Reckitt Benckiser $RKT (+0,64 %) just hit 52-week lows. The market is panicking over a Q1 sales miss driven by a weak flu season tanking Mucinex demand, European sales dropping, higher oil prices pressuring margins, and the ongoing Mead Johnson litigation overhang.

It looks ugly in the headlines. But here is what the math engine shows today:

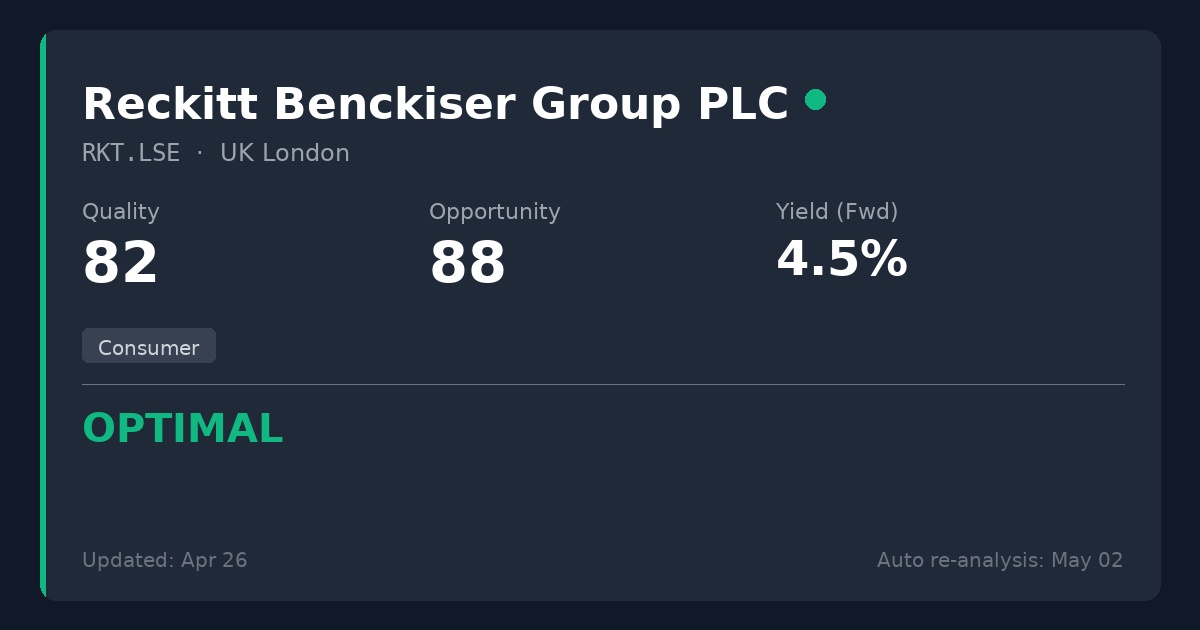

- Quadrant: 🟢 OPTIMAL

- Quality Score: 82/100

- Opportunity Score: 88/100

- P/E: 9.8x (historic low for the owners of Lysol, Dettol, and Finish)

- Yield: 4.4% (backed by a highly conservative 61% free cash flow payout)

The motor flagged this as a "Temporary Problem". It isolates the fact that acquiring dominant consumer staple brand equity at a single-digit multiplier is a rare dislocation. Short-term headwinds and lawsuits are masking highly resilient cash flows.