia therefore has a KGV of 32.7.

At first glance, the share does not look like a bargain. However, as already mentioned, the industry is at a crucial point. Demand is outstripping supply, which has led to full capacity utilization in production and rising prices.

At the same time, a massive expansion of production is underway to keep up with demand.

As a result, Kioxia's profit is likely to roughly quadruple in the current financial year. According to consensus estimates, earnings will rise by 397% to JPY 4,600 per share.

Should this happen, the P/E ratio would fall to 6.6

Kioxia share: Chart from 10.04.2026, price: JPY 30,350 - symbol: 285A | source: TWS

The share is therefore currently unstoppable and from a fundamental perspective there is little to prevent the rally from continuing. The biggest Risiko are the typical price cycles in this sector. NAND flash is largely standardized. When supply and demand collapse, prices often fall dramatically.

Source:

Podcast episode 138 "Buy High. Sell Low." Iran war winners and losers, buy the dip, oil.

Subscribe to the podcast so that there will soon be peace.

00:00:00 Oil and government bonds

00:37:50 Liberty Energy $LBYE

00:48:30 Cheniere Energy $LNG (+3,49 %)

00:56:35 Kinder Morgan $KMI (+1,68 %)

01:00:52 Iran war losers / Buy The Dip

01:19:20 Bitcoin

Spotify

https://open.spotify.com/episode/7jouQHLiEbfg5QGyZOdZWJ?si=Du2whTFIR7WOE8AFD1RICA

YouTube

Apple Podcast

$TKA (-0,47 %)

$SZG (+1,72 %)

$SZGPY (+2,36 %)

$HLAG (+1,6 %)

$VNA (-0,02 %)

$CCL

$AAL (+0,14 %)

$SMSD (-0,19 %)

$005930

$CONTININS

$TUI1 (+1,22 %)

$IFX (+3,74 %)

$MC (+0,78 %)

$BA (-1,75 %)

$2330

$CCO (-2,68 %)