The dry bulk market in early April 2025 is a tale of cautious stability and looming disruption, shaped by seasonal swings and global policy shifts. Capesize sees a Pacific rebound fade as Atlantic demand wanes, while Panamax rides a soybean wave but faces tariff uncertainty. Supramax and Ultramax stay subdued amid slow activity, and Handysize remains flat with little spark. Trump’s new U.S. tariffs—34% on Chinese imports—and sanctions on Russian grain movers are rattling trade flows, while fees on Chinese-built ships loom large. Coal cuts in Colombia and holiday lulls in Asia add to the mix. It’s a market balancing resilience with risk, with headlines driving the narrative as of April 4, 2025.

This update digs into Capesize, Panamax, Supramax/Ultramax, and Handysize, spotlighting the events shaping them. From trade wars to tonnage trends, here’s a clear, engaging breakdown—easy to read, packed with insight.

⏬ Capesize Market: Pacific Flicker, Atlantic Fade

Market Activity and Rates

Capesize bulkers, the giants of dry cargo, kicked off the week slowly with holidays in Singapore (Hari Raya Puasa), but the Pacific saw a midweek lift—Western Australia-to-China (C5) rates climbed from mid-$8 per tonne to $9.235, with miners fixing in the low $9s. By April 4, though, momentum fizzled—holidays in Hong Kong and China softened activity, pulling C5 back to $8.78. In the Atlantic, Brazil-to-China (C3) held at $21.815 by week’s end, down from $22.45 midweek, while West Africa-to-China edged lower despite steady tonnage. Baltic Exchange spot rates dropped 6% to $20,198/day, with the BCI 5TC at $18,404, signaling a bearish turn.

Demand and Tonnage Trends

West Australia enquiries for mid-April and May dates are healthy, per April 2 reports, with East Australia coal cargoes—like KLC’s $22,750 time-charter—adding support. Pacific spot tonnage tightened midweek as prompt ships cleared out, though ballasting west grew for May. The Atlantic’s North saw transatlantic cargoes fail to soak up ships, tanking the C8 index, while South Brazil and West Africa held steady early on. Allied Shipbroking notes owners banking on fresh May cargoes to revive the market after a sluggish stretch.

Tariffs and Trade Impacts

Trump’s April 2 “Liberation Day” tariffs—34% on Chinese imports—could hit steel and cement, though Greek owner Stamatis Tsantanis sees core Capesize cargoes (iron ore, coal) as less exposed. Glencore’s 5-10M tonne coal cut at Colombia’s Cerrejon mine, slashing 2025 output to 11-16M tonnes, may trim longer-haul trades to Europe and Asia, per MB Shipbrokers. Replacement volumes from Australia or Indonesia—shorter runs—could dent tonne-miles, with Colombian freight to China ($34-$35/tonne) outpacing Newcastle ($13.50/tonne).

⏳ Panamax Market: Soybean Support, Tariff Shadows

Market Performance

Panamax bulkers, the mid-tier haulers, are at a turning point—Baltic spot rates hit $13,489/day by April 1, a 5% weekly rise and 43% monthly jump, surpassing six-month highs. The Atlantic shows a split—North softens with weak mineral demand and rising tonnage, while South America’s soybean exports prop up rates, per April 2 updates. Asia’s Pacific basin faltered—holiday slowdowns and fading NoPac/Australia cargoes met owner resistance, though coal from Indonesia and South American grains lent some lift. By April 4, momentum stalled as U.S. tariff uncertainty widened bid/offer gaps.

Fixtures and Sentiment

Clarksons notes strong Atlantic fronthaul demand—e.g., an 82,000-dwt fixed at $18,750 from North Spain to Singapore-Japan, now closer to $17,000s. In Asia, an 82,000-dwt scored $15,500 for a year-long charter from China. The Baltic reports fixtures like the 87,285-dwt Climate Justice at $18,250 via East Australia to Singapore-Japan, though activity muted post-holidays. Fundamentals seem balanced, but low coal shipments and U.S. grain declines temper optimism beyond the seasonal peak, per April 2 analyses.

Tariff and Macro Pressures

Trump’s 34% tariff on Chinese imports, announced April 2, seeps into sentiment—Braemar Research warns of trade war risks, though Greek owner John Coustas sees long-term shipping gains from rerouted flows. Low coal prices and Glencore’s Colombian cuts could soften demand, while USTR’s $1M-$1.5M fees on Chinese-built ships worry charterers, per April 1 reports. The market holds firm for now—soybeans buoy it—but macro headwinds loom large.

Bulker delivers coal to a terminal in Jiujiang, in China’s Jiangxi province

⏱️ Supramax/Ultramax Market: Quiet Waters, Mixed Signals

Regional Activity

Supramax and Ultramax, the versatile smaller bulkers, stayed subdued—U.S. Gulf wavered with a 61,000-dwt fixed at $16,000 to Japan, while South Atlantic gained traction, like a 64,000-dwt at $14,500 plus $450,000 bonus to SE Asia, per April 4. The Continent-Mediterranean saw slow fixing—e.g., a 58,000-dwt at $14,000 to East Med—while Asia weakened with tonnage oversupply and holiday lulls. Indian Ocean runs, like a 63,000-dwt at $12,000 to Bangladesh, stayed lackluster, though a 61,000-dwt to WC India hit $16,000, per April 2 reports.

Market Sentiment

Global holidays muted activity—sentiment’s mixed, with U.S. Gulf fragile and Asia’s NoPac/backhaul demand poor, per April 2 updates. Slight rate upticks in South Atlantic and Continent-Med offer glimmers, but oversupply in Asia drags overall mood. Trump’s tariffs on steel and cement—key Supramax/Ultramax cargoes—could hit U.S. imports (60M tonnes annually), per AXS data, though trade shifts might offset losses, per Braemar.

Trade and Tariff Impacts

Steel imports, down from 35M tonnes (2017) to 20M (2020) in past trade wars, face new 34% tariffs—cement from Vietnam (3.8M tonnes, 46% tariff) may pivot to Turkey (6.8M tonnes, 10% tariff), per April 3 analyses. USTR’s Chinese ship fees add pressure—Clarksons sees valuation gaps widening, impacting these mid-sized fleets. The sector’s quiet—some positives flicker—but tariffs cloud the horizon.

Self-unloading cement carrier

⏸️ Handysize Market: Flatline Across Basins

Market Stagnation

Handysize bulkers, the smallest dry cargo movers, saw minimal action—Continent-Med stayed flat, with a 35,000-dwt fixed at $7,250 to NC South America, per April 4. South Atlantic and U.S. Gulf held steady—e.g., a 38,000-dwt at $15,250 to Algeria—while Asia’s gradual tonnage rise met modest demand, like a 40,000-dwt at $16,000 to China. Sentiment’s unchanged—long tonnage lists pressure rates across basins, per April 2 reports.

Sanctions and Activity

The U.S. Treasury’s April 2 sanctions hit the Russia-flagged 37,200-dwt Zafar for moving Ukrainian grain to Yemen’s Houthis—linked to Russia’s Salmi Shipmanagement, it’s a rare dry bulk blacklist. Activity stayed low—holidays and weak cargo volumes kept rates stable but uninspired. The market’s in a holding pattern—no big shifts, just quiet consistency.

Tariff Considerations

Trump’s tariffs could ripple to Handysize—steel and cement flows may reroute, though core demand holds, per Greek owner insights. USTR’s Chinese ship fees loom, but impact’s unclear on this smaller tier. For now, it’s steady but subdued—no fireworks here.

" Zafar " (picture above) carried grain from the Crimea to Houthi-controlled Saleef port on at least two occasions last year

🌐 What’s Driving It: Tariffs, Sanctions, and Supply

U.S. Policy Shifts

Trump’s 34% tariffs on Chinese imports (April 2) and sanctions on Russia’s Zafar for Ukrainian grain (April 2) disrupt steel, cement, and coal trades—Braemar sees short-term pain, long-term gains. USTR’s $1M-$1.5M fees on Chinese-built ships widen valuation gaps—Clarksons predicts 7-10% discounts, per April 2. Greek owners like Harry Vafias eye tonne-mile boosts from trade rerouting, per April 3.

Commodity and Tonnage Dynamics

Glencore’s 5-10M tonne coal cut in Colombia shrinks long-haul demand—MB Shipbrokers note shorter Australia/Indonesia runs may follow, per April 1. Holiday lulls and tonnage oversupply in Asia/Pacific weigh on rates, though Pacific Capesize and Atlantic Panamax resist softening, per April 4. Low coal prices and cautious S&P activity—Allied counts 168 dry bulk sales in Q1, down from 237—signal restraint, per April 2.

🌐 Outlook: Cautious Currents

Capesize at $18,000-$20,000/day—Pacific dips, Atlantic weakens—May cargoes key. Panamax near $13,500/day—soybeans prop, tariffs loom—stability tested. Supramax/Ultramax steady—South Atlantic lifts, Asia drags—trade shifts ahead. Handysize flat—rates hold, no spark—quiet persists.

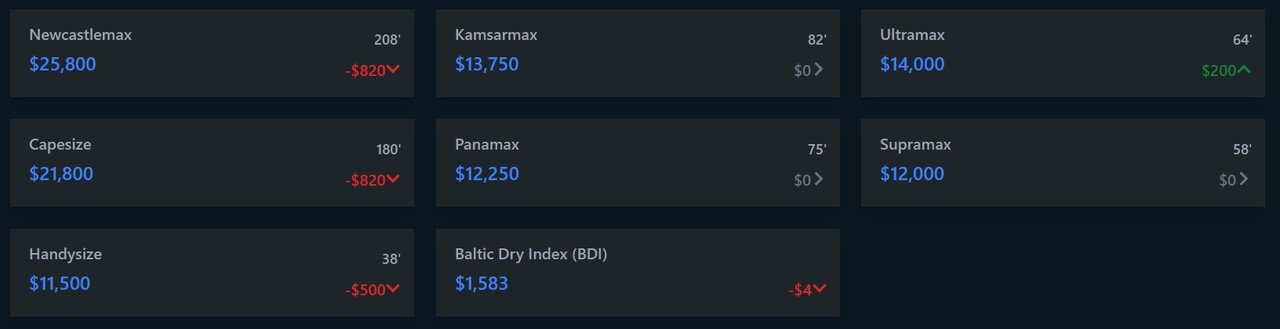

1 Year T/C Dry Bulk - April 2nd

💬 Your Take?

Panamax riding high, or Capesize set to bounce? Drop your thoughts—let’s unpack it! 🚢