Overview of Semiconductor Manufacturing and Chipmaking Tools Markets

Smartphones, smart cars, LED lighting displays, gaming devices, and countless other Internet of Things (IoT) devices all share a common foundation: semiconductors. These technologies wouldn't exist without semiconductors. The invention of the integrated circuit in 1958 sparked the Third Industrial Revolution, propelling the world into the digital age. Today, everything digital relies on semiconductors, making them the backbone of our increasingly connected world.

Digitalization is pervasive and is expected to continue expanding. As a result, the amount of data that needs to be stored, processed, and transmitted is growing exponentially. The rise of artificial intelligence (AI) and its integration into everyday workflows has further fueled the demand for computing power. To keep pace with this demand, semiconductor production must increase in both volume and capability. Additionally, the significance of the semiconductor equipment market cannot be overstated, as it plays a crucial role in enabling these advancements in semiconductor technology.

Moore’s Law, which predicts that computing efficiency should double every two years, highlights the need for continuous innovation in semiconductor technology to meet the demands of new and emerging technologies. According to Pat Gelsinger, CEO of Intel Corp., semiconductor manufacturing and design will play a role in global geopolitics over the next few decades, akin to the significance of oil production in the last 50 years.

The world faces a significant challenge: ensuring an adequate supply of advanced semiconductors. But who is responsible for this? Who are the key players in the semiconductor market? This article aims to unravel the complexity of semiconductor production and introduce you to the major companies and countries driving this critical industry. While my expertise in engineering is limited, I am confident that by the end of this article, you will understand why companies involved in semiconductor production are so attractive to investors.

—————————————————————————

Market Structure of the Semiconductor Industry

The semiconductor market is highly complex and structured around several key segments that encompass the entire supply chain. The market is structured as follows:

Design and IP (Intellectual Property)

- Fabless Companies: These companies focus on the design and development of semiconductor chips but do not manufacture them. They outsource manufacturing to foundries. Examples include Qualcomm $QCOM (+2,48 %) , Qualcomm $NVDA (+2,01 %) , and Advanced Micro Devices $AMD (-0,35 %).

- IP Providers: These companies develop and license intellectual property (IP) cores that are used in semiconductor designs. ARM Holdings, for example, licenses its processor designs to various chipmakers.

Semiconductor Manufacturing

- Foundries: These companies specialize in manufacturing semiconductor wafers and chips designed by fabless companies. They operate large-scale fabrication plants, often called fabs. Key players include Taiwan Semiconductor Manufacturing Company $TSM (+0,43 %) , GlobalFoundries, and Samsung Foundry.

- Integrated Device Manufacturers (IDMs): These companies handle both design and manufacturing of semiconductors. They own and operate their own fabs. Intel, Samsung Electronics, and Micron Technology are prominent IDMs.

Equipment and Materials Suppliers

- Semiconductor Equipment Manufacturers: These companies supply the machinery and tools required for semiconductor manufacturing, including lithography machines, etching equipment, and testing machines. Key players include $ASML (-1,59 %) ASML, $AMAT (+0,53 %) Applied Materials, and$LRCX (+0,38 %) Lam Research.

- Materials Suppliers: These companies provide the raw materials necessary for semiconductor production, such as silicon wafers, chemicals, and gases. Companies like Shin-Etsu Chemical and SUMCO are major suppliers in this segment.

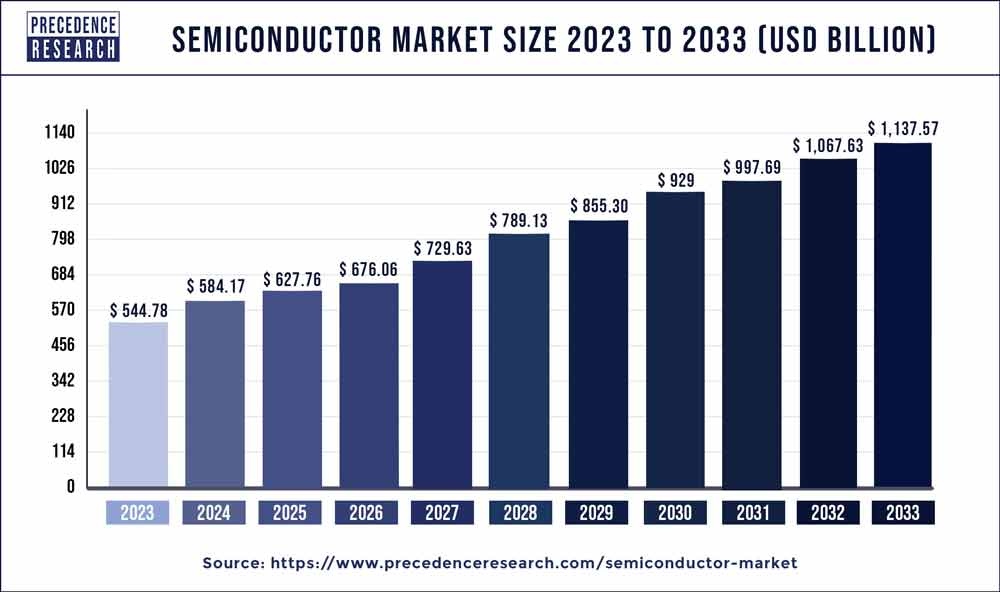

The combined revenues from all segments, along with contributions from smaller beneficiaries, make up the total semiconductor market. In 2023, the market was valued at $544 billion and is projected to grow to approximately $1.14 trillion by 2033, reflecting a compound annual growth rate (CAGR) of 7.64% over the forecast period from 2024 to 2033.

—————————————————————————

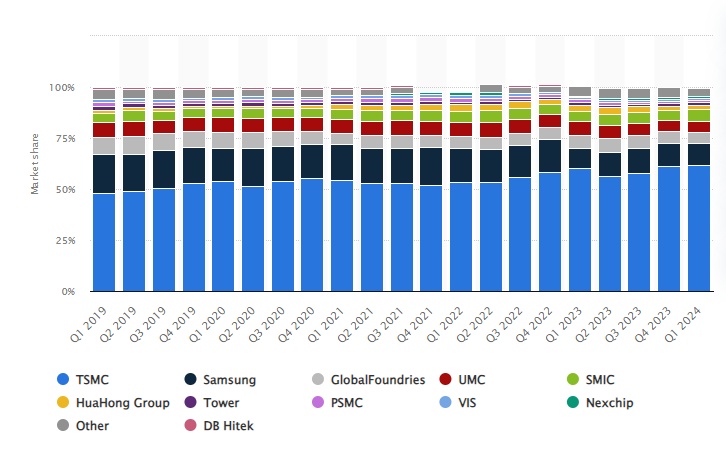

TSMC is the largest semiconductor manufacturer with over 70% of share of the market

In the semiconductor manufacturing market, Taiwan Semiconductor Manufacturing Company (TSMC) holds the largest share, accounting for around 60%. Samsung and GlobalFoundries have market shares of approximately 10% and 5%, respectively. These figures highlight that over 70% of the world's semiconductors are produced in Asia, with 60% coming from Taiwan alone.

In 2020, the COVID-19 pandemic disrupted global supply chains, and with semiconductor production heavily concentrated in Asia, even minor disruptions led to a significant chip shortage. This situation served as a wake-up call, exposing the world's heavy reliance on these critical components and the fragility of the supply chain. Consequently, the semiconductor market is highly sensitive to geopolitical tensions and economic conflicts, such as export/import tariffs and sanctions. These measures can restrict direct sales or limit manufacturers' access to essential raw materials and chipmaking tools, further exacerbating supply chain vulnerabilities.

—————————————————————————

Key Players in Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing Company NASDAQ: $TSM (+0,43 %)

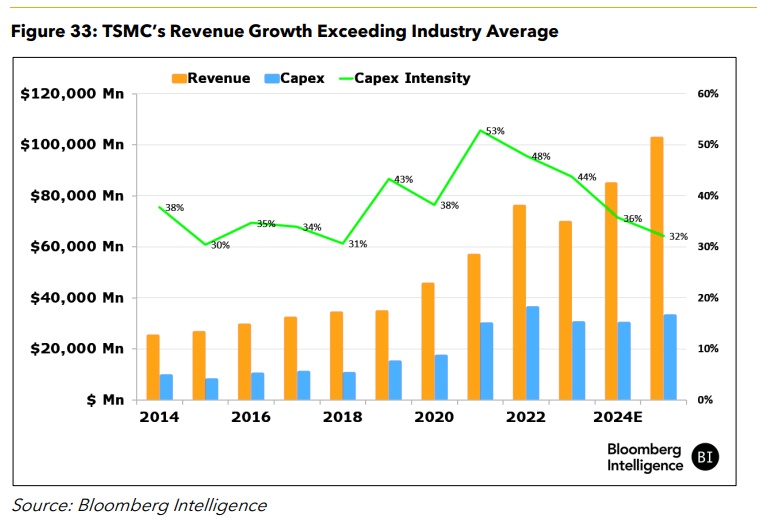

TSMC is poised to cement its leadership of the industry by acquiring more advanced photolithography equipment in the coming decade. Data from SEMI highlights its ambitious trajectory, indicating a potential doubling of its advanced-nodes capacity in the coming eight years, the fastest among the leading trio of firms. TSMC has upgraded its technology node approximately every 24-36 months since 2014. TSMC's capital expenditure (CapEx) intensity is about 35% of its revenue. With an expected revenue growth rate of 8.5% annually over the next decade and maintaining a CapEx intensity of 35%, TSMC could potentially allocate around $400 billion to equipment investments during this period.

TSMC’s comprehensive suite of advanced packaging services, ranging from 2D to 3D solutions, is set to attract strong demand from leading chip designers such as Nvidia, Qualcomm, and Tesla. These services are expected to cater to key sectors including AI, cloud computing, and smartphones.

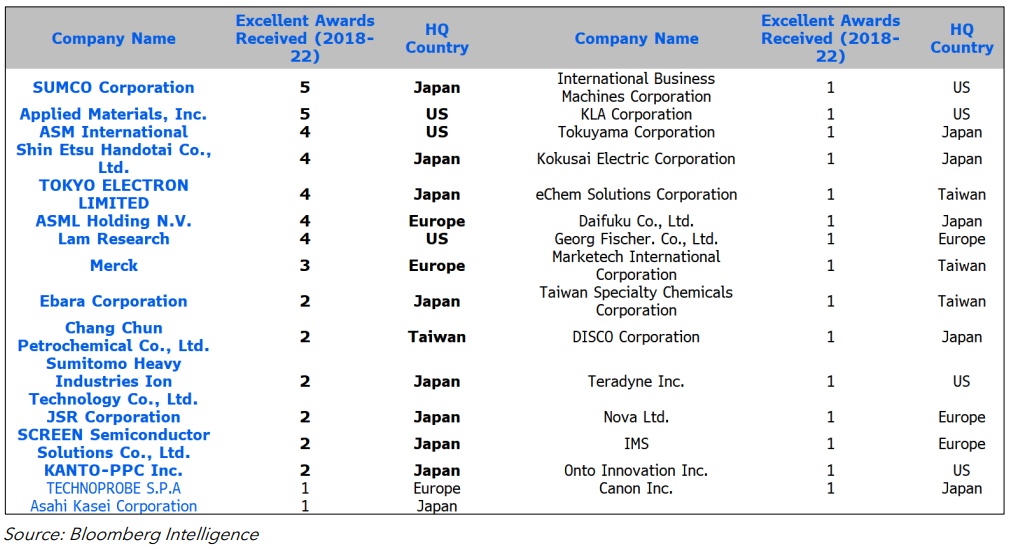

TSMC's sourcing strategy underscores its strong ties to leading global semiconductor suppliers, particularly those from Japan. In 2018-2022, of the 31 suppliers recognized by TSMC's outstanding-performance award, 14 were Japanese, reflecting a clear affinity. The US followed with seven suppliers and Europe with six. Among TSMC's top five suppliers by revenue, ASML, Applied Materials, Tokyo Electron and Lam Research have consistently won the excellence award for the past five years, underscoring their industry-leading positions and commitment to TSMC. As TSMC expands its manufacturing horizon, these key relationships suggest sustained and potentially increased order flows for the top-tier suppliers.

INTEL NASDAQ: $INTC (+1,8 %)

Intel's ambitious foundry plans under its IDM 2.0 strategy, which involves opening its manufacturing capacity to external customers, are expected to drive a significant increase in capital expenditures over the next few years. The company is poised to benefit from US government-led subsidies, particularly through the CHIPS Act, signed into law on August 9, 2022. This legislation provides $52 billion in incentives for semiconductor manufacturing and research in the US, offering crucial support amid escalating trade tensions with China.

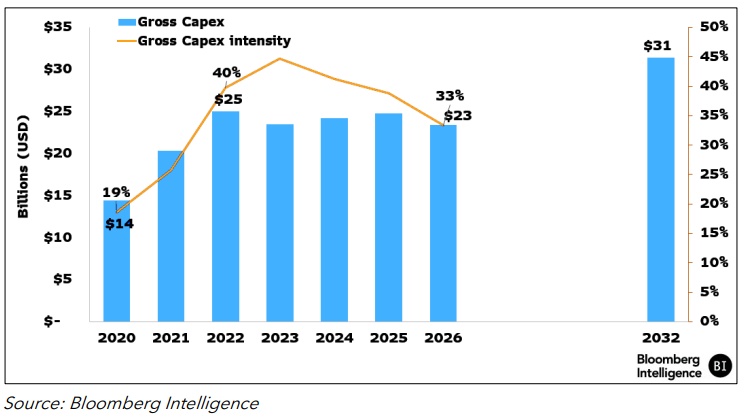

In 2022, Intel’s gross capex was $25 billion, representing about 40% of its revenue. This figure is projected to rise to approximately 45% by 2032. Intel is expected to lead its semiconductor-manufacturing counterparts in gross capital intensity over the next few years, although it will remain behind leading peers in terms of absolute capex dollars spent. This investment is set to introduce a range of new technologies, starting with the integration of EUV tools in Intel 4, followed by advanced Foveros packaging, and ultimately the highly anticipated high-NA EUV technology with Intel 18A—a node designed to secure industry leadership for the company.

Beyond cutting-edge node manufacturing, Intel's expertise in packaging—including chiplets, glass substrates, and Foveros packaging—will be a key differentiator for its customers and a competitive advantage for suppliers. Intel is transitioning from its traditional role as an integrated-device manufacturer to become a leading manufacturing supplier for the fabless chip industry. This shift involves a more collaborative approach, with Intel acting as a customer, supplier, and even competitor to the same companies.

As Intel embarks on its first EUV lithography manufacturing node (Intel 4), suppliers of EUV-associated solutions are expected to become key partners, with ASML, the world’s leading EUV toolmaker, being particularly crucial. Although past contract awards do not guarantee future success, suppliers with a history of consistent and repeated contract wins are likely to continue benefiting from growing business with Intel. To date, Intel’s top suppliers have remained relatively stable, with Applied Materials, Tokyo Electron, Lam Research, and Senju Metal consistently securing major contracts.

Samsung

Samsung Electronics is expected to account for 20% of global chip investment through 2032, focusing on logic, DRAM, and NAND chips. The company aims to produce 1.4-nm chips by 2027 and is advancing with 5-nm, 4-nm, and 3-nm technologies. It leads in DRAM with EUV technology and may adopt high-NA EUV tools for 1-nm chips by 2030.

Samsung plans to expand production in the US with a $17 billion investment in its Taylor, Texas plant, aiming for 40,000 wafers per month by 2024, and potentially adding another facility by 2027. It might add up to nine fabrication facilities over the next 20 years.

Samsung's capital expenditure for chip manufacturing could rise to $50-$55 billion annually by 2032, up from $37 billion in 2022. The breakdown is projected to be 22% for DRAM, 34% for NAND, and 44% for foundry/IDM.

—————————————————————————

How Much Do Manufacturers Invest?

The semiconductor manufacturing business is highly capital-intensive. The growing demand for data collection, computation, and transfer drives the need for more powerful and energy-efficient chips. To meet this demand, manufacturers must continuously innovate their production processes, requiring substantial investments in fabrication facilities (fabs).

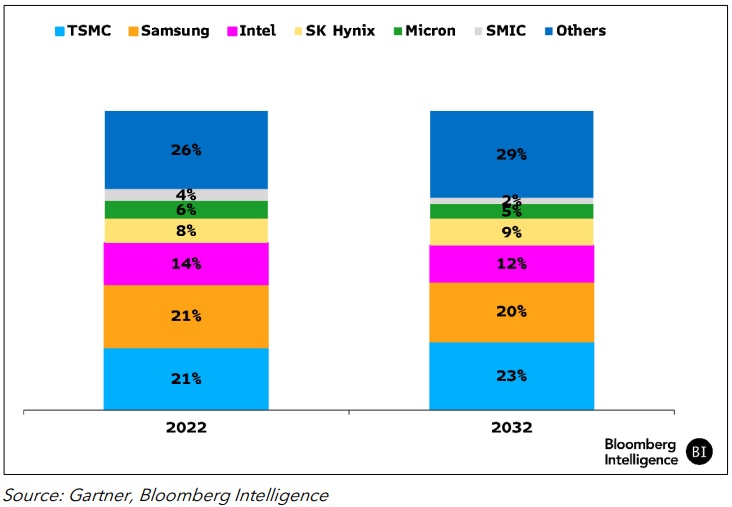

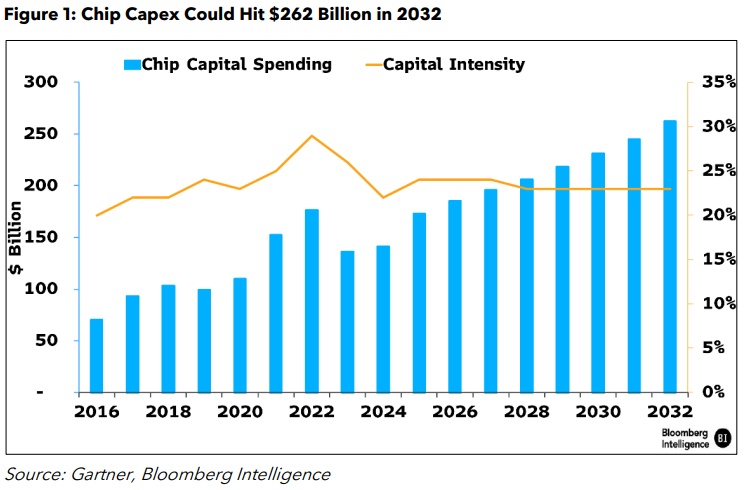

According to Bloomberg Intelligence, semiconductor makers’ capital expenditures could expand from $136 billion to $262 billion in 2032, about 1.9x its level in 2023, mainly because of robust shipments of logic chips. TSMC and Samsung will account for 43% of the industry’s entire capex in 2032.

—————————————————————————

Importance of Miniaturization in Chipmaking

Miniaturization in circuit devices focuses on fitting more transistors onto smaller integrated circuits, which leads to more cost-effective chip production and reduced power consumption. Since semiconductor power consumption is proportional to the square of the drive voltage, lowering the drive voltage results in a substantial decrease in power consumption, achievable through finer wiring patterns.

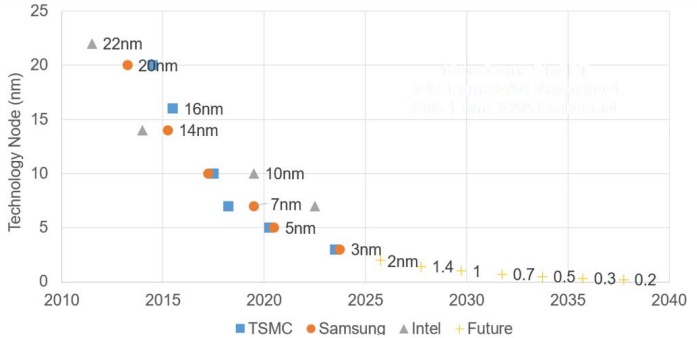

If transistors were 20 nm in size in 2014, they have already shrunk to 3 nm by 2024. The reduction in transistor size highlights the rapid pace of advancement in semiconductor technology.

Although the benefits of further miniaturization may diminish in terms of performance gains and cost efficiency, its impact on energy efficiency remains significant. Miniaturization will continue to be a crucial focus for semiconductor technology over the next 10-15 years, driving improvements in performance, cost, and energy efficiency.

Moore's Law, which predicts that the number of transistors on a chip will double approximately every two years, underscores the importance of miniaturization in meeting the increasing demand for computational power. This trend not only facilitates enhanced performance but also boosts power efficiency, making miniaturization a fundamental strategy for future advancements.

Additionally, miniaturization spurs innovation in fabrication tools. As transistors shrink, the precision and capabilities of manufacturing equipment must evolve accordingly. This continual upgrade of tools ensures that production processes remain state-of-the-art, supporting ongoing progress and innovation in the semiconductor industry. This is why Foundry business is very capital-intensive.

Growing capital expenditure in the absolute form implies the demand for chipmaking tools that manufacturers buy to maintain and renovate their fabs. So, the companies that supply the machinery and tools required for semiconductor manufacturing, including lithography machines, etching equipment, and testing machines will benefit from it. In order to understand the importance of each tool used in the semiconductors' production process, we need to explore the process of production itself.

—————————————————————————

Due to the constraints on the number of images in this post, I will pause here. However, in the next part of this article, I plan to dive deeper into the critical question: What do the leading semiconductor manufacturers need to meet the growing demand?

The answer lies in one key element—the equipment they must upgrade and innovate. In the upcoming article, I will explore the production process in greater detail, highlighting the advanced tools and machinery required to meet this demand. And trust me, without pictures, it will be hard to speak about.

Additionally, I will examine the key suppliers in this space and identify which companies stand to benefit most from the ongoing semiconductor boom. Stay tuned as we explore the technologies and players shaping the future of this high-growth industry.

Let me know in the comments or through reactions if you're interested in the continuation of this article! Your feedback will guide the next steps, so I’d love to hear your thoughts.

Source:

Bloomberg Intelligence

Precedence research

Statista