🚨 Beware of investing in the next big thing...

Source: CB Insights

$RIVN (+5,16 %)

$ABNB (+3,68 %)

$CPNG (+0,67 %)

$SNOW (+0,59 %)

$COIN (+0,27 %)

$NU (-0,2 %)

$RBLX

$PATH (+3,5 %)

$HOOD (+3,38 %)

$AFRM (+3,63 %)

$PLTR (+6,35 %)

Postes

96🚨 Beware of investing in the next big thing...

Source: CB Insights

$RIVN (+5,16 %)

$ABNB (+3,68 %)

$CPNG (+0,67 %)

$SNOW (+0,59 %)

$COIN (+0,27 %)

$NU (-0,2 %)

$RBLX

$PATH (+3,5 %)

$HOOD (+3,38 %)

$AFRM (+3,63 %)

$PLTR (+6,35 %)

Medium-term objective to buy positions in $MA (-0,34 %) y $V (-0,14 %) when they reach a more appropriate price

These are companies that have performed very well in periods of crisis and maintain stable and growing dividends and constant results.

To equalize the risk a bit, when I have my portfolio at full capacity it will be composed of:

60% Technology with Growth Potential

$GOOGL (+0,94 %)

$NVDA (+2,01 %)

$MSFT (-1,05 %)

$META (-2,23 %)

$AAPL (+1,34 %)

$AMZN (+0,26 %)

$ABNB (+3,68 %)

$NFLX (+0,09 %)

30% Well-performing companies in crisis with stable growth and dividends.

$WMT (-2,1 %)

$MCD (-0,31 %)

$ITX (+1,17 %)

$MA (-0,34 %)

$V (-0,14 %)

10% Companies that can give good results in the long term and are going through temporary difficulties or companies that do not have profits because they reinvest everything in growth (riskier investments but with a higher possible return).

$BFIT (+0,23 %)

$NKE (-6,85 %)

$BMW (+0,87 %)

Any ideas to contribute? 💡

Airbnb share: Chart from 08.11.2024, Price: 140.22 USD - Symbol: ABNB | Source: TWS

We may already be seeing the first signs that the higher marketing expenditure is paying off. At the end of the third quarter, there were already signs of increasing momentum, which continued in Q4 according to preliminary data.

After the number of nights booked in recent quarters consistently increased by a single-digit percentage, double-digit growth is now being recorded again.

This gives reason to hope that the positive trend will continue in the coming year.

As Airbnb fell slightly short of expectations in the third quarter, the share is still trading vorbörslich nevertheless down 4.95 % at USD 140.08.

This gives Airbnb the opportunity to continue buying back its own shares at an attractive price.

In the last 12 months, the number of outstanding shares has been reduced from 681 to 665 million.

Airbnb currently has a P/FCF of 20.1, and while the consensus estimates for the coming year are most likely too low, they suggest that the P/FCF would then fall to 19.

Since Airbnb has been listed, the P/FCF has averaged 29.

In pre-market trading, the share has returned to UnterstützungUSD 140, close to which the upper and upper Aufwärtstrend and the downward trend that has been overcome. Increased buying interest can therefore be expected at this level.

It is therefore quite possible that the spook is already over.

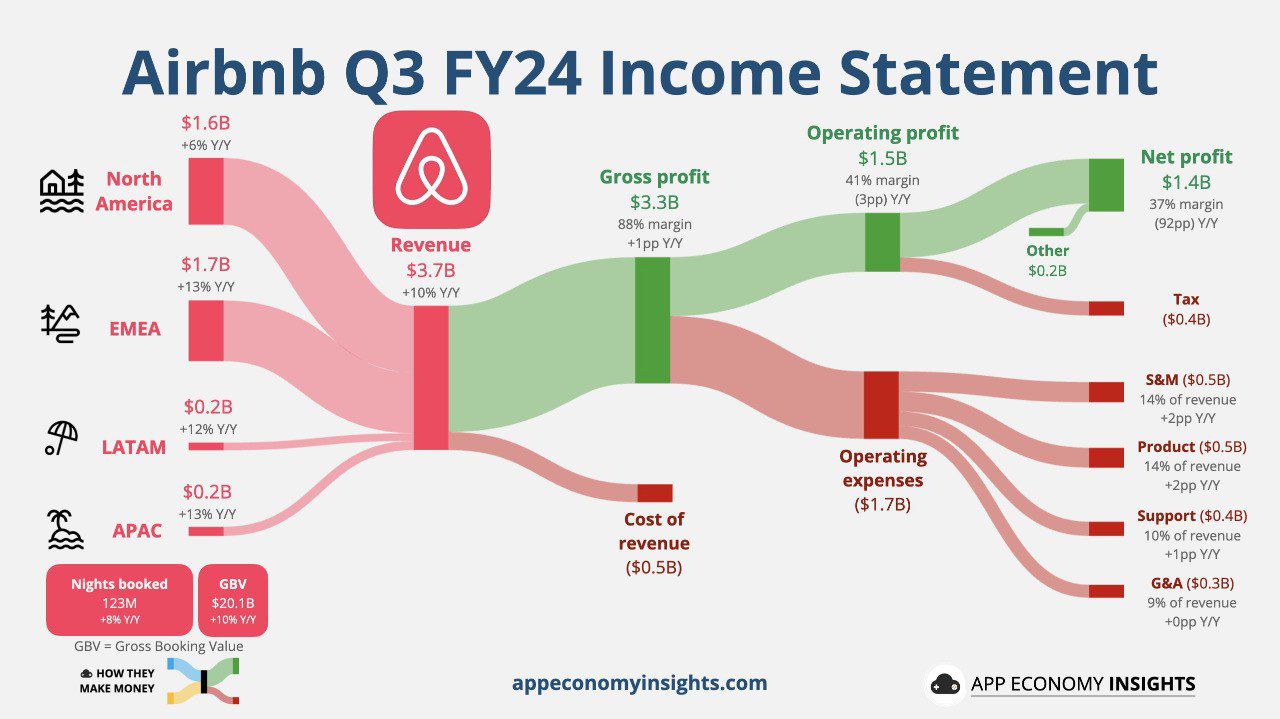

$ABNB (+3,68 %) | Airbnb Q3 Earnings Highlights:

🔹 Revenue: $3.73B (Est. $3.7B) 🟢; UP +10% YoY

🔹 GAAP EPS: $2.13 (Est. $2.14) 🔴

🔹 Adjusted EBITDA: $1.96B; UP +7% YoY

Q4 Outlook :

🔹 Revenue: $2.39B-$2.44B; UP +8-10% YoY

🔹 Expected increase in Nights & Experiences growth vs Q3

🔹 ADR anticipated to increase modestly YoY

🔹 Full-year 2024 Adjusted EBITDA margin ~35.5%

🔹 Full-year Free Cash Flow margin projected to exceed Adjusted EBITDA margin

Business Metrics:

🔹 Gross Booking Value (GBV): $20.1B; UP +10% YoY

🔹 Nights & Experiences Booked: 122.8M; UP +8% YoY

🔹 Active Listings: Over 8M

🔹 Free Cash Flow: $1.1B; 29% margin

Regional Performance:

🔹 North America: Improved growth throughout Q3

🔹 EMEA: Slight acceleration vs Q2, supported by Paris Olympics

🔹 Latin America: Nights booked UP +15% YoY

🔹 Asia Pacific: Nights booked UP +19% YoY

Business Highlights:

🔸 Removed over 300,000 low-quality listings

🔸 Host cancellation rates down nearly 30% YoY

🔸 Launched Co-Host Network in 10 countries

🔸 Cross-border travel to Asia Pacific grew 23% YoY

🔸 Repurchased $1.1B in shares during Q3

Good afternoon everyone,

I am looking forward to the figures from $ABNB (+3,68 %) tonight and how the business has developed.

Will they remain a cash machine?

Is the ban on vacation rentals in some vacation destinations such as major cities in Spain causing them problems?

How is the event industry developing?

...

Let's have a little discussion. I'm looking forward to your opinion 😄

Earnings next week

$$BRK.A (+0,54 %) (Saturday)

Part 1: Embedded Finance

The silent game changer in apps and platforms

Reading time: approx. 4 minutes

Embedded finance - the seamless integration of financial services directly into apps and platforms. But what's really behind it? What technology makes this possible and how does it differ from traditional banking solutions? In this article, I go one step further and shed light on what makes embedded finance so special and how it is already being used by major players and exciting niche companies.

More than just payments

When we think of embedded finance, the first thing that often comes to mind is payment solutions - such as paying with Apple Pay or Google Pay in various apps. But embedded finance goes far beyond that. It also includes loans, insurance, investments and even bank accounts that are directly embedded in non-financial platforms. The trick here is that these services are often presented to the end user as part of the main offering without them realizing that a financial service provider is behind them.

How does embedded finance work technically?

At the heart of embedded finance are APIs (Application Programming Interfaces), which enable third-party providers - i.e. non-banks - to integrate financial services directly into their systems. In the past, companies would have had to enter into separate partnerships with banks or even apply for a banking license themselves in order to be able to offer financial products. Today, API technology allows financial services from specialized providers to be integrated into any platform "in real time".

Simply put, APIs ensure that the complexity behind financial services remains invisible. Instead of having to call a bank or payment provider, everything is handled in the background. This saves time and makes it super convenient to use.

A comparison:

In the traditional model, you used an external payment service provider such as PayPal or a credit card payment for an online purchase, for example. Now the payment runs directly in the background via the platform - often without any additional steps. It works in a similar way for loans or insurance: Instead of applying for a loan via a separate bank, the platform offers you financing options directly, such as Klarna does.

Well-known names that already use Embedded Finance

These examples show that embedded finance is no longer just a nice extra function, but has become essential for the business models of these companies. They enable a consistent user experience and ensure that customer loyalty grows because everything remains in one ecosystem.

Exciting niche examples

In addition to the well-known giants, there are also smaller, specialized providers that use embedded finance in innovative ways.

These niche providers show how versatile embedded finance is and how it also enables smaller players to integrate financial services into their platforms without a great deal of effort.

What distinguishes embedded finance from the traditional model?

In the traditional model, you as a customer often had to actively take an intermediate step in order to use financial services - be it a separate registration with a bank, requesting a loan or buying insurance. The traditional banks act as independent entities that you have to consciously go to.

With embedded finance, this intermediate step disappears almost completely. It is a contextual finance model where financial services are provided exactly where they are needed. Whether it's instant financing for your online purchase or insurance for the goods you've just ordered, it's all embedded in the process, often without you having to think about it.

Another differentiator is the agility. Embedded finance is often used by fintechs or new providers that can react much faster and more flexibly to the market. Traditional banks have major infrastructure and regulatory requirements, which often slows down innovation.

Embedded finance is changing the way financial services are offered and used. With APIs and the ability to seamlessly integrate complex banking and financial products into any platform, companies can offer their customers a whole new level of convenience. Whether you realize it or not, embedded finance has long since arrived in your everyday life - from big names like Uber to specialized fintechs that are making the ecosystem even smarter.

Outlook:

In the next part of the series we take a look at how embedded finance came about and why tech giants are suddenly entering the financial sector. What have banks missed in this development, and how have fintechs and tech companies been able to fill the gap so quickly? We take a look at the historical development and the role of traditional banks compared to new market players.

Stay tuned - it's going to be exciting!

How do you like the start of the series? Let me know and I'll be happy to receive your feedback!

Happy investing! 😊

GG

Still downtrend red zone until this weeks and i think can take more like $ABNB (+3,68 %) , $CTAS (+0,17 %) , $LRCX (+0,38 %) for my list. Good reason if you still use signal indicator but condition market not blind it to hide all. Good day for all 👍💫

Podcast episode 58 "Buy High. Sell Low."

Subscribe to the podcast to see Bitcoin perform in Q4.

00:00:00 Iran & Israel, Buy The Dip

00:16:00 Portfolio performance, September review

00:36:00 Bitcoin, Crypto - ETFs

00:48:00 Hims & Hers

01:06:00 Novo Nordisk, Eli Lilly

01:13:30 Print dies

Spotify

https://open.spotify.com/episode/6qnlfoTcu6MYhqRWq7wJzH?si=5T-g9DHYSt6fFljTK2xjKA

YouTube

Apple Podcast

$LLY (+1,78 %)

$NVO (-18,32 %)

$HIMS (-1,68 %)

$BTC (-2,06 %)

$ETH (-1,28 %)

$SOL (-0,03 %)

$PLTR (+6,35 %)

$SNOW (+0,59 %)

$ABNB (+3,68 %)

#gold

#silber

#palantir

$AMD (-0,35 %)

$NU (-0,2 %)

$P911 (-0,41 %)

$GOOGL (+0,94 %)

Meilleurs créateurs cette semaine