The tanker market in late March 2025 is firing on multiple fronts. VLCC rates shot up as Middle East cargoes snapped up ships, while Suezmax hit a yearly high in the Mediterranean with Kazakh oil pumping strong. Aframax lags with patchy demand, but clean tankers—LRs, MRs, and Handymax—are riding an Eastern wave of gains. U.S. sanctions are slamming shadow fleets, proposed port fees on Chinese ships spark debate, and Red Sea tensions stretch routes. Venezuela’s export shake-up looms, and Russian oil keeps flowing through sneaky transfers. It’s a high-stakes scene with solid rates and big uncertainties brewing.

This update breaks down VLCC, Suezmax, Aframax, and LR/MR/Handymax trends, plus the forces rocking the boat. From freight spikes to geopolitical jolts, here’s the full picture—laid out clear and simple.

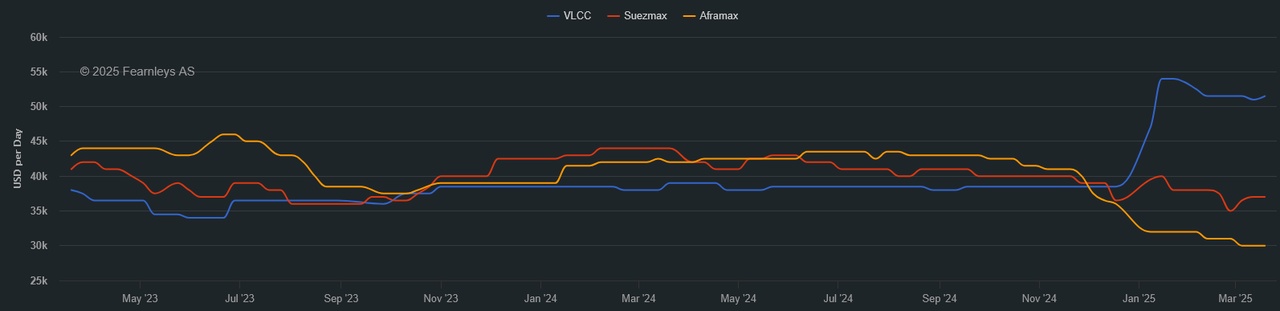

⏬ VLCC Market: Rates Jump, Eyes on April

VLCCs, the giants of crude shipping, saw rates leap to $52,100/day on Middle East-to-Asia runs—a 33% weekly jump—as Saudi April cargoes drained a tight tonnage pool.

A MEG/Korea trip hit WS 67.5 ($51,536/day TCE), nudging toward WS 70, while West Africa to China (TD15) climbed to WS 66.75 ($49,598/day) and U.S. Gulf to China (TD22) rose to $7.797M ($40,321/day).

Atlantic support comes from Brazil and West Africa, but U.S. Gulf stumbles—tariff threats of $1.5M per port call on Chinese-built ships slow exports, though TD22 gained $455,000.

Sanctions nabbed five VLCCs like Kohana (Iran-linked) and tracked Sovcomflot’s STS off Hong Kong—700,000 barrels to Hannah—yet India (1.6M bpd) and China keep Russian oil flowing.

Venezuela’s 790,000 bpd exports face a Chevron $CVX (+0,13 %) exit—Clarksons predicts a 0.5% tonne-mile boost if Middle East crude fills the U.S. gap.

The Daban’s month-long Russian oil trek ended in Qingdao, dodging sanctions via three Sovcomflot Aframaxes—shadow fleets adapt fast.

Fearnley sees yields over 10% for Frontline $FRO (+1,74 %) and DHT $DHT (+0,31 %) —rates could stick above $50,000/day if April stays hot, though futures lag the spot surge.

Activity’s set to hum—Atlantic production rises as peak export season nears, keeping owners hopeful.

⏳ Suezmax Market: Med Peaks, West Wavers

Suezmax in the Mediterranean soared to $63,000/day—a year-high—driven by 38 CPC cargoes from Kazakhstan’s Tengiz field (960,000 bpd via Black Sea).

Globally, rates averaged $52,000/day, up 21%, but Nigeria to UK (TD20) slipped to WS 95.56 ($40,980/day), and CPC/Med (TD6) eased to WS 129.25 ($62,910/day).

West Africa and U.S. Gulf softened—TD20 dropped 7 points, and a Wilhelmshaven relet fell to WS 92.5 after a WS 100 sub—charterers dodged a hike past WS 90.

Germany seized the Eventin (152,000 dwt) with Russian oil in the Baltic—a $30M prize—signaling rare crackdowns on shadow fleets.

Middle East’s TD23 held steady at WS 92.5-93, despite ships shifting west—9M barrels head to Asia in March, 3M more booked for April.

Ukrainian drone hits on CPC pipelines didn’t dent loadings—Kazakh cuts for OPEC+ loom, but no big slowdown shows yet.

Allied notes Western momentum, though Atlantic demand lags—rates might climb further if tonnage stays tight and Asia pulls more.

Owners eye a spillover—West Africa’s steady gains could tighten things up if Med strength holds.

⏱️ Aframax Market: Flat but Flickers

Aframax, the smaller crude runners, stayed muted—North Sea’s TD7 parked at WS 107.5 ($25,500/day), while U.S. Gulf’s TD26 rose to WS 135.83 ($26,577/day).

Mediterranean’s TD19 ticked up to WS 120.61 ($29,000/day), but demand’s weak—March stems are scarce, pushing dates to early April.

U.S. Gulf to UK (TD25) gained to WS 145.56 ($34,697/day), hinting at life as ships ballast out—sanctions hit three Sovcomflot units like Volans.

Russian oil STS off Hong Kong (700,000 barrels) and Nakhodka Bay glitches (e.g., Canis Power) highlight shadow fleet risks—lists still show surplus tonnage.

CPC Aframax loadings fell to 25 in February from 33, with Suezmax taking the load—Kazakh shifts keep things lopsided.

North Sea and CPC lack punch—U.S. firming could lift rates to $30,000/day, but it’s a waiting game for now.

Owners see quiet fixes—consistency’s missing, though Atlantic flickers offer a slim chance of a push.

1 Year T/C - VLCC SUEZMAX AFRAMAX ECO / SCRUBBER - March 19th

⏸️ LR/MR/Handymax Market: Clean Gains East

LR2s in the MEG topped out at WS 166.94 on TC1 (75kt to Japan), now WS 164.17, with TC20 to UK at $4.2M—Med/East (TC15) dipped to $3.04M.

LR1s climbed—TC5 (55kt MEG/Japan) reached WS 180.94, TC8 to UK hit $3.33M—while UK’s TC16 stayed flat at WS 112.5.

MRs roared in the MEG—TC17 to East Africa soared to WS 262.86—UK’s TC2 rose to WS 172.5 ($21,004/day), and U.S. Gulf’s TC14 jumped to WS 121.79.

Handymax rallied—Med’s TC6 hit WS 268.33, UK’s TC23 crossed WS 200 to WS 207.5—naphtha demand from Asia’s petrochemical boom drives it.

Sanctions cut scrubber premiums to $400/day—VLSFO ($497/tonne) edges out HSFO ($439.50)—some owners ditch scrubbers for profit.

U.S. Gulf MRs woke up—TC18 to Brazil hit WS 175.71, TC21 to Caribbean rose 40% to $617,857—Atlantic TCE basket climbed to $27,847.

Eastern rates rule—West gains traction, but Asia’s petrochemical pull keeps clean tankers humming strong.

🌐 What’s Stirring It: Sanctions and Shifts

U.S. sanctions target Iran (Shandong refiner, eight tankers) and Russia (Sovcomflot STS)—India, China, and Venezuela (790,000 bpd) adapt fast.

FMC eyes chokepoints (e.g., Suez) for bans—$1M-$100M fees on Chinese ships could clog U.S. ports, says Bimco—coal and grain face big cost hikes.

Red Sea airstrikes vs. Houthis stretch routes—Clarksons sees container rates up by June—crude pivots to Atlantic as Russia/Iran tighten.

Kazakh CPC oil (960,000 bpd) and Asian demand juice Suezmax and clean tankers—U.S. Gulf lags under tariff clouds.

Venezuela’s Chevron $CVX (+0,13 %) exit could shift long-haul crude—sanctions and fees might reshape flows, not kill them.

It’s a sanctions-loaded, trade-twisting mix—rates ride high now, but disruption’s lurking.

USS Harry S. Truman carrying out strikes against the Houthis

🚨 Outlook: Hot Streaks, Big Risks

VLCCs might hold $50,000+/day if April cargoes pile on—Atlantic could add steam as exports peak.

Suezmax peaks in the Med at $60,000+/day—West needs a demand jolt—sanctions keep tightening the vise.

Aframax waits for traction—$30,000/day’s in reach if U.S. stirs—clean LR/MR/Handymax bank on Asia’s heat.

Port fees and Red Sea chaos could spike costs—volatility’s brewing, but strength’s got legs for now.

💬 What’s Your View?

Riding VLCC highs, or betting on Suezmax’s Med run? Drop your thoughts—let’s dig in! 🚢

*The Worldscale (WS) rate is a system used to calculate tanker freight rates, where WS 100 represents a standard base rate for a specific route. Rates above or below this benchmark indicate how much more or less a charterer will pay relative to the base cost. A higher WS rate means better earnings for shipowners, while a lower WS rate means lower transportation costs for charterers.