The tanker market as of late February 2025 is a study in contrasts. VLCC rates oscillate between tight supply and softening sentiment, driven by geopolitical shifts and a wave of new regulations. Meanwhile, Suezmax and Aframax segments wrestle with oversupply and muted activity, though glimmers of demand—like Sudan’s resumed Dar Blend exports—offer some counterbalance. New U.S. port fees targeting Chinese tonnage, sanctions on Iran and Russia, and Trump’s Venezuela policy shift are reshaping the landscape. Oil demand wavers, adding another layer of complexity for shipping investors.

This update dives into the latest across VLCC, Suezmax, and Aframax markets, alongside regulatory and oil market trends. For those tracking shipping stocks or oil-related investments, the mix of risks and opportunities here is worth dissecting. Volatility is the name of the game—let’s break it down.

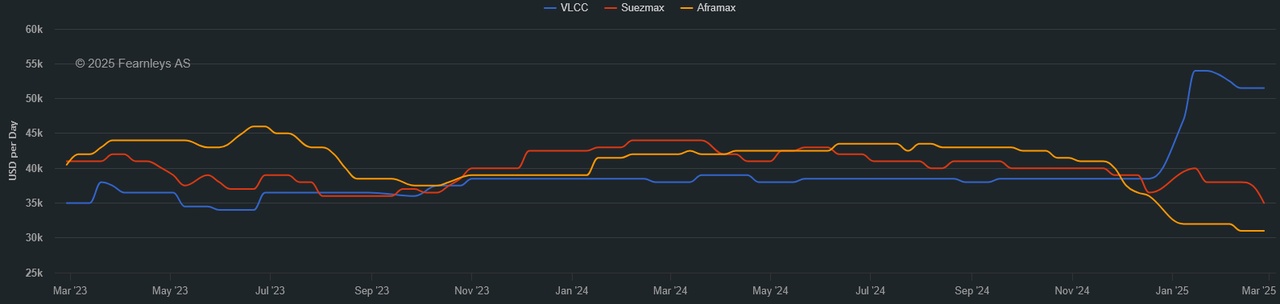

⏬ VLCC Market: Volatility Holds Firm

VLCCs East of Suez show rates in the high WS 50s to China, a level reflecting recent ups and downs. The market’s been quiet this week with IE Week in London slowing activity, but modern tonnage remains scarce, hinting at potential rate gains once schedules clear. In the Atlantic, it’s a different story—tonnage lists are growing, and a lack of U.S. Gulf business has nudged Brazil-Far East rates down to WS 57.25 as the last done deal. Geopolitical ripples add spice: China’s rebounding imports of sanctioned Russian and Iranian crude are fueling demand for older, unsanctioned VLCCs from the shadow fleet. Yet, U.S. sanctions just hit 5 VLCCs (average age ~19 years), part of an 11% capacity squeeze, while the EU and UK blacklist 153 shadow fleet vessels. This tightens supply for non-compliant routes, particularly Middle East to Asia, but softening Western sentiment and expanding tonnage could cap gains. Investors might note the thin balance here—tightness in the East versus oversupply risks in the West.

Rates - Dirty - Spot WS February 26th 2025

⏳ Suezmax Market: Steady but Under Pressure

Suezmax markets are subdued, with little to report East or West of Suez. In West Africa, available tonnage keeps climbing while cargo volumes stay weak, dragging TD20 rates into the mid-80s—a softening trend mirrored in the broader BDTI index. Stateside, activity is picking up in the U.S. Gulf, but Aframaxes are stealing the show, leaving Suezmax supply in charterers’ favor. At least six safe ships are open for mid-first decade March, suggesting rates for USG/TA runs might correct to WS 75 soon. In the East, surface activity is quiet beyond a few Indian quotes, and older tonnage keeps the market balanced, limiting upside. However, 20T crane-fitted vessels are scarcer, which could lift rates if Basrah barrels surge. A rare bright spot: Sudan’s first Dar Blend cargo in a year—1 million barrels on the Suezmax Toska—departed Monday, hinting at Red Sea demand if exports stabilize. For now, it’s a waiting game—steady, but soft.

⏱️ Aframax Market: Cargo Crunch Persists

Aframaxes are feeling the pinch from limited cargo availability. IE Week has kept surface activity low, and natural dates are stretching to the end of March’s first decade. Larger ships are snapping up stems, leaving fewer opportunities for Aframaxes, while ballasting out remains an attractive option for early tonnage. In the Mediterranean, vessels from the North Sea are adding to an already long list, forcing owners to compete harder for employment. U.S. Gulf action might pull some ships stateside, but without a local cargo boost, it’s unlikely to lift rates here. Sanctions complicate things further—3 Aframaxes (~22 years old) were tagged in the latest U.S. Iran crackdown, part of a 16% capacity hit for this class. On the flip side, Dar Blend’s return (historically 61% Aframax-lifted) could tighten tonnage if Sudan’s exports hold. Investors might weigh this oversupply against niche demand pockets—recovery hinges on volume.

1 Year T/C - VLCC SUEZMAX AFRAMAX ECO / SCRUBBER

🌐 Regulatory Waves: Rising Costs, Shifting Flows

Regulatory changes are shaking the tanker market. The U.S. proposes new port fees—up to $1M-$1.5M per call for Chinese-built or owned ships (21-22% of U.S. trade tonnage), adding $7.14-$21.43/t to Aframax costs. This could make U.S. crude less competitive in Europe, pushing oil firms to favor non-penalized tonnage. Sanctions pile on: U.S. targets 13 Iran-linked vessels (11% VLCC, 16% Aframax capacity), while EU/UK bans on Russian hubs like Ust-Luga and 40 more tankers disrupt shadow fleets. Trump’s plan to revoke Chevron’s Venezuela license by March 1 threatens 209k b/d of Aframax exports to the U.S., likely rerouting VLCCs to Asia and raising freight costs. Syria’s EU sanction relief and Dar Blend’s restart signal potential Mediterranean demand, but uncertainty reigns. These moves could favor compliant tonnage while squeezing margins elsewhere—a mixed bag for shipping profitability.

📈 Oil Market Backdrop: Demand Clouds Form

Oil prices are testing the low end of their range, driven by demand worries. China’s shift to alternative energy weighs on growth forecasts, and OPEC+ may boost output, risking oversupply. Geopolitical tensions haven’t jolted prices, with spare capacity cushioning supply fears. Atlantic basin crude growth supports tanker demand short-term, but gas product gains outpace liquids, tempering upside for crude carriers. Low inventories offer some stability, yet without clearer demand signals, absorbing extra supply remains a question mark. Investors might see this as a neutral-to-bearish signal for tanker reliance—watch China closely.

🚨 Outlook: A Delicate Balance

The tanker market sits on a knife-edge. VLCCs could see rate support from tight modern tonnage and shadow fleet demand, but Atlantic oversupply looms as a counterweight. Suezmax and Aframax segments need cargo volume to halt softening trends—Dar Blend’s return offers hope, though it’s tentative. Regulatory costs and sanctions may bolster compliant tonnage rates while pressuring U.S. export economics. Venezuela’s potential output drop and Russia’s restricted flows add downside risks, offset by Syria’s sanction easing and Atlantic basin growth. For shipping investors, it’s a wait-and-see moment—volatility isn’t going anywhere soon.

💬 What’s Your View?

How do you read the tanker market’s next move? Are VLCCs a buy on tightness, or is oversupply the bigger story? Drop your thoughts—let’s unpack this together!