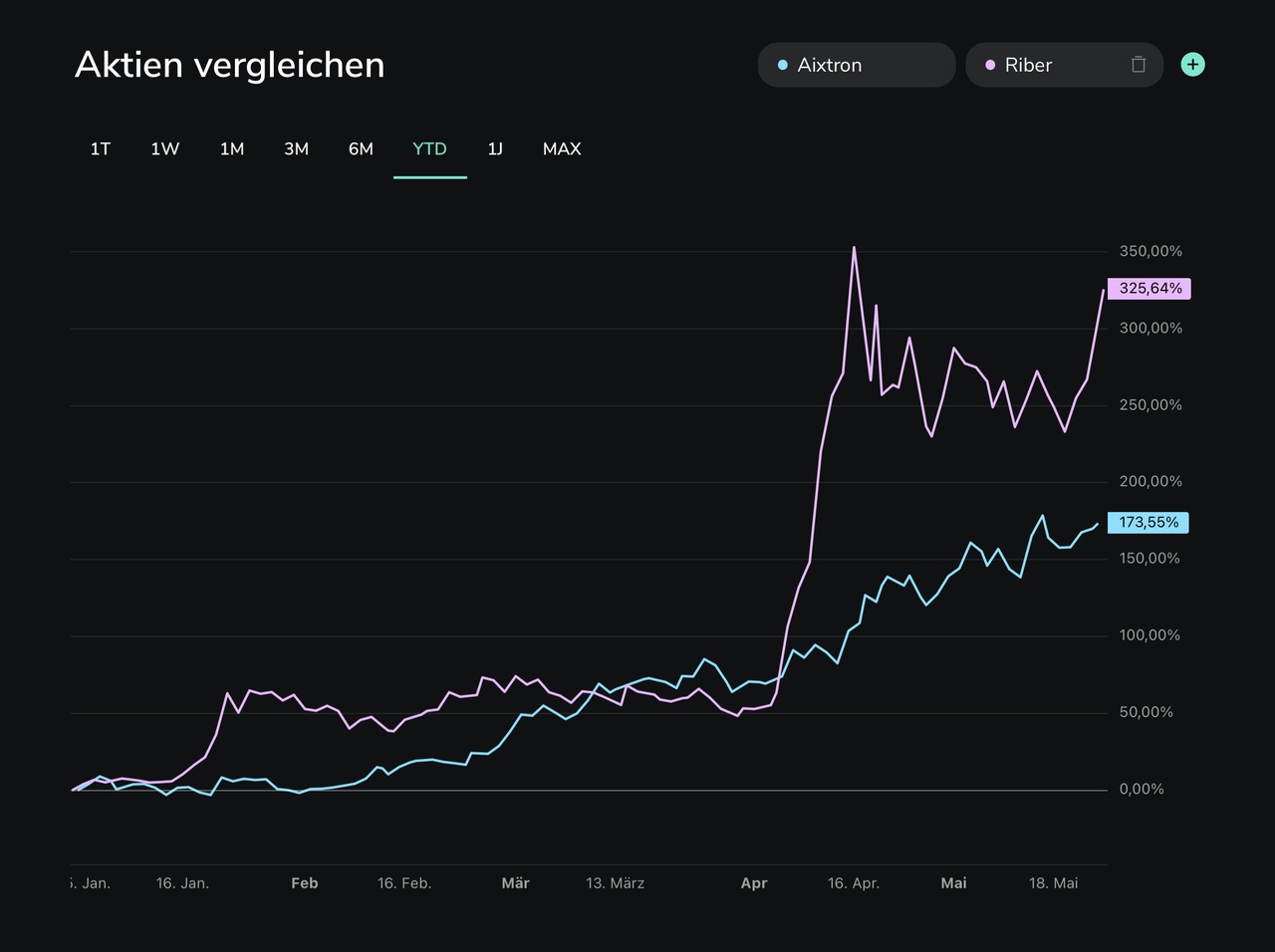

I'm also staying invested in AIXTRON!

The Aixtron SE benefited from strong order intake in the second quarter of 2026, which rose by 81 percent to 214.5 million euros. Over the first half of the year, orders totaled 386.0 million euros, an increase of 54 percent compared to the 250.7 million euros reported in the previous year. According to the equipment manufacturer, this growth was driven by high demand for systems for optoelectronic applications, which accounted for around 75 percent of equipment orders received in the second quarter. Consequently, the order backlog climbed to 456.9 million euros as of June 30, 2026, up from 284.6 million euros a year earlier and 257.8 million euros at the end of 2025. Larger laser system deliveries are scheduled to begin in the third quarter of 2026.

In contrast, the still-weak first half of the year is reflected in current operations. Revenue fell by 30 percent in the first half to 174.5 million euros, down from 249.9 million euros, but was in line with expectations. Operating income slipped to minus 7.6 million euros, down from plus 26.9 million euros, which Aixtron attributes primarily to lower production volumes, compounded by one-time costs from a workforce reduction in the first quarter. In the second quarter alone, however, EBIT returned to positive territory at 14.7 million euros. Net income for the first half of the year was minus 2.8 million euros, while in the second quarter it was plus 19.1 million euros, supported by deferred tax income from prior-year losses.

“The first half of 2026 marks an important turning point for Aixtron. The strong order momentum in optoelectronics provides high visibility for the upcoming production ramp-up. At the same time, the convertible bond and our planned production site in Malaysia increase our financial and operational flexibility. This has positioned the company well to fully capitalize on the accelerating wave of demand in optoelectronics. At a later stage, power electronics will also pick up again and contribute to revenue growth,” says Felix Grawert, CEO of Aixtron SE.

Cash Flow Figures at Aixtron Significantly Improved

Cash inflows for the Herzogenrath-based company near Aachen have improved significantly. Operating cash flow nearly doubled in the first half of the year to 172.7 million euros, while free cash flow rose to 162.1 million euros, up from 71.1 million euros. This was primarily driven by higher customer prepayments, which are helping to finance the upcoming production ramp-up. In addition, Aixtron placed convertible bondsAnleihen over 450 million euros. As a result, cash and cash equivalents rose to 816.2 million euros, up from 224.6 million euros at year-end, while net financial assets totaled 467.0 million euros. As a result of the bond issuance, the equity ratio fell to 61 percent, down from 88 percent.

Aixtron is sticking to the forecast it raised on April 14, 2026. For the full year, the TecDAXGroup expects revenue of 560 million euros, with a range of plus or minus 30 million euros, a gross margin of around 42 percent, and an EBIT margin of 17 to 20 percent. For the third quarter of 2026, Aixtron forecasts revenue of 180 million euros, with a range of plus or minus 20 million euros. According to the company, this outlook is supported by the robust order book in optoelectronics and the start of major system deliveries in the second half of the year. The production ramp-up is proceeding according to plan, and Aixtron has also begun groundwork for its new site in Penang, Malaysia.

Aixtron füllt die Auftragsbücher dank Optoelektronik-Boom | 4investors.de