The figures speak for themselves

Over the past ten years, S&P Global has more than doubled its turnover from USD 5.31 billion to USD 14.21 billion.

At the same time, profitability has improved somewhat, with a recent operating margin of around 39%.

During this period, earnings more than tripled from USD 4.54 to USD 15.70 per share.

In addition, the company is constantly buying back its own Aktien shares. Dilution only took place in the course of the takeover of IHS Market. However, this appears to be paying off, as profits have risen rapidly since the acquisition in 2022

Expectations exceeded, forecast raised

Furthermore, S&P Quartalsergebnissepresented. At USD 4.43 per share, Q2 earnings were well above expectations of USD 4.25. With sales of USD 3.76 billion, analysts' estimates of USD 3.68 billion were also exceeded.

For the year as a whole, this corresponds to a 6% increase in sales and a 10% jump in profits.

All divisions contributed to this growth, although the rating business was by far the weakest performer with a sales increase of just 1%. This indicates subdued economic activity.

The index business recorded the strongest growth with an increase of 15%.

In addition, the forecast for sales growth was raised from 4 - 6 % to 5 - 7 % and the profit expectations from USD 16.75 - 17.25 to USD 17.00 - 17.25 per share

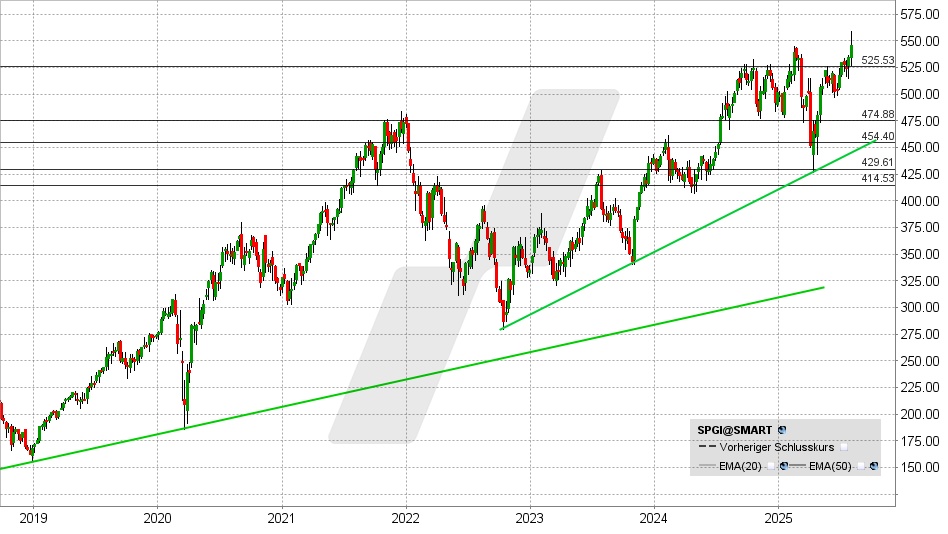

S&P Global share: Chart from 04.08.2025, price: USD 545.66 - symbol: SPGI | Source: TWS

S&P therefore arrives at a forward P/E of 31.7. Over the long term, the P/E has hovered around 27.2. From this perspective, the share would therefore be slightly überbewertet. However, larger setbacks should prove to be an opportunity, as earnings growth of 10 - 12 % p.a. is expected in both the current and the coming financial years.

Source