Coca-Cola $KO (-0,85 %) is in the top 10 of my largest positions with 2.5% of my portfolio. Therefore, here is my classification of the Q1 report [1] and earnings call [2].

Coca Cola is a classic in the portfolio for many, stable dividend, well-known brand, global presence.

The Q1 figures look strong. But as always: don't just look at the headline figures, but understand what's behind them.

How often do I start with one... two. explanations.

1. what does "reported" vs. "adjusted (non-GAAP)" mean?

Companies often publish two versions of their figures:

- Reported (GAAP): The official, correct figures according to US accounting standards

- Adjusted (non-GAAP): Figures excluding one-off effects such as special items, depreciation and amortization, sales, etc., i.e. the "normal" operating business

➡️ Example: Coca-Cola made a large one-off payment for Fairlife in 2025. The adjusted key figure shows how the business is performing without this one-off effect.

➡️ Non-GAAP = "not adjusted in accordance with accounting law, but economically meaningful"

2. the Q1 in figures

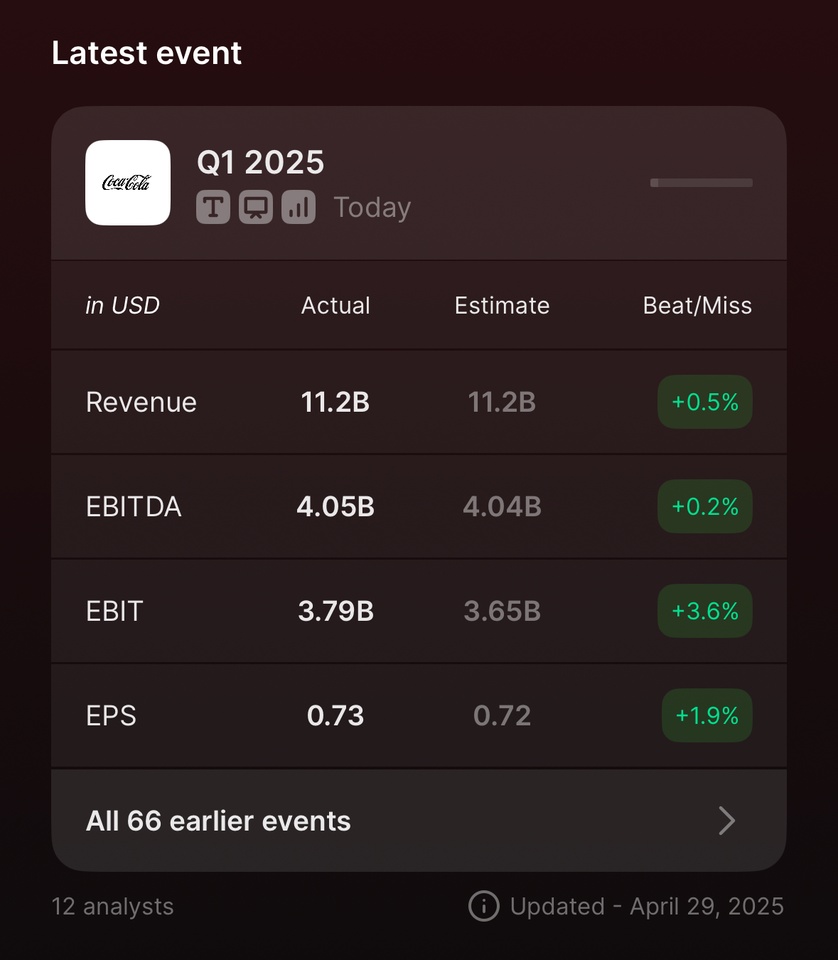

📊 ESTIMATES VS. REPORTED

Revenue (reported): $11.1 billion (-2 %)

- Decline due to currency effects & disposal of bottling plants...

EXCURSES:

In recent years, Coca-Cola has sold many of its own bottling plants to independent partner companies, a process known as "refranchising".

Why?

- Coca-Cola wants to focus more on brand management, formulation and marketing, not on expensive production and logistics.

- The bottlers take over production, packaging and distribution, while Coca-Cola collects license fees and sells concentrates.

What does this mean for the figures?

- When Coca-Cola sells a bottling plant, its turnover is removed from the balance sheet, which can reduce reported turnover, even if the business is doing well.

- Organic sales are therefore adjusted to show how the core business is really developing.

➡️ Declines in sales due to the sale of bottling plants are not a bad sign, but part of a long-term strategy.

Organic sales: +6 %

- Currency & structure-adjusted - shows real growth

Earnings per sharee (EPS, reported): $0,77 (+5 %)

- Net earnings per share, including special effect

Earnings per share (EPS, adjusted): $0,73 (+1 %)

- Shows the adjusted operating earnings per share

Operating profit: +71 %

- Looks hefty, but is due to the special effect from Q1 2024

Operating margin: 32.9 % (previous year: 18.9 %)

- Huge jump due to elimination of fairlife amortization

Adjusted operating margin33.8% (previous year: 32.4%)

- Significantly more stable, that is the really relevant comparison

Sales volume (unit case volume): +2 %

- Important key figure, shows whether people are also drinking more

CALL:

CEO James Quincey describes the current environment as "dynamic, with geopolitical tensions and fluctuating consumer sentiment". Nevertheless, he emphasizes:

"Our first quarter results show that our all-weather strategy is working. We are delivering organic growth and a higher operating margin, despite difficult conditions."

➡️ Coca-Cola presents itself as a robust crisis player with a focus on agility, consumer proximity and local execution.

3. what does "unit case volume" mean and why is it so important?

Coca-Cola measures actual beverage consumption via the unit case volume, i.e. the quantity sold in standardized units.

➡️ Important because it shows whether Coca-Cola is really selling more products, regardless of price.

➡️ This volume increased by +2 %, driven by India, China & Brazil, countries with a growing middle class, increasing demand and great growth potential in out-of-home consumption.

4. price mix: more than just price increases

+5 % price-mix growth means:

- Higher prices in the market

- Better mix (e.g. smaller cans at higher prices, premium products)

- Regional shifts (e.g. more sales in high-price regions)

➡️ This strategy ensures growth even if unit sales stagnate.

5. product insights:

Growth stars:

- Coca-Cola Zero Sugar: +14 %, clear megatrend!

- Water, tea: +2-3 %

Weaker:

- Coffee (-2 %), mainly affects Costa Coffee and vending machines

- Sports drinks (-1 %), such as Powerade & BODYARMOR

6. regions at a glance

🌍 Europe, Middle East & Africa (EMEA):

- Sales +3 %, Coca-Cola & Fanta performing strongly

- Price/mix +6 %

❗ Currency impact -9 %, many local currencies (e.g. Turkish lira, African markets) lose against the dollar

➡️ in case you were also wondering why exactly these regions are grouped together? Operational management at Coca-Cola runs via regions with comparable logistical markets, not a geographical coincidence.

🌎 Latin America:

- Organic sales +13 %

- Adjusted operating profit: +18 %

❗ Volume stagnates, but price increases drive sales

➡️ Strong pricing strategy necessary due to high inflation in countries such as Argentina and Colombia; the company is compensating for this skillfully.

Why Mexico is weakening:

"In Mexico, we are seeing subdued consumer sentiment, partly due to geopolitical tensions."

➡️ Coca-Cola is responding with a campaign to boost confidence ("Hecho en México") and favorable value packs, particularly important in a price-sensitive market.

🌎 North America:

- Sales volume -3 %, mainly affects classic cola & water

- Price/mix +8 %, customers buy smaller, more expensive products or premium variants

- Operating profit +170 % (reported), but only +4 % adjusted

➡️ The big jump comes from the elimination of negative special effects from Q1 2024, e.g. impairments

➡️ Decline in sales is a warning sign, but not (yet) dramatic, offset by pricing strategy

this is what Coca-Cola itself says:

"While we increased sales and profits, we are dissatisfied with the volume trend."

"Hispanic consumers in particular were less willing to buy towards the end of the quarter."

➡️ Coca-Cola is taking the weak sales seriously and, according to the CEO, has already reacted: more focus on faster decisions and targeted investments to boost volumes again.

🌏 Asia-Pacific:

- Volume +6%, strong growth in China, India

- Operating profit -5 % (reported), adjusted +7 %

➡️ Currency impact & higher marketing costs depress earnings, but top in operational terms!

7 Fairlife: A strong brand building block with an expensive finish

Fairlife is Coca-Cola's fast-growing dairy brand (lactose-free milk, protein shakes such as Core Power).

➡️ It was already clear in my last post on Q4: great potential, strong volumes.

➡️ The last purchase price payment of $6.1 bn was made in March 2025.

Effect: Free cash flow fell to -$5.5 bn, without this payment it would have been +558 m.

ConclusionA strong strategic move that hurts in the short term but makes sense in the long term.

CALL:

"fairlife continues to deliver strong performance. We expect a slowdown in growth until additional capacity comes online."

➡️ The high purchase price of $6.1 billion has had a short-term negative impact on cash flow, but Coca-Cola clearly sees the brand as a growth driver.

Despite the write-down in 2024, the momentum remains intact in 2025. You could say a milk brand as an investment case.

8. currency risks and why they are particularly important for Coca-Cola

Coca-Cola generates over 80% of its sales outside the USA.

➡️ When the dollar is strong, foreign revenues are worth less when translated

➡️ Particularly problematic in emerging countries with weak currencies: Turkey, Argentina, parts of Africa

9. outlook 2025: what does Coca-Cola expect?

- Organic sales growth: 5-6%

- Adjusted EPS target: $2.94-$2.97

- Currency impact on EPS: 5-6%

- Free cash flow target (adjusted): $9.5 bn

Further:

Is the currency turnaround in sight? Trump & the dollar in focus

In Q1 2025, a strong US dollar weighed on Coca-Cola's international business, particularly in Latin America, Africa and Asia, where local currencies depreciated massively against the dollar.

But now (end of April 2025) the wind is changing:

- The dollar is losing strength, partly due to political uncertainty surrounding Donald Trump's possible economic policy measures.

- Trump has repeatedly expressed his desire for a "weaker dollar" in order to promote US exports, keyword: Mar-a-Lago Accord 2.0.

What does this mean for Coca-Cola?

➡️ If the dollar trend continues, currency disadvantages could turn into advantages in the second half of the year, which would give an additional boost to reported sales and profits.

Tensions from Trump policy & tariffs, but CFO warns too cautious

"The current global trade dynamics may have an impact on our cost structure and consumer sentiment."

"We are monitoring developments closely, but are relatively flexible thanks to our local business model."

➡️ Coca-Cola is aware of the risks, but believes in its local production structure as a buffer against trade barriers.

10 Conclusion:

Coca-Cola delivers operationally: sales are growing, volumes are rising slightly and brands such as Coke Zero are booming.

- Global strength, especially in Asia & emerging markets

- Strong pricing power, even with stagnating volumes

- Currency risks and one-off special expenses (fairlife) distort the figures

- Demand is falling in North America, something to watch!

My opinion, not investment advice:

Coca-Cola remains solid for dividend investors. Those looking for short-term growth should wait for better entry opportunities. I will hold my position and plan to make further entries next year.

________________

Thanks for reading! 🤝

______________

SOURCES:

[2] Call: https://events.q4inc.com/attendee/694146189

_____________